%202.svg)

Compare the best credit cards for churches in 2026 on spend controls, virtual cards, fund accounting integrations, rewards, and no personal guarantee options.

Six credit cards still work well for churches in 2026: KleerCard, Devote, AdelFi (formerly Christian Community Credit Union), America's Christian Credit Union, Charity Charge, and AGCU.

The right choice depends on two things. First, whether you need spend controls before the transaction (virtual cards, budget caps, merchant rules) or after (statements and rewards). Second, whether your church runs on a fund accounting platform such as Aplos, Realm, ShelbyNext, ACS, ParishSOFT, Blackbaud, or PowerChurch.

I co-founded KleerCard and serve as treasurer at my church. This guide stays honest about what each option does well and where it falls short.

Two shifts have narrowed the field of church credit cards over the past 18 months.

Amex acquired CenterCard and changed the service terms. Churches under $4M in annual revenue now need individual personal guarantees on cards. The shift forced churches into rushed migrations. A Tennessee church treasurer I spoke with in April had about 60 days from the announcement to find a replacement before service ended.

Ramp also started adding platform fees of $5,000 to $10,000 at customer renewal cycles, beginning in late 2025. In April 2026, I spoke with 13 nonprofits who hit this transition. Ramp has been taking actions that seem to be setting them up for an IPO and the pricing changes line up with that preparation. A surprise five-figure fee at renewal is hard for a church on a fixed budget.

Because of this, neither made it onto our list.

If you used CenterCard and need a replacement, KleerCard and Devote (sections 1 and 2) are the closest fits.

KleerCard is a Visa Commercial card paired with expense management built for churches, schools, and nonprofits. The card belongs to the organization. No personal guarantee is required. Underwriting looks at the church's cash assets and cash flow, not a board member's personal credit.

Churches using Aplos, Realm, ShelbyNext, ACS, ParishSOFT, Blackbaud, or PowerChurch get native exports or direct sync. Most of those platforms lack open APIs, so the integration work happens on the card side. QuickBooks Online and Desktop and NetSuite are also supported.

Unlimited virtual cards can be single-use, recurring, merchant-restricted, or time-restricted. Physical cards ship in 5–8 days. Auto-lock after missing receipts is available on higher plans. Receipt capture happens at the point of purchase through the mobile app or email.

Pricing (current as of mid-2026):

Optional add-ons:

See current KleerCard pricing for full plan details.

My own church has 2.5 paid staff and runs 21 active cards. On a per-seat model that would cost several thousand dollars a year. The Standard or Pro tier covers the same setup for a fraction of that.

An executive pastor reported month-end close dropping from three days to about seven minutes after real-time sync replaced manual entry. An HR and finance director cut receipt collection from roughly 40 hours per month to one hour in the first month.

White-glove setup usually takes two or three 30-minute calls. Application is online and typically returns in 24–48 hours. Virtual cards can be issued the same day approval clears.

Explore KleerCard for churches or sign up to get started.

Devote is a Visa charge card platform with expense management, fund-tied cards, real-time controls, and receipt capture. It requires pre-funding (cash-secured model) rather than traditional credit underwriting. No personal guarantee and no credit check.

Cards can be tied to specific funds or grants. Unlimited virtual and physical cards support per-card limits, merchant categories, and time windows. Auto-lock is available. Devote Points rewards program is included.

Integrations center on QuickBooks Online and other major tools. Fund accounting depth is lighter than KleerCard for platforms such as Shelby, Realm, ACS, or ParishSOFT.

Devote works well for churches that prefer a pre-funded model and do not need the deepest native fund accounting exports. Setup is self-serve with optional support.

See our full Devote card review and alternatives for a deeper comparison. Confirm current details on the official Devote site.

Christian Community Credit Union and AdelFi merged in December 2025. The Ministry Card continues under the combined organization, which is moving to the AdelFi Christian Banking brand through mid-2026.

The card earns 1.5% cash back through CURewards and carries a $300 bonus for $3,000 spend in the first three months. No annual fee. Virtual cards and merchant-level or time-based controls are not available. Limits are set per cardholder through basic tools.

QuickBooks statement download or sync is the primary accounting path. Many churches that already bank with CCCU/AdelFi keep the card for the rewards and the faith-aligned relationship. Underwriting may require a personal guarantee depending on the variant and the church's financial profile.

Confirm current terms and eligibility directly on the AdelFi website after the brand transition.

.avif)

ACCU's Visa Ministry Rewards card earns tiered points: higher rates on travel, hotels, and qualifying charitable donations, with a baseline rate on other spend. No annual fee. The 360Control platform provides limits and reporting but does not support merchant-category or time-window rules at the card level.

Accounting support is CSV export only. No native sync with Aplos, Realm, Shelby, ACS, ParishSOFT, or Blackbaud. Personal guarantee requirements vary by underwriting.

This card fits ministries that travel frequently or make large charitable gifts and already value the ACCU relationship. It is less suited to churches that need virtual cards, auto-lock, or deep fund accounting integrations.

Read the full ACCU Visa Ministry Rewards review. Check current terms on the ACCU site.

Charity Charge offers a Mastercard product built for 501(c)(3) organizations. No personal guarantee on the core Business Card. Real-time controls and employee cards are available. QuickBooks Online integration is supported. No annual fee on the base product.

Virtual cards and merchant/time restrictions are limited compared with KleerCard or Devote. Fund accounting depth outside QuickBooks is thinner. The Corporate Card variant adds rewards.

Mastercard acceptance is the practical limitation for churches that shop at Costco or run international missions. Confirm current revenue thresholds and product differences (Business vs Corporate) on the Charity Charge site before applying.

The Assemblies of God Credit Union ministry card is a no-annual-fee Visa issued through Elan Financial Services. Three variants exist (rewards, low-rate, flexible-rewards). Eligibility is restricted to Assemblies of God churches, AG-affiliated organizations, AG ministers, and their families.

Controls are basic online expense reporting. No programmatic merchant or time rules. Accounting is manual export. Personal guarantee requirements vary.

For AG churches that already bank with AGCU and prefer a simple statement-based workflow, the card remains a reasonable fit. Churches outside the AG fellowship cannot open an account.

See the full AGCU church credit card review. Confirm eligibility on the AGCU website.

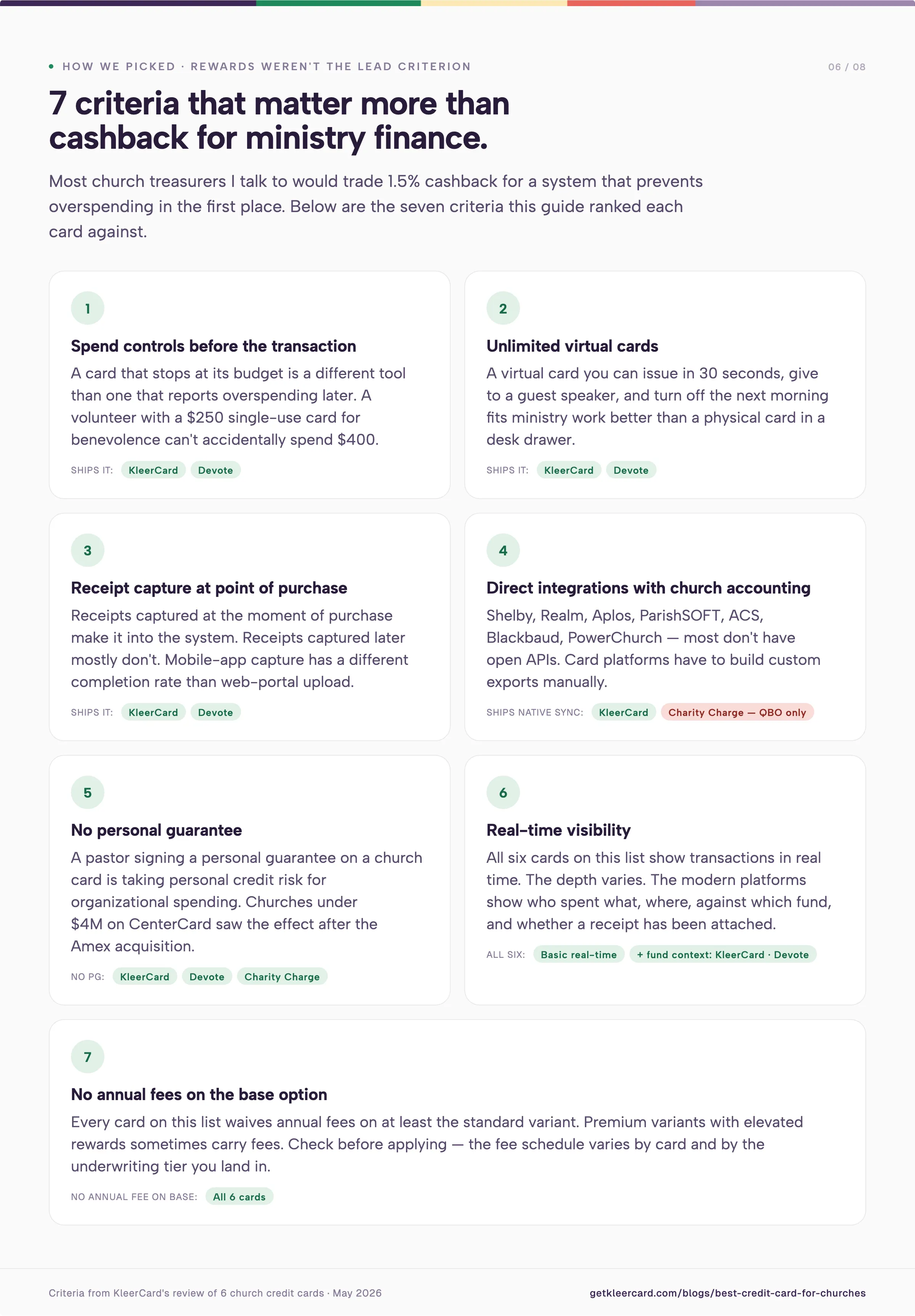

Spend controls before the transaction matter more than rewards for most churches. A card that declines a purchase outside the approved budget or merchant category prevents the problem instead of documenting it after the fact. This is the core of effective expense management for ministry teams.

Unlimited virtual cards let a church issue a single-use number for a one-time vendor or a recurring card for the hospitality team without sharing a high-limit plastic card.

Receipt capture at the point of purchase cuts the monthly chase. Auto-lock for missing receipts enforces the habit.

Direct integrations with the platforms churches actually use (Shelby, Realm, ACS, ParishSOFT, Aplos, Blackbaud, PowerChurch) remove hours of manual coding. QuickBooks-only support is not enough for most fund accounting shops. For a broader view of the tools churches rely on, see our guide to the best accounting software for churches.

No personal guarantee keeps the pastor's or treasurer's personal credit out of the church's liability. For a deeper look at options that never require one, see nonprofit credit cards with no personal guarantee.

Real-time visibility lets finance see every charge as it happens instead of waiting for a monthly statement.

No annual fee on the base option keeps the cost predictable for smaller congregations.

If your church needs complex multi-step approval chains that force a manager to approve before finance can act, KleerCard does not offer that workflow. Many nonprofit finance teams prefer the flexibility to code and close while a camp director is offline for weeks. That design choice is intentional and is not changing.

If you need long-term cash float or interest-bearing revolving credit, look elsewhere. KleerCard is built for controlled spending, not for carrying balances.

If you already bank exclusively with a credit union and value the relationship and cash-back rewards more than virtual cards or fund accounting sync, AdelFi or ACCU may be the simpler path.

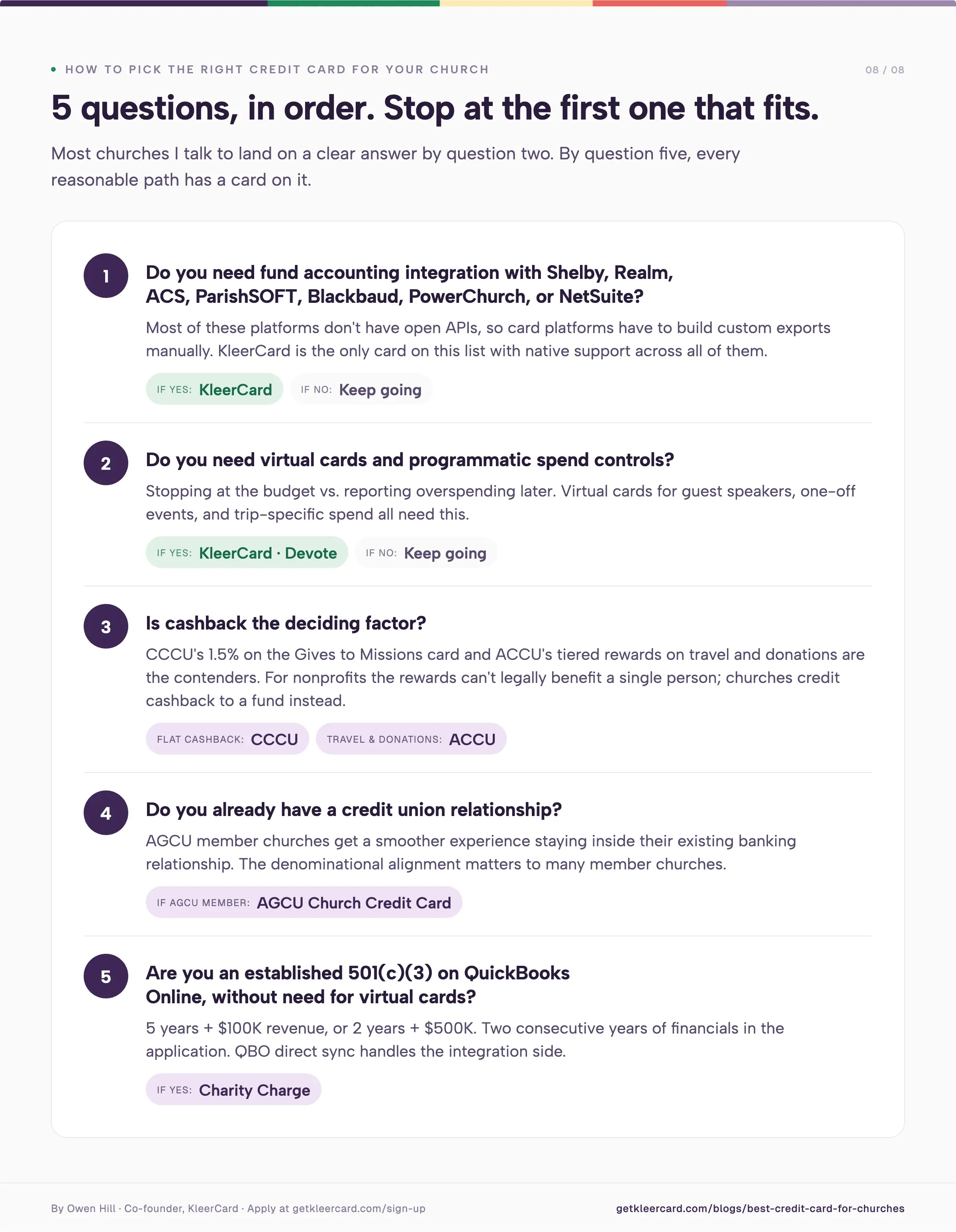

Work through these questions in order:

Once those answers are clear, the shortlist is usually one or two cards.

If you make it through and still aren't sure, the demo form below opens a 30-minute conversation. I'm fine telling you another option fits better, and that conversation happens often.

Most churches still operate with five shared cards or personal reimbursements. The result is lost receipts, delayed month-end, and board members personally exposed. A platform built for fund accounting, virtual cards, and no personal guarantee removes those constraints without adding complexity.

Apply for KleerCard or schedule a short demo. Setup is typically two or three 30-minute calls. Virtual cards can be live the same day approval clears. See current pricing for plan options.

Owen Hill is co-founder of KleerCard. He previously served as Budget Director at Compassion International and founded Switch Consulting, a fractional CFO practice for nonprofits. He volunteers as Treasurer for his local church and has served on the boards of Save the Storks and Life Network.

Yes. Churches organized as 501(c)(3) entities can apply for business and corporate credit cards in the church's name using the organization's EIN. Some cards (KleerCard, Devote, Charity Charge) do not require a personal guarantee from the pastor or treasurer. Others (most traditional bank cards and many credit union business cards) may require one, especially for smaller churches. Confirm with the issuer before applying.

It depends on the card. KleerCard, Devote, and Charity Charge do not require personal guarantees. Bank-issued business cards and many credit union ministry cards may require one, particularly for churches under $4 million in annual revenue. After the CenterCard-to-Amex transition, more church credit card programs moved toward requiring personal guarantees for smaller organizations. See the full list of nonprofit credit cards with no personal guarantee.

For smaller churches (under roughly 200 members or under $500K in annual revenue), starting credit limits typically run from $5,000 to $50,000 depending on the issuer's underwriting model. KleerCard underwrites against organizational cash assets (typically up to 20% of cash assets weekly) without a personal guarantee. Credit unions often base limits on banking history and personal credit.

For churches with 5 to 15 cardholders that use a fund accounting platform (Aplos, Realm, Shelby, ACS, ParishSOFT, PowerChurch, Blackbaud), KleerCard's Standard plan at $29/month fits the typical profile. For churches that prefer cashback and do not need virtual cards or merchant-level controls, the AdelFi (formerly CCCU) Ministry Card is a strong pick.

Yes. 501(c)(3) status does not disqualify an organization. Several issuers (Charity Charge, KleerCard, Devote, AdelFi, ACCU, AGCU) build their nonprofit programs around organizations with 501(c)(3) status. The application uses the organization's EIN, IRS determination letter, and financials.

Some do. AdelFi's Ministry Card earns 1.5% cash back through CURewards. ACCU's Visa Ministry Rewards Credit Card earns tiered points on charitable donations, travel, and hotels.

KleerCard offers cashback to higher-spend customers on custom plans (typical threshold roughly $30,000+/month). Charity Charge has no cashback on the Business Card; the Corporate Card variant does. Rewards earned by a nonprofit cannot legally benefit a single individual. Churches credit them to the general fund, missions, building, or a specific program.

The integrations that matter depend on which platform you use. If you use Aplos, Realm, ShelbyNext Financials, ACS Technologies, ParishSOFT, Blackbaud Financial Edge NXT, or PowerChurch, look for a card platform with native exports or direct sync. Most of these platforms do not have open APIs, so the card platform must build the connection. KleerCard ships those.

If you use QuickBooks Online or NetSuite, more options open up. For a wider look at the software churches actually run, see the best accounting software for churches.

For modern fintech cards (KleerCard, Devote, Charity Charge), the application takes 5 to 10 minutes and approval usually returns in 24 to 48 hours. Virtual cards can be issued immediately on approval; physical cards ship within 5 to 8 days. For credit union cards (AdelFi, ACCU, AGCU), the timeline runs longer, typically 1 to 3 weeks from application to first card in hand, depending on underwriting and existing membership status.

Speak to a member of our team and we can have you up and running in minutes, not weeks.