%202.svg)

Updated July 2026

Most business credit card spending stays off your personal credit report. But the answer depends on the issuer and on what you mean by "report." Two things get mixed up here: whether you sign a personal guarantee and whether the card's activity shows up on your personal file. They are not the same, and a card can do one without the other.

Here are the key takeaways:

- Most issuers keep routine activity on business bureaus only.

- A personal guarantee creates liability even if reporting stays off your file.

- Corporate cards and options like KleerCard skip both for eligible organizations.

- Nonprofits, churches, and schools face extra risks from leader turnover and recent provider changes.

This page explains how business card reporting works, names the issuers that keep activity off your personal credit and the ones that don't, and covers what that separation means if you run a nonprofit, church, or school.

Do business credit cards report to personal credit?

Most business credit cards report routine activity only to business credit bureaus, not to your personal credit. The common exceptions are Capital One Spark revolving cards and Discover, which report everything, and any issuer reporting a default or serious delinquency.

The card you choose, and how you pay it, decides whether business spending ever reaches your personal file. Pay on time and stick with an issuer that limits reporting to business bureaus, and your personal credit stays clear during normal use. See Capital One's guidance on business card reporting.

Which cards keep business spending off personal credit

Here is how the main options break down. Reporting practices can change, so confirm each issuer's current policy before you apply.

Corporate cards and KleerCard keep routine spending off personal credit entirely. Most bank business cards do the same for day-to-day activity while still requiring a guarantee. Capital One Spark revolving cards and Discover business cards are the clearest exceptions that report full activity to your personal file every cycle.

The two moments a business card can touch your personal credit

A business card can affect your personal credit at two separate points.

The first is the application. Most issuers pull your personal credit as a hard inquiry. That can dip your score by a few points and stays on your report for about two years. Corporate cards underwritten on business financials skip this pull completely.

The second is ongoing use. Whether balances, payments, and utilization reach your personal file depends entirely on the issuer's reporting policy. A card can pull personal credit at application yet never report your day-to-day activity. That is exactly how most bank business cards work.

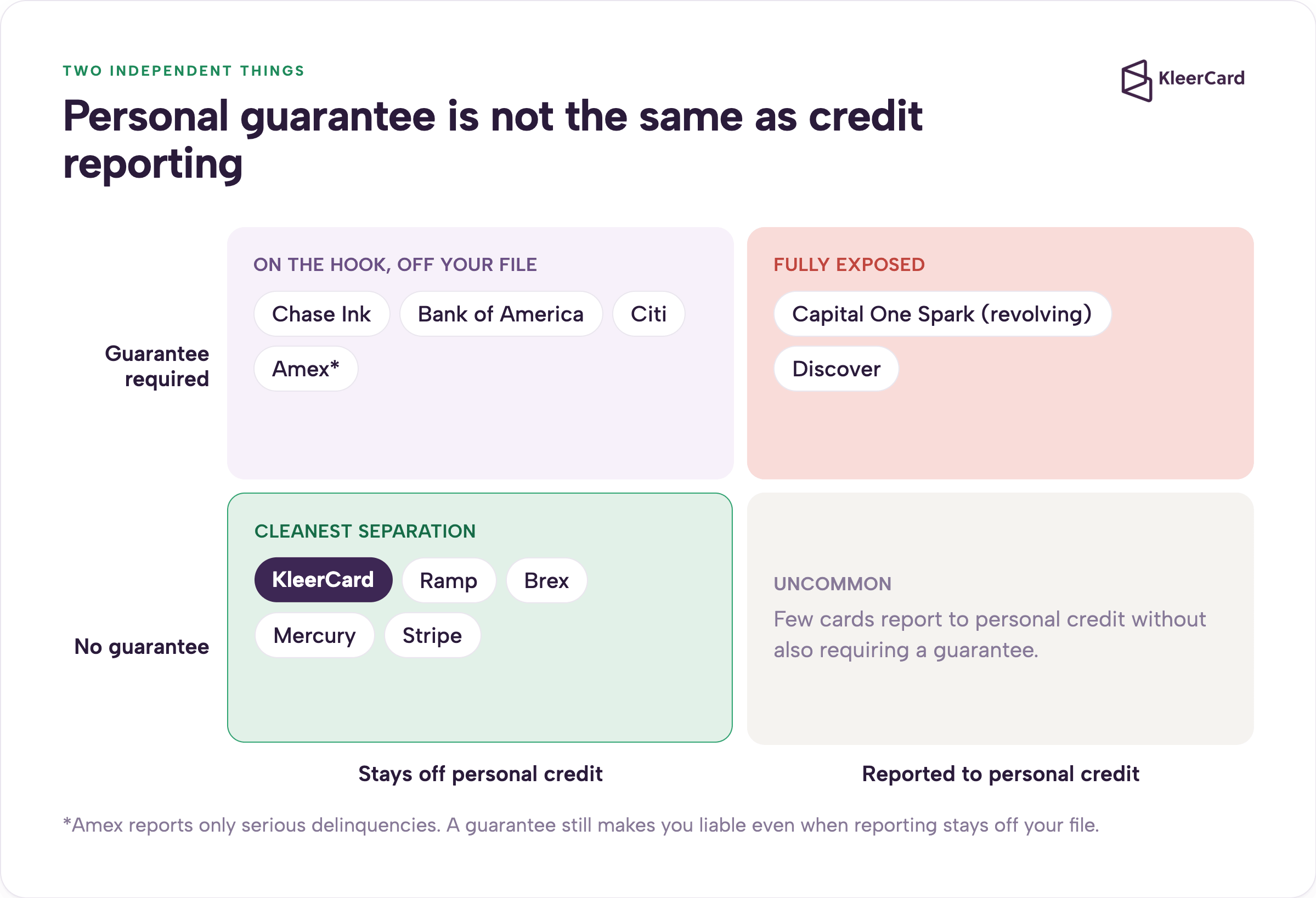

Personal guarantee and credit reporting are two different things

A personal guarantee means you are personally liable if the organization cannot pay. Credit reporting is about what appears on your file. These are different.

Chase Ink cards require a personal guarantee and still keep routine activity off your personal credit. A corporate card from KleerCard, Ramp, or Brex skips both the guarantee and the reporting.

Skipping personal reporting protects your score during normal use. A guarantee still puts you on the hook for the debt, though. A default or collections can reach your personal credit regardless of the issuer's everyday policy.

Which cards report everything to personal credit

Capital One Spark revolving cards report full balances, utilization, and payment history to all three personal bureaus every cycle. Discover business cards do the same. American Express reports negative information when an account becomes seriously delinquent.

A few Capital One products, such as the Spark Cash Plus and Venture X Business charge cards, report only on non-payment. The pattern is clear once you look at the specific product: revolving cards from these issuers are the ones that move routine activity onto your personal file.

Corporate cards skip personal credit entirely

Corporate cards from Ramp, Brex, Mercury, and Stripe approve based on business cash and revenue. They run no personal credit check, require no guarantee, and never report to personal bureaus.

The catch is eligibility. Most accept only registered companies, and some exclude sole proprietors. For a for-profit business chasing rewards or high limits while keeping personal credit completely out of it, one of these is often the right call.

Business cards still build business credit

Most business cards report to Dun & Bradstreet, Experian Business, and Equifax Business. That builds a business credit profile the organization can use later for loans and better terms.

The trade-off is simple. A card kept off your personal file will not help build your personal credit either. That matters for owners with a thin personal history who want every positive payment to count on their own report.

At KleerCard, we only report activity to Dun & Bradstreet. When an organization later needs to apply for a loan (for example, to fund a new building, expand facilities, or cover major equipment) the positive payment history we've helped build strengthens their business credit profile.

Lenders see a track record of responsible spending and on-time payments, which can improve approval odds and terms. We've seen this make a real difference for churches and schools planning growth projects.

Learn the simple steps to start building business credit now.

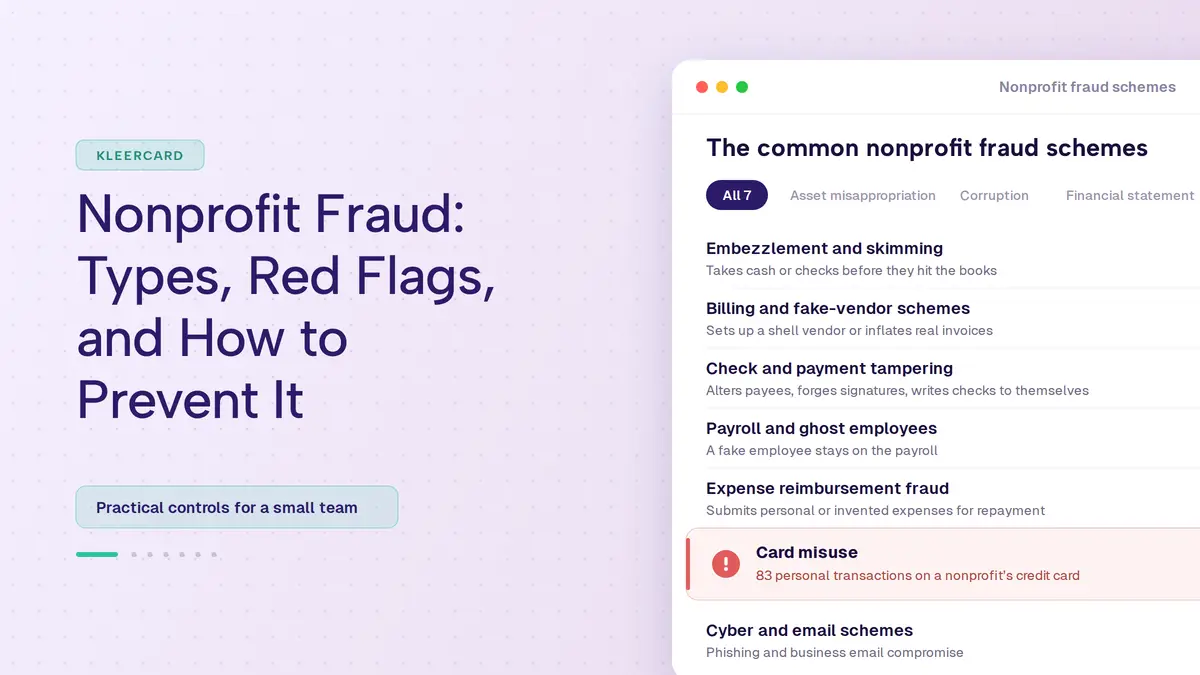

Why this matters more for nonprofits, churches, and schools

When a card sits on a treasurer's or pastor's personal credit, the organization's spending becomes one person's liability. That creates real problems when leaders change roles or a board weighs who signs. Across the organizations we've supported, this is one of the most common pain points we hear.

Turnover is one of the biggest challenges.

When a card is tied to a specific pastor or director, it immediately becomes a liability the moment that person leaves. The former staff member remains personally liable on the account, and if the bank discovers they’re no longer with the organization, it will typically require a new credit check with another staff member as guarantor. Plus the frustrating process of canceling the old cards and issuing entirely new ones.

An organizational card, by contrast, can be seamlessly reassigned to a new staff member without ever touching anyone’s personal credit file.

Recent disruptions made this worse. After one major provider was acquired, many churches and smaller nonprofits under a revenue threshold were suddenly asked for individual personal guarantees. That pushed a lot of them into urgent searches for a card issued to the organization itself. I've spoken with leaders who faced exactly this after their previous program changed terms.

KleerCard handles it differently. We underwrite on the organization's financials and EIN. There is no personal guarantee required, and the account stays off any individual's personal credit record. Leaders can approve growth without putting their own credit on the line.

One school finance team we worked with described going from five shared cards across campus—constant hunting for who had the card—to over sixty individual and loaner cards. They cut lost receipts dramatically and sped up reconciliation, all while keeping spending off personal files. See how expense management works for schools and nonprofits.

Organizations that need to float funds against net-30 or net-60 receivables may be better served by a line of credit or commercial banking. The card model works best when spending stays within budgeted, predictable amounts.

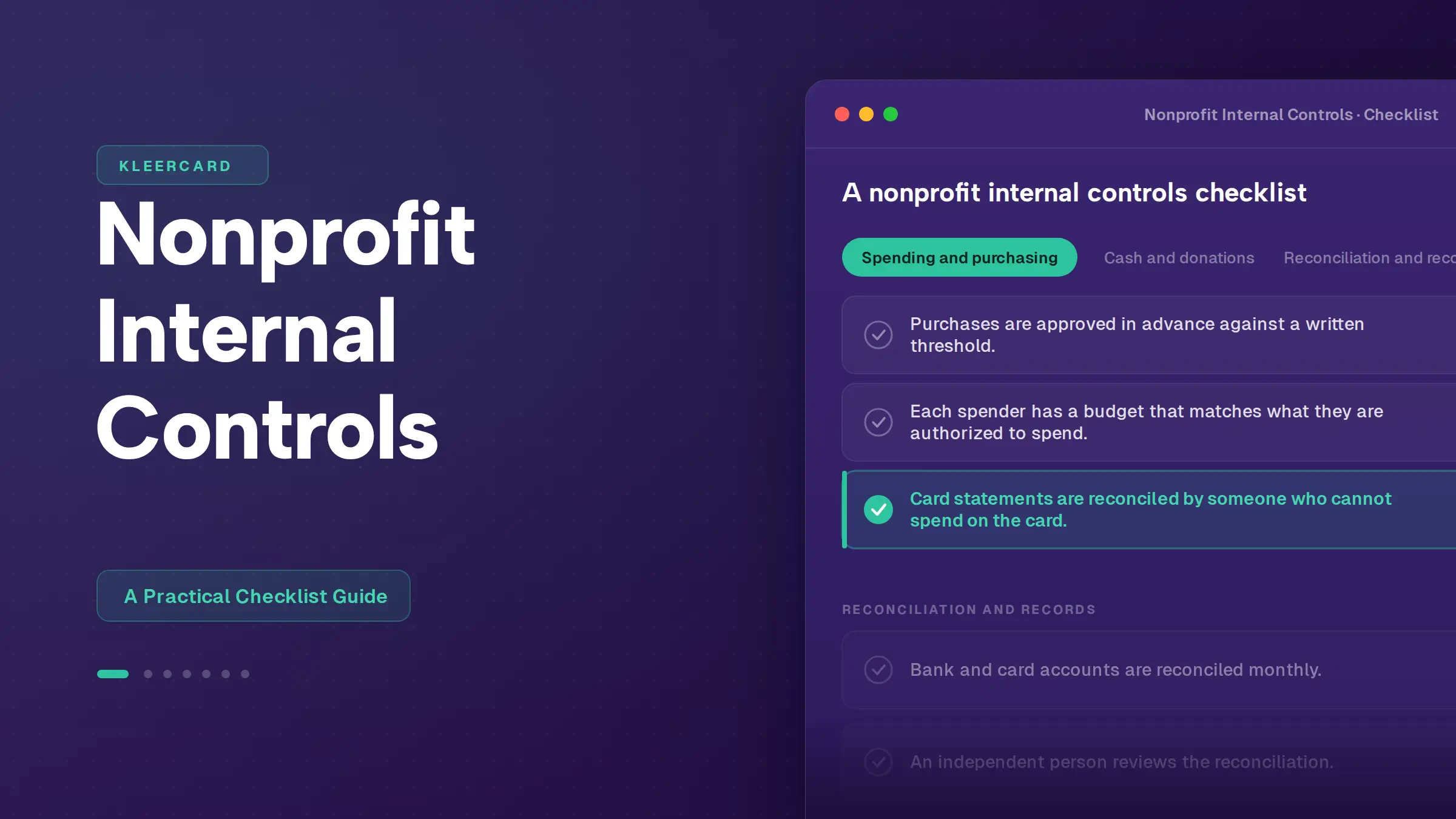

How to keep business and personal credit separate

Open the card under the organization's legal entity and EIN. Choose an issuer that reports only to business bureaus. Pay on time to avoid the default exception that reaches personal credit. Keep organizational and personal spending on separate cards. Review your business credit profile periodically so you know what is building there.

Frequently asked questions

Do business credit cards report to personal credit?

Most report routine activity only to business bureaus. Capital One Spark revolving cards and Discover are the common exceptions that report everything.

Does applying for a business credit card affect your personal credit?

Usually yes, through a hard inquiry at application that can lower your score by a few points. Corporate cards underwritten on business financials skip the personal pull.

Do all business credit cards require a personal guarantee?

No. Corporate cards and cards issued to an organization can skip the guarantee. Most small business cards from major banks still require one.

Does a business credit card build personal credit?

Only if the issuer reports to personal bureaus. A card kept off your personal file will not build personal credit, though it can build business credit.

Which business credit cards report to personal credit?

Capital One Spark revolving cards and Discover business cards report all activity. American Express reports serious delinquencies.

Does KleerCard affect your personal credit?

KleerCard is underwritten on the organization's financials and EIN and asks for no personal guarantee, so the account is not tied to an individual's personal credit record.

Conclusion

For most business cards, routine spending stays off your personal credit. The guarantee, the application pull, and the default exception are the details that decide your exposure.

For a for-profit business, a corporate card from a provider like Ramp or Brex keeps personal credit out of it. For a nonprofit, church, or school, KleerCard issues to the organization with no personal guarantee and pricing built for mission-driven budgets.

See current plans and sign up in minutes.

Explore solutions built for nonprofits and churches.

Pricing details here.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)