%202.svg)

By Owen Hill, co-founder of KleerCard. Former Budget Director at Compassion International. Treasurer at his local church.

Last updated May 27, 2026.

The AGCU ministry credit card is a no-annual-fee Visa from the Assemblies of God Credit Union, issued through Elan Financial Services. It offers three variants: rewards, low-rate, and flexible-rewards.

For an Assemblies of God church that already banks with AGCU and reconciles statements by hand, the card fits the current workflow.

Churches that need virtual cards, volunteer access, or direct sync to fund accounting platforms like Shelby, Aplos, or Realm will find the traditional revolving-credit structure leaves manual reconciliation on the table.

This review covers eligibility, published features, the main limitations for church finance teams, and how the card compares to alternatives built for nonprofit workflows.

AGCU Church Credit Card vs. KleerCard: at a glance

Card details verified against AGCU's ministry credit cards page and KleerCard pricing as of May 27, 2026. AGCU does not publish APR ranges, credit limits, or rewards earn rates on the public ministry credit card page. Rates are quoted during the application process.

What is AGCU, and how does its ministry credit card work?

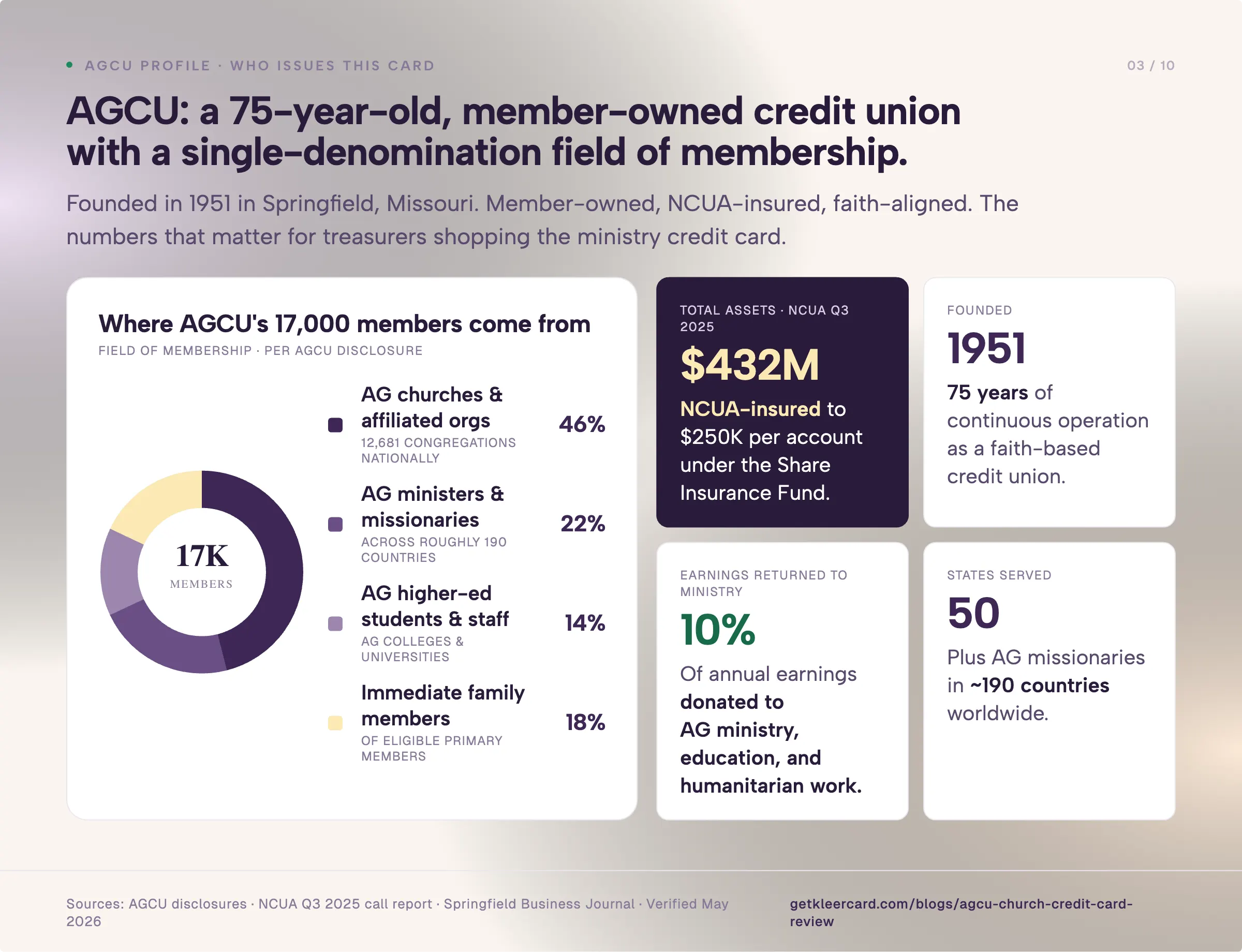

AGCU is a member-owned, faith-based credit union headquartered in Springfield, Missouri. It was founded in 1951 and serves more than 17,000 members across all 50 states plus Assemblies of God missionaries in roughly 190 countries.

AGCU holds approximately $432 million in total assets per the NCUA's Q3 2025 call report data and donates 10% of annual earnings to AG ministry, education, and humanitarian work, according to the Springfield Business Journal.

Membership follows a strict field of membership. Only Assemblies of God churches, AG-affiliated organizations, ordained AG ministers, AG missionaries, AG employees, attendees of AG-affiliated churches, students and employees of AG institutions of higher learning, and their immediate family members qualify. Churches outside the AG fellowship cannot open an account. The Assemblies of God USA reported 12,681 congregations and 1.74 million members in its 2023 census.

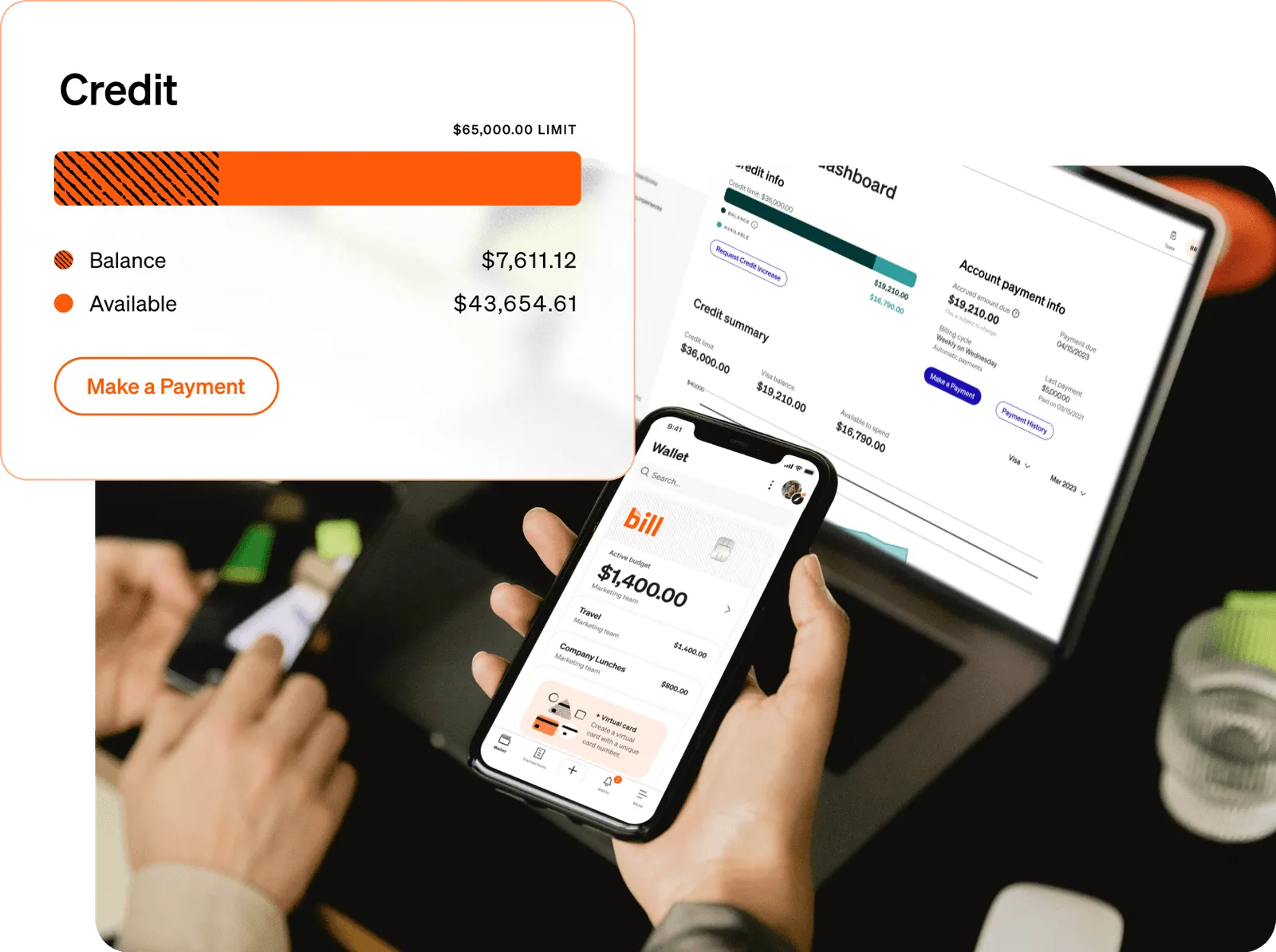

For churches that qualify, AGCU issues ministry credit cards through Elan Financial Services. The product is a traditional revolving-credit business card. Your church applies in the organization's name, AGCU underwrites a credit line, and you pay monthly statements. Balances not paid in full accrue interest at the variable APR set during underwriting.

AGCU offers three variants on its ministry credit cards page: a rewards card that earns points, a low-rate card that prioritizes lower APR over rewards, and a flexible-rewards card that mixes the two. Specific APRs, credit limits, and rewards earn rates are not published publicly and are quoted during the application call.

What the AGCU ministry credit card includes

AGCU publishes these features:

- No annual fee on any variant

- No fee for additional employee cards

- Free online expense reporting tools through the Elan/myaccountaccess.com portal

- Mobile payment capability (Apple Pay, Google Pay)

- Visa Zero Fraud Liability on lost or stolen cards

- 24/7 Cardmember Service, 365 days a year

- Choice of three variants by APR/rewards preference

If your church already banks with AGCU on the checking and savings side, the ministry credit card slots into the same member relationship. You do not onboard a new vendor or learn a new portal.

The rewards math depends on the variant chosen. The Rewards card earns points redeemable for travel, statement credits, or merchandise through the Elan rewards platform. Most Elan-issued credit-union rewards programs deliver around a 1% effective return after redemption. The low-rate card prioritizes APR over rewards and fits churches that occasionally carry a balance month to month.

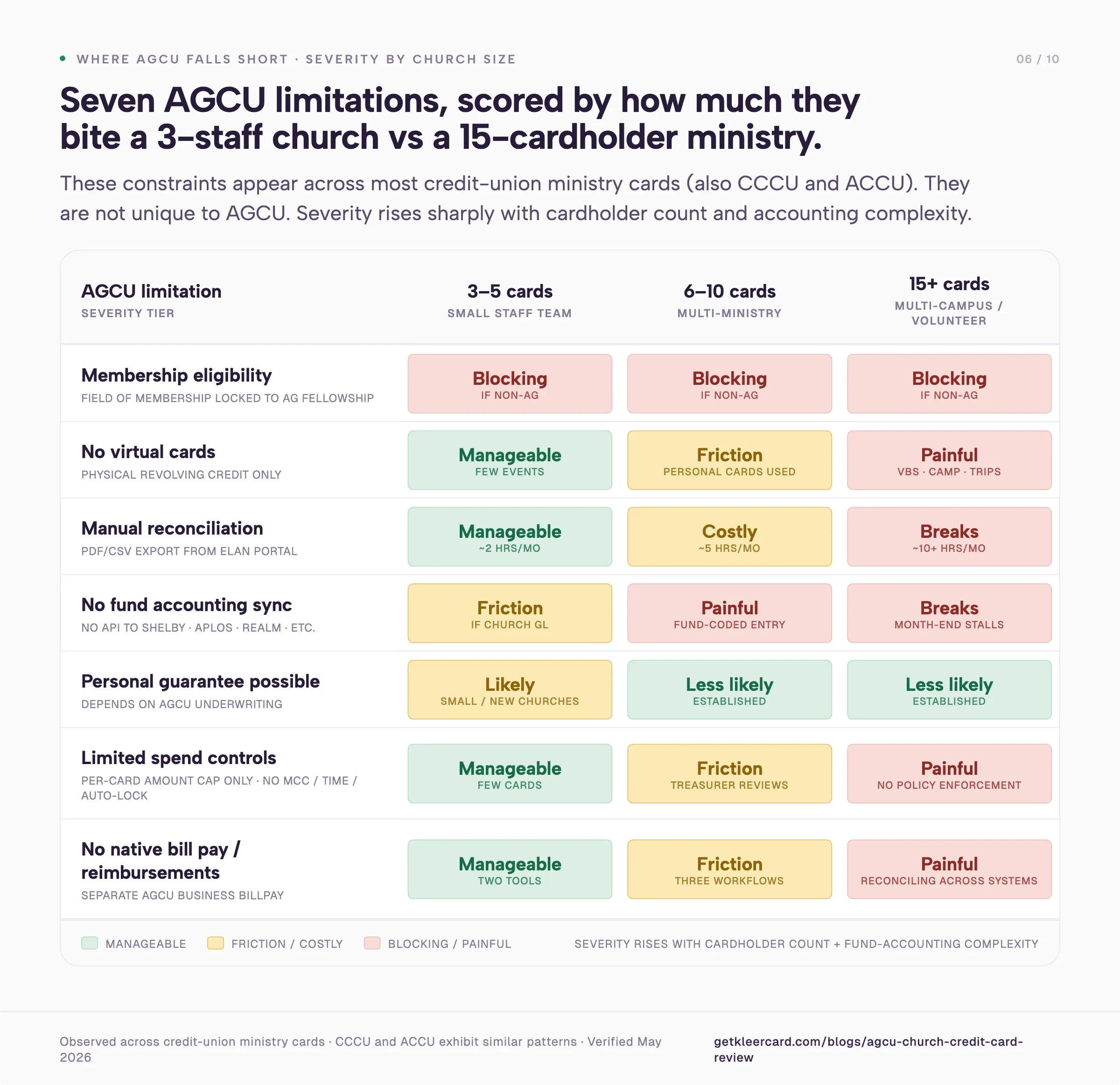

Where the AGCU church credit card falls short

These limitations appear across most credit-union ministry cards, including those from America's Christian Credit Union and Christian Community Credit Union. They are not unique to AGCU. Most treasurers want to walk through the trade-offs before deciding.

Membership eligibility blocks most U.S. churches

If your church is not part of the Assemblies of God fellowship, AGCU is not open to you. Baptist, Methodist, nondenominational, Catholic, Presbyterian, and most other churches must look elsewhere. For an AG church, this section does not apply.

No virtual cards

AGCU's ministry credit cards are physical revolving-credit cards only. You cannot issue a single-use virtual card for a youth pastor's weekend retreat, a missions trip leader buying gas across three states, or a hospitality volunteer running airport pickups.

In my conversations with church finance teams this year, this limitation surfaces more often than any other. A church with three or four cards from a credit union often ends up using staff personal credit cards for short-term events because an organizational card cannot be issued fast enough. Reimbursements then run through accounting after the fact, which creates problems for IRS accountable-plan documentation.

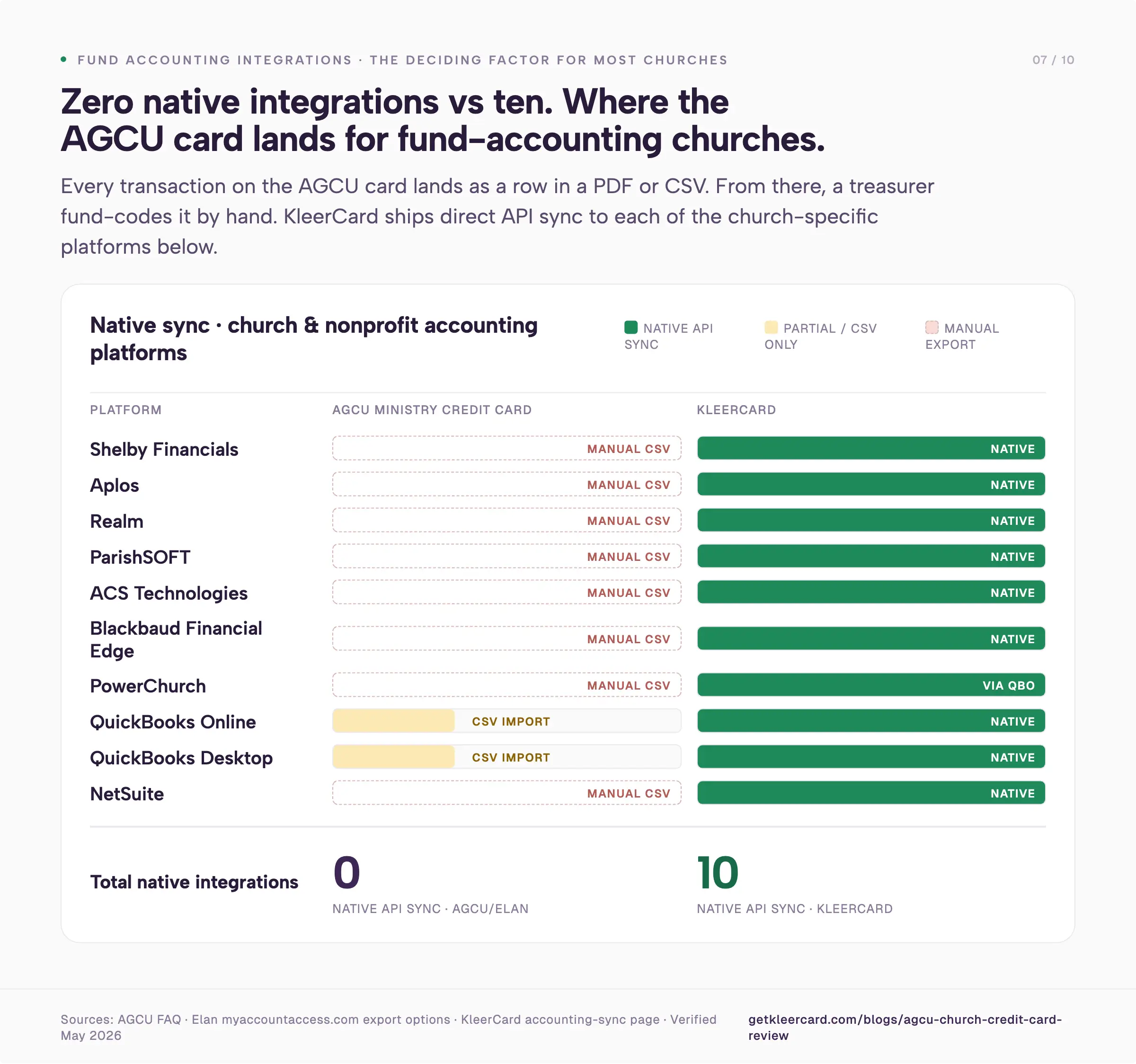

Manual reconciliation and no fund accounting sync

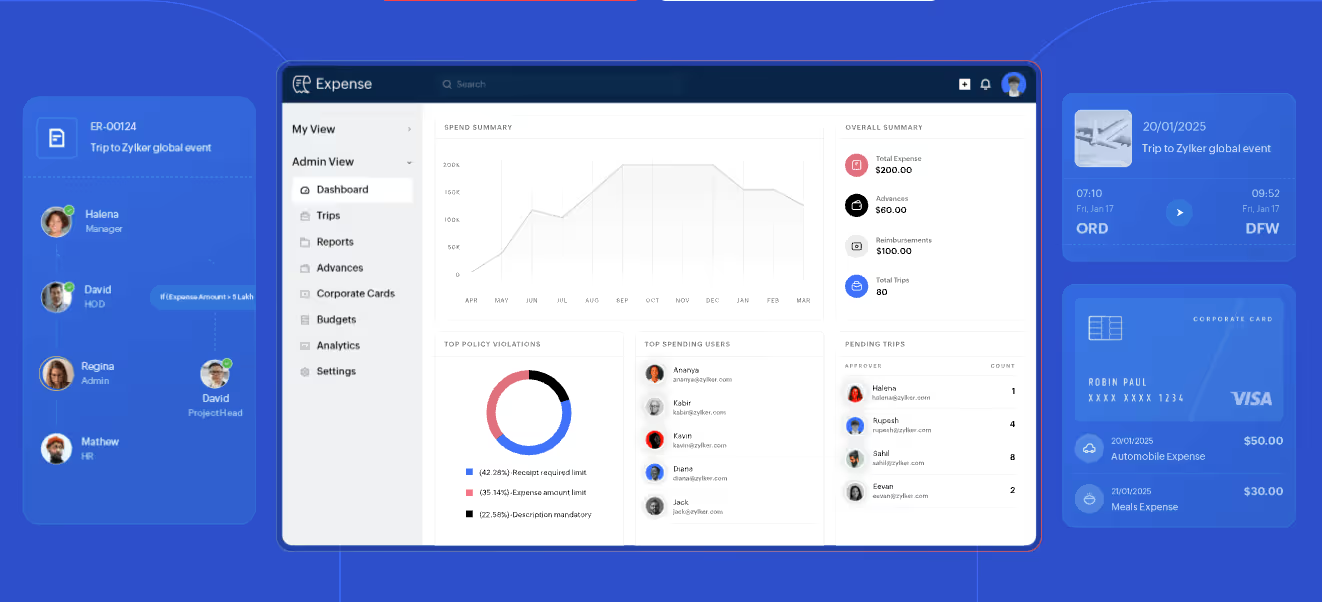

AGCU's online expense reporting tools live inside Elan's cardholder portal. Statements export to PDF or CSV. AGCU does not offer a direct sync with church-specific fund accounting platforms such as Shelby Financials, Aplos, Realm, ParishSOFT, ACS Technologies, Blackbaud Financial Edge, or PowerChurch. Finance teams using those platforms reconcile by hand every month.

Personal guarantee may be required

AGCU's underwriting decides whether a personal guarantee from a pastor or board officer is needed. The answer varies by the church's financial profile, credit history, and the size of the requested credit line. Smaller churches, newer church plants, and ministries with limited organizational credit history are more often asked for one.

This pattern matches most credit-union and bank-issued business cards. If a personal guarantee is a dealbreaker for your church board, ask AGCU about it before you apply rather than after. KleerCard requires no personal guarantee for qualifying nonprofits, churches, or schools.

Spend controls are limited to per-cardholder amount limits

The Elan cardholder portal lets administrators set spending limits per card and view transactions in roughly real time. It does not offer merchant-category restrictions, time-window restrictions, or auto-locking cards when receipts are missing.

For a church with three or four cardholders, the simpler controls are usually enough. For a church with 15 or more cardholders across youth, hospitality, missions, and music ministries, every "did this purchase fit the youth budget?" question turns into a manual review by the treasurer instead of a rule the card enforces on its own.

No native bill pay or reimbursement workflow

The AGCU ministry credit card is a card. Bill pay (ACH or check) and staff reimbursements happen separately, through AGCU Business BillPay or the church's checking account. If you want cards, bill pay, and reimbursements consolidated in a single tool, you manage them across multiple systems.

No church accounting software integrations on the card itself

AGCU card transactions can be exported as CSV or PDF, then imported into your accounting software by hand. There is no API-based, automatic workflow. If your finance team's most time-consuming month-end task is fund-coded data entry, the AGCU card does not reduce it.

Who the AGCU church credit card is right for

The AGCU ministry credit card is a good fit if your church:

- Is part of the Assemblies of God fellowship and qualifies for AGCU membership

- Already banks with AGCU on the checking and savings side

- Has three to five cardholders, all paid staff (no volunteers)

- Uses QuickBooks Online or a comparable mainstream accounting platform

- Does not need virtual cards, merchant-category restrictions, or short-term cards for camps, VBS, or mission trips

- Wants a faith-aligned financial partner whose 10% tithe of earnings funds AG ministry work

You will want to compare alternatives if your church:

- Is not AG-affiliated (any other denomination, nondenominational, or interdenominational)

- Uses Shelby Financials, Aplos, Realm, ParishSOFT, ACS Technologies, Blackbaud, or PowerChurch for fund accounting

- Has 10 or more cardholders, multiple campuses, or seasonal users (camp staff, mission trip leaders, six-week class instructors, summer interns)

- Wants to issue volunteer cards (deacon teams, hospitality, youth ministry parents, missions volunteers)

- Wants merchant-category restrictions, single-use virtual cards, or auto-lock for missing receipts

- Wants cards, bill pay, and reimbursements consolidated in one platform

For churches in the second group, we built KleerCard for the integration depth, the volunteer card workflow, and the seasonal-user math that traditional business credit cards do not cover. See our dedicated solutions page for churches.

For non-AG churches that still want a credit-union relationship, the Christian Community Credit Union Ministry Credit Card review and the America's Christian Credit Union Visa Ministry Rewards review cover the two closest substitutes.

How AGCU compares to KleerCard for fund-accounting churches

The comparison comes down to what your finance team needs the card to do beyond payments. AGCU offers a credit card product built around the Assemblies of God fellowship, member ownership, and a familiar business-card experience. KleerCard is a card-plus-software platform we built around fund accounting, volunteer flexibility, and detailed spend controls.

If you bank with AGCU, qualify for membership, have a few staff cardholders, and reconcile statements by hand anyway, the AGCU card and KleerCard land at roughly the same monthly cost. Your decision becomes a preference call: a faith-aligned credit union with rewards points, or church-specific software with fund-accounting sync, unlimited virtual cards, and consolidated bill pay.

If your finance team runs Shelby Financials, Aplos, Realm, ParishSOFT, ACS Technologies, Blackbaud, or PowerChurch, the comparison shifts. KleerCard's direct integrations remove the manual reconciliation step that the AGCU card does not address. For a church spending five or more hours a month on card-to-fund-accounting data entry (common in the customers I talk to), that time saving usually outweighs the rewards points side of the comparison.

We built KleerCard's direct integrations with each of those fund accounting platforms precisely because asking a volunteer treasurer to enter every transaction by hand at month-end was not workable for our own church. See the full list of integrations on our accounting integrations page.

For most non-AG churches reading this page, AGCU is not an option because of the membership requirement. The relevant comparisons for those readers are KleerCard, CCCU, ACCU, Charity Charge, and the broader list in The Best Credit Cards For Churches in 2026.

A note on cashback. KleerCard's standard plans do not include cashback. Cashback is available on custom pricing for organizations spending roughly $30,000 or more per month on cards. See our full pricing details. AGCU's Rewards card earns points on the Elan platform, redeemable for travel, statement credits, or merchandise. Most credit-union rewards programs land around a 1% effective return after redemption.

For nonprofits, cashback also adds an accounting wrinkle. The rewards cannot legally accrue to one person, and most boards end up directing them to a designated fund (missions, building, general), which adds administrative time at year-end.

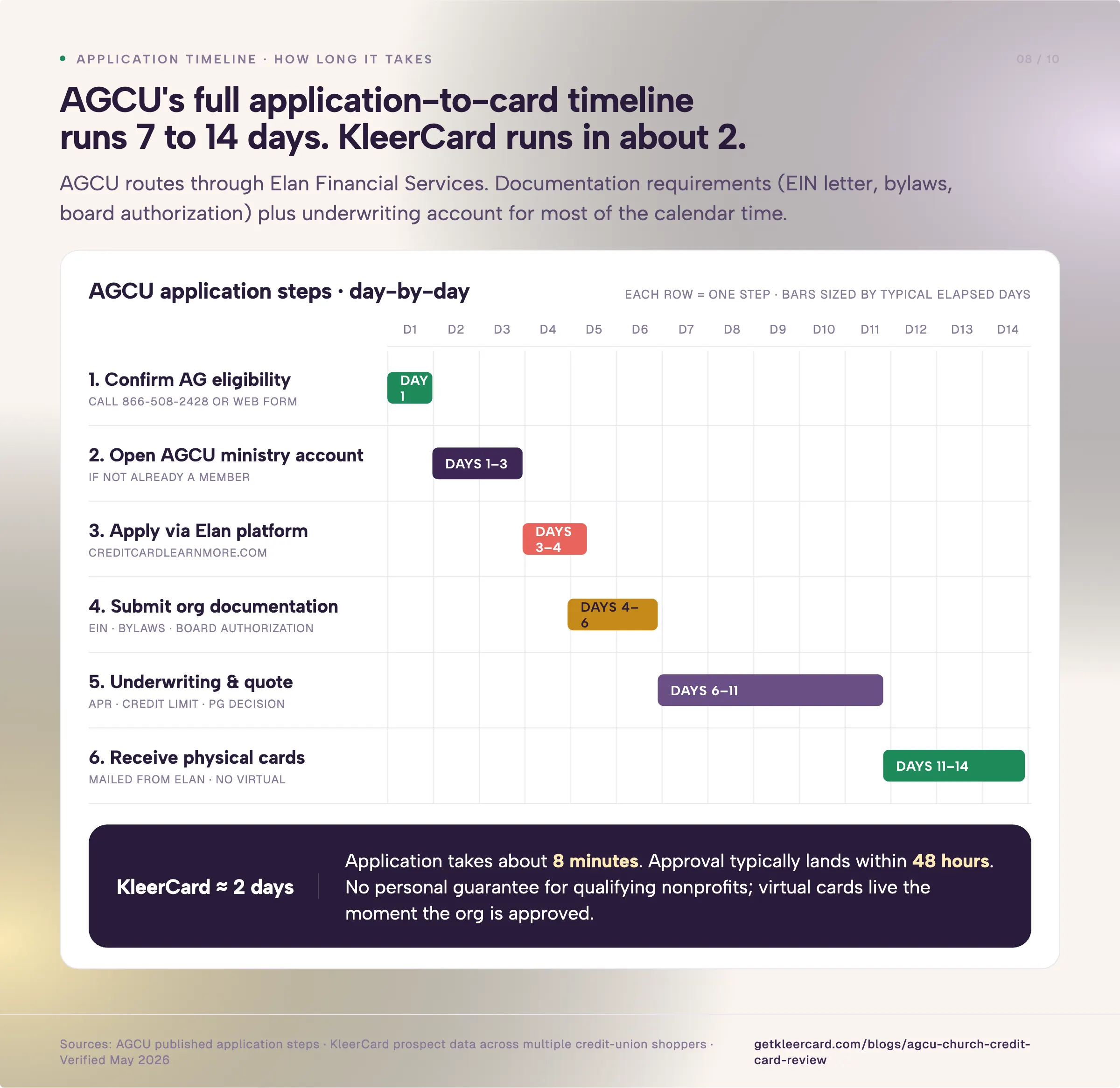

How to apply for an AGCU church credit card

The application process per AGCU's published material:

- Confirm field-of-membership eligibility. Call AGCU at 866-508-2428 or use their online contact form before starting an application.

- Open an AGCU ministry account if you do not already have one. Most ministry credit card applicants are existing AGCU ministry checking customers.

- Apply through AGCU's ministry credit cards page. The link routes to Elan's application platform at creditcardlearnmore.com.

- Submit organizational documentation. AGCU usually asks for the church's EIN letter, governing documents (bylaws or articles of incorporation), and board authorization for the credit card.

- Review the underwriting quote. AGCU will quote your specific APR, credit limit, and (if needed) personal guarantee requirements.

- Receive your cards from Elan. Approved accounts get physical cards by mail. Virtual cards are not offered.

Based on what KleerCard prospects report after shopping multiple credit-union options, the full application-to-card timeline through credit unions on Elan's platform usually runs 7 to 14 days depending on how complete the documentation is.

Frequently asked questions

Who is eligible for an AGCU ministry credit card?

Per AGCU's field of membership, eligibility is limited to Assemblies of God churches, AG-affiliated ministries and institutions, ordained AG ministers, AG missionaries, AG employees, attendees of AG-affiliated churches, students and employees of AG institutions of higher learning, and immediate family members of eligible members. Churches outside the AG fellowship cannot open an AGCU ministry account. Confirm current eligibility directly with AGCU at 866-508-2428 before applying.

Is the AGCU church credit card a good credit card for churches?

For Assemblies of God-affiliated churches that already bank with AGCU and have small finance teams comfortable reconciling card statements by hand, the AGCU card is a reasonable fit. It offers no annual fee, no fee for additional employee cards, Visa Zero Fraud Liability, and 24/7 cardmember service.

For non-AG churches, AGCU is not available because of membership restrictions. For churches that need virtual cards, granular spend controls, or direct integration with church accounting platforms, the decision depends on whether you can absorb the manual reconciliation workload. Compare against KleerCard, ACCU, CCCU, and Charity Charge before deciding.

Does AGCU charge an annual fee on its ministry credit card?

No. AGCU's ministry credit cards have no annual fee, and no fee for additional employee cards. APR ranges, credit limits, balance transfer fees, and cash advance fees are not published on the public ministry credit cards page and are quoted during the application process. Ask about each of these before signing.

Is a personal guarantee required for AGCU's ministry credit card?

It depends on AGCU's underwriting decision for your church. Smaller churches, newer church plants, and ministries with limited organizational credit history are more often asked for a personal guarantee from a pastor or board officer. This pattern matches most credit-union and bank-issued business cards. KleerCard requires no personal guarantee for qualifying nonprofits, churches, or schools.

Does AGCU's ministry credit card integrate with church accounting software?

Not through a direct API integration. AGCU's ministry credit cards run through Elan Financial Services and the myaccountaccess.com portal, which lets administrators export transactions to PDF or CSV for manual import into accounting software. There is no automatic sync with Shelby Financials, Aplos, Realm, ParishSOFT, ACS Technologies, Blackbaud Financial Edge, or PowerChurch. KleerCard ships direct integrations with each of those fund accounting platforms. See the full list on our accounting integrations page.

Can AGCU issue virtual cards for short-term ministry events?

No. AGCU's ministry credit cards are physical revolving-credit cards only. You cannot issue a single-use virtual card for a mission trip leader, a camp staff member, a hospitality volunteer, or a one-day event coordinator. Churches that need virtual cards for short-term events or volunteer roles should compare card platforms built for that workflow, including KleerCard, Ramp, Brex (eligibility permitting), and Charity Charge's newer Nonprofit Corporate Card. Learn more about how virtual cards work in our guide to virtual cards for churches and nonprofits.

What's the difference between AGCU's three ministry credit card variants?

AGCU offers a Rewards card (earns points on purchases through Elan's rewards platform), a low-rate card (lower APR, no rewards), and a flexible-rewards card (a middle option). The specific APRs, rewards earn rates, and credit limits depend on AGCU's underwriting and are not published on the public ministry credit cards page. The Rewards card fits churches that pay the full balance every month and want to redeem points. The low-rate card fits churches that occasionally carry a balance.

How does AGCU compare to other faith-based credit unions for church credit cards?

AGCU serves the Assemblies of God fellowship. America's Christian Credit Union (ACCU) serves a broader Christian audience and offers the Visa Ministry Rewards card with 1.5% cashback. Christian Community Credit Union (CCCU) also serves a broader Christian membership and offers the Ministry Credit Card with 1.5% cash back through CURewards. Each credit union has its own eligibility rules, rewards structure, and APR range. Pick the one your church qualifies for, then compare features against modern card platforms before deciding.

How do I log in to my AGCU credit card account?

AGCU's ministry credit cards are serviced through Elan Financial Services at www.myaccountaccess.com. You log in with the Elan credentials you set up when your card was issued, not with your AGCU online banking credentials. Elan also offers a mobile app (Elan Credit Card) for iOS and Android. AGCU's own online banking at agcu.org is a separate login for checking, savings, and loan accounts.

Is AGCU NCUA-insured?

Yes. AGCU is federally insured by the National Credit Union Administration (NCUA). Member deposits are insured up to $250,000 per account under the NCUA Share Insurance Fund. Per the NCUA's most recent call report data, AGCU holds approximately $432 million in total assets. The credit union has been operating continuously since 1951.

The bottom line for treasurers shopping AGCU

For an Assemblies of God church already inside AGCU's member relationship, the ministry credit card is a reasonable, no-annual-fee option. It fits the way many small AG churches operate: a handful of paid staff cardholders, manual monthly reconciliation, a preference for a faith-aligned financial partner, and a reasonable comfort level with the Elan portal.

If that describes your church, AGCU is worth a look. Confirm the rates and personal guarantee question during the application call. You will know within a couple of weeks whether you have found a good fit.

For everyone else, the comparison usually shifts toward platforms that handle workflows AGCU's traditional card structure does not: volunteer cards, fund accounting sync, granular spend controls, virtual cards for short-term events, and consolidated bill pay.

If those are the items on your shortlist, KleerCard is one option to look at. The application takes about eight minutes, approval usually lands within 48 hours, no personal guarantee is required, and we ship direct integrations with the church accounting software AGCU's card cannot reach. If a different platform on this list fits your church better, I hope this guide helped you figure that out.

Owen Hill is co-founder of KleerCard. He previously served as Budget Director at Compassion International and founded Switch Consulting, a fractional CFO practice for nonprofits. He volunteers as Treasurer for his local church and has served on the boards of Save the Storks and Life Network.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)