%202.svg)

KleerCard competes with Ramp and Brex for nonprofit and church buyers. Full disclosure at the bottom of this article.

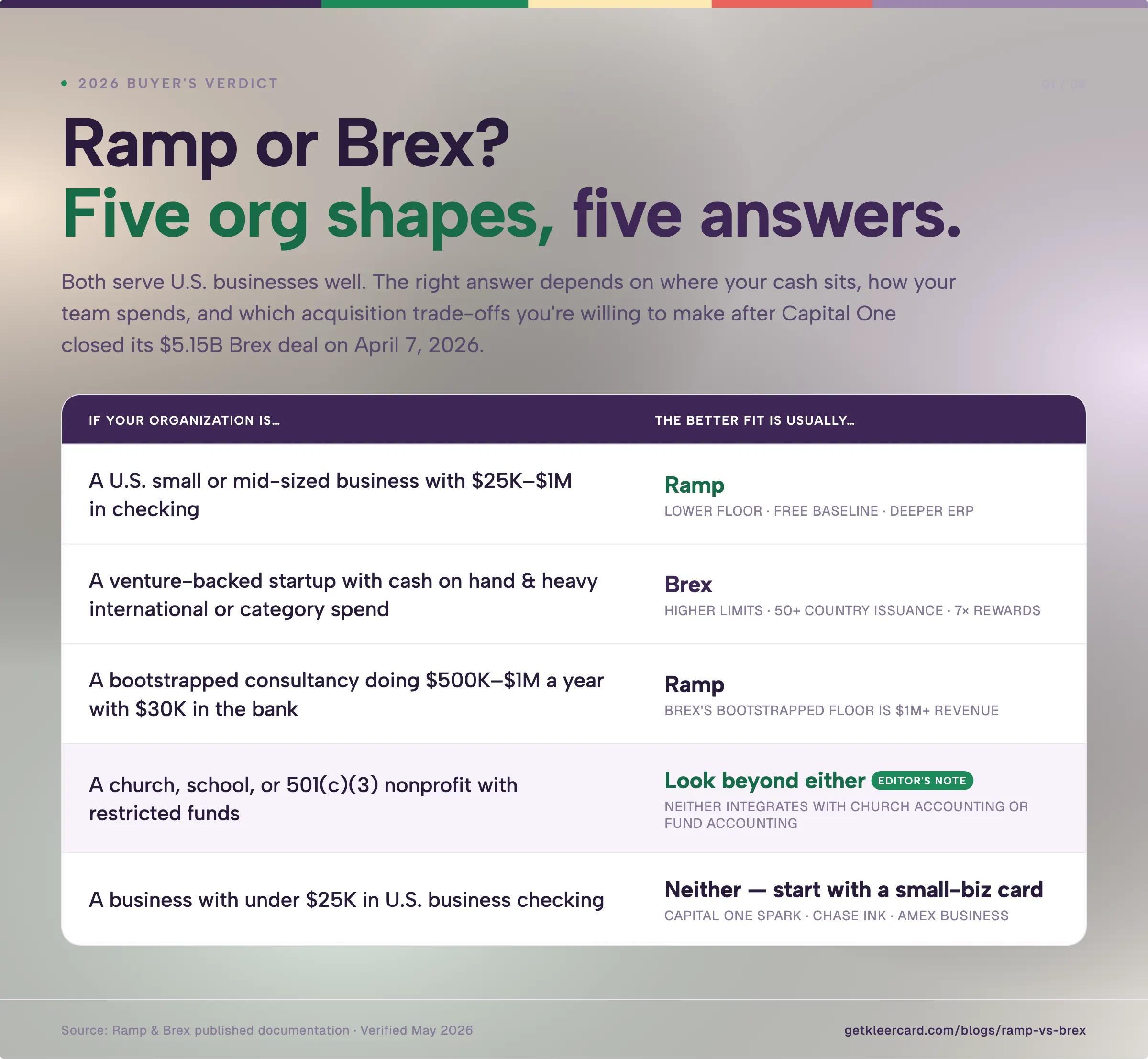

Ramp vs Brex: short answer

For most U.S. small and mid-sized businesses, Ramp is the better fit. It has a lower eligibility floor, a free baseline product, and deeper ERP integrations.

For venture-backed startups with cash on hand and a lot of international or category-heavy spend, Brex still has the edge. Capital One closed its acquisition of Brex on April 7, 2026, which is worth weighing if you're picking Brex right now.

Churches, schools, and 501(c)(3) nonprofits with restricted funds probably want to look beyond either one. Neither integrates with church accounting software or supports fund accounting natively. (See our breakdown for nonprofits here.)

If you have less than $25,000 in your business bank account, neither will approve you on standard terms. A small business card from Capital One Spark, Chase Ink, or Amex is the more realistic path.

The Capital One acquisition: what changed in 2026

Capital One announced its acquisition of Brex on January 22, 2026, in a deal valued at $5.15 billion, 50% cash and 50% stock. The deal closed on April 7, 2026. That price represents a roughly 58% drop from Brex's $12.3 billion peak valuation, per CNBC's coverage.

Pedro Franceschi stays on as Brex CEO. Capital One says pricing, products, and support are unchanged for now, while acknowledging the transition will reshape product direction and policies over time.

A few things are still unanswered for buyers evaluating Brex this year: whether Brex keeps shipping product at the same pace under bank ownership, whether eligibility or pricing tightens as Capital One's risk models layer onto Brex's underwriting, and whether the customer base drifts toward Capital One's traditional commercial banking clients and away from the venture-backed startups Brex grew up serving.

Capital One has only said integration will be gradual. None of those questions have public answers yet.

If you're evaluating Brex right now, the product still works the way it did six months ago. The longer-term direction is the part that's uncertain.

Ramp vs Brex at a glance

Where Brex is the better choice

A few situations where Brex tends to win:

Higher credit limits for cash-heavy startups. Brex underwrites against your cash balance and funding history. A company holding $2-5M can access credit limits 10-20x higher than traditional small business cards offer, per NerdWallet. That kind of headroom is useful for a funded startup with $80,000 in monthly card spend and eighteen months of runway.

Global card issuance. Brex issues local-currency cards in 50+ countries with no FX markup. A startup with engineers in Berlin, contractors in Bogotá, and a sales team in London avoids the layered FX fees a U.S.-issued card produces. Ramp charges a 3% currency conversion fee on foreign-currency purchases, per NerdWallet's Ramp review.

Category-rich rewards for startup spend. Brex pays up to 7x on rideshare, 4x on restaurants and travel booked through Brex Travel, and 2x on software subscriptions. For a team whose spend stack runs Uber, DoorDash, AWS, and conference travel, the points program can outpace Ramp's flat cashback. Points redeem through travel partners, statement credits, and gift cards.

Travel infrastructure. Brex's built-in travel booking earns 4x points and integrates with TravelBank for policy management. For finance teams managing distributed travel across multiple countries, it tends to come up well in side-by-side reviews against Ramp.

Where Ramp is the better choice

A few situations where Ramp tends to win:

Lower eligibility floor. Ramp accepts businesses with $25,000 in connected accounts. Brex's $50,000 funded-startup minimum (or $1M revenue if bootstrapped) excludes a large share of small businesses and most small nonprofits. A bootstrapped consultancy doing $600,000 a year with $35,000 in checking qualifies for Ramp and falls short of Brex.

Free baseline product. Ramp's free tier includes unlimited physical and virtual cards, bill pay, expense management, basic policy controls, and accounting sync. Brex's Essentials tier is also free, but the more useful Premium tier runs $12/user/month last published. For a 10-person company without multi-entity or PO workflow needs, Ramp's free product covers more than most teams use.

Independent roadmap. Ramp stays independent and venture-backed. Brex now sits inside a bank holding company with $475.8 billion in deposits, per Capital One's announcement of the deal. There are trade-offs in both directions. Capital One brings balance sheet scale and underwriting depth. Bank ownership tends to slow feature velocity. For teams that want faster product cycles over the next year or two, Ramp is the safer bet.

ERP depth. Ramp ships bi-directional, real-time sync with QuickBooks Online, NetSuite, Sage Intacct, and Oracle Fusion. Brex's QuickBooks Online integration caps you at one Brex account per QBO account, and edits in QuickBooks don't sync back to Brex, per Relay Financial's comparison. Finance teams running multi-entity setups on QuickBooks tend to feel that ceiling at month-end close.

Spend control granularity. Ramp lets you set merchant-level, category-level, and vendor-level restrictions on individual cards. Brex offers category-level controls. The practical difference: a Ramp card locked to "Office Depot only" works at Office Depot and nowhere else. A Brex card capped to "office supplies" works at Staples, Best Buy's office aisle, Amazon Business, and a long list of other merchants in the same MCC. For finance teams handing cards to non-finance staff, the more granular lockdown helps.

Is this comparison relevant for your organization?

Most people searching "Ramp vs Brex" are running for-profit businesses. Both products serve that audience well, and what's above should be useful.

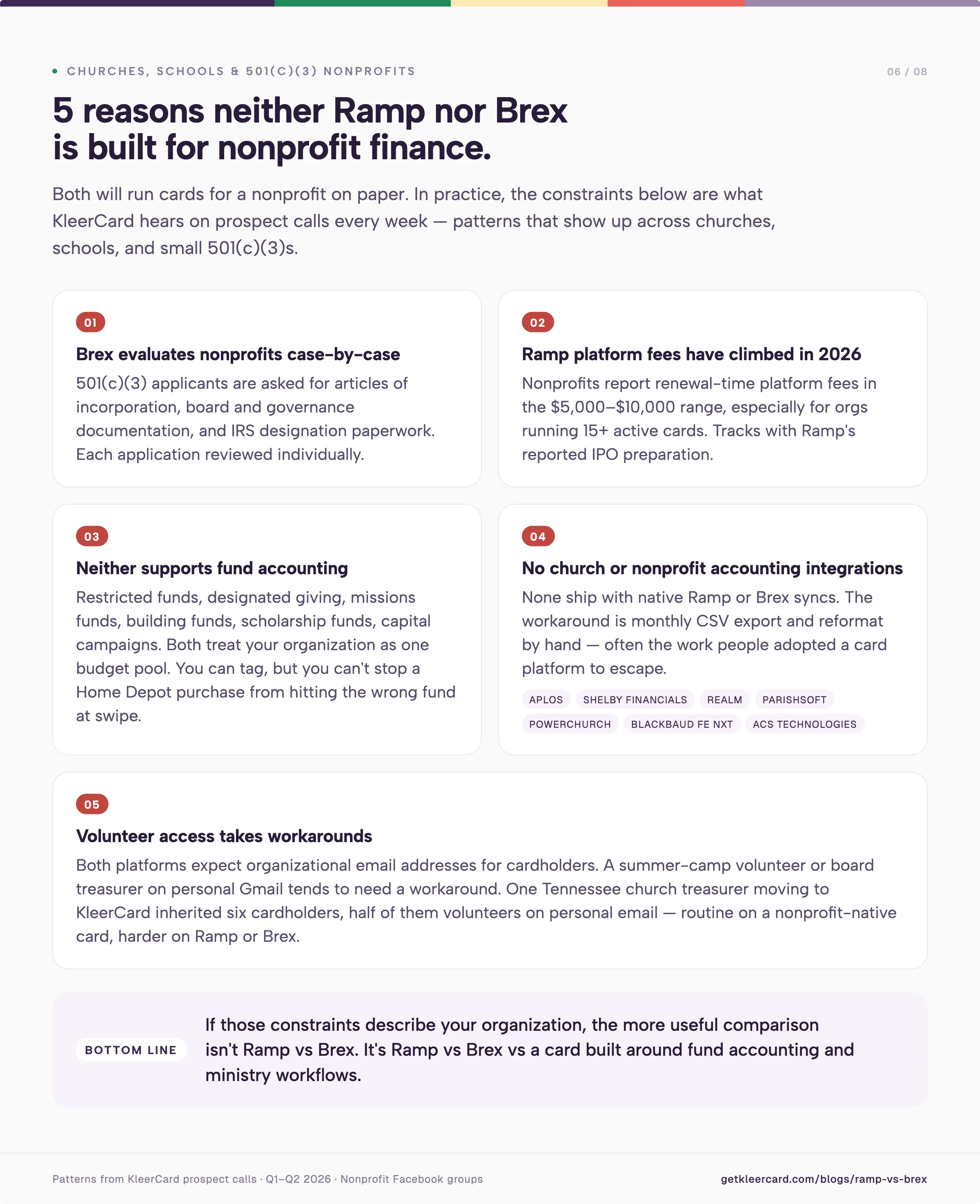

For churches, schools, and 501(c)(3) nonprofits, the constraints get more specific. A few patterns we hear from prospect calls at KleerCard through Q1 and Q2 2026:

- Brex evaluates nonprofits case-by-case. Brex's own documentation asks 501(c)(3) applicants for articles of incorporation, board and governance documentation, and IRS designation paperwork. Each application is reviewed individually. The underlying credit model was built for venture-backed startups with cash on hand, not for organizations funded by donations or grants.

- Ramp accepts nonprofits, but platform fees have climbed in 2026. A number of nonprofits we've talked with have reported Ramp adding platform fees at renewal in the $5,000-$10,000 range, especially for organizations running 15 or more active cards. The shift tracks with Ramp's reported IPO preparation at a ~$32B valuation. We see the pattern in nonprofit Facebook groups and in our own discovery calls.

- Neither platform supports fund accounting natively. Restricted funds, designated giving, missions funds, building funds, scholarship funds, capital campaigns. None of these live inside Ramp's or Brex's data models. Both treat your organization as one budget pool. You can tag transactions after the fact, but you can't stop a Home Depot purchase from hitting the wrong fund at the point of swipe.

- Neither integrates with church or nonprofit accounting software. Aplos, Shelby Financials, Realm, ParishSOFT, PowerChurch, Blackbaud Financial Edge NXT, ACS Technologies. None ship with native Ramp or Brex integrations. The standard workaround is monthly CSV export and reformat by hand, which is often the work people adopted a card platform to get away from.

- Volunteer access can be hard to set up. Ramp and Brex both expect organizational email addresses for cardholders. A summer camp volunteer or a board treasurer on personal Gmail tends to need a workaround. One Tennessee church treasurer who moved to KleerCard inherited a setup with six cardholders, half of them volunteers on personal email. That kind of setup is routine on a nonprofit-native card and harder on Ramp or Brex.

If those constraints describe your organization, the more useful comparison is Ramp vs Brex vs a card built around fund accounting and ministry workflows.

Eligibility: who qualifies for each

The most common reason someone rules a platform out is that they don't qualify on day one. Both Ramp and Brex publish their requirements.

Ramp eligibility (current)

Per Ramp's published support documentation, an applicant must:

- Be a corporation, LLC, LP, or nonprofit

- Hold at least $25,000 in cash in any connected U.S. business bank account

- Run most operations and corporate spending in the U.S. (international transactions supported)

- Have a valid EIN

- List a U.S. physical address (no PO boxes, no virtual offices, no registered agent addresses)

Sole proprietors and unregistered businesses don't qualify. Foreign owners can apply with a passport in place of an SSN.

Brex eligibility (current)

Per Brex's published account requirements:

- Daily-payment accounts require less than the monthly-payment thresholds below

- Monthly-payment accounts for funded startups: $50,000 cash minimum (sometimes lower with partner referrals)

- Monthly-payment accounts for bootstrapped commercial businesses: $1M+ annual revenue

- Monthly-payment accounts for mid-market and enterprise: $400,000+ monthly revenue (~$4.8M annualized)

- Valid U.S. EIN, U.S. incorporation, U.S. operations, U.S. physical address

- Nonprofits case-by-case, with 501(c)(3) designation, board governance, and articles of incorporation reviewed by a Brex underwriter

How the thresholds shake out in practice

A bootstrapped services company doing $500,000 a year with $30,000 in the bank qualifies for Ramp and falls short of Brex's monthly-payment threshold. A venture-backed startup with $2M raised and $200,000 in monthly revenue qualifies for Brex but might find Ramp's cash requirement tight depending on burn rate. A church with $1.2M in annual giving and $80,000 in operating cash qualifies for Ramp; Brex will likely route the application into case-by-case review and ask for governance documentation before approving.

For nonprofits, Ramp is the cleaner path to approval. Brex's case-by-case review is real, but it tends to be slower, and the credit model wasn't designed for donation-funded organizations.

Three fit scenarios

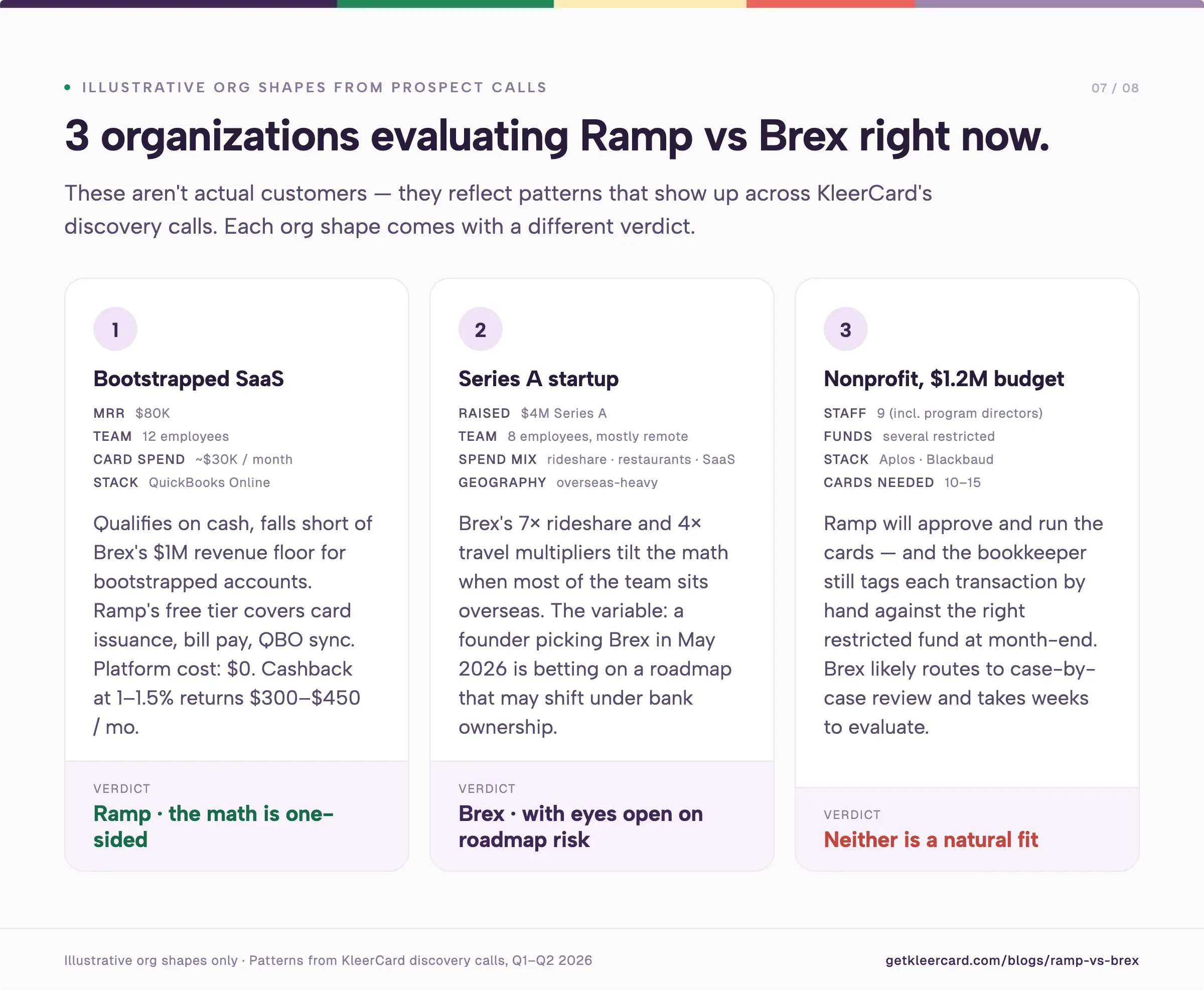

These are illustrative org shapes, not actual customers. They reflect patterns that show up in our prospect calls.

Scenario 1: Bootstrapped SaaS, $80K MRR, 12 employees

The math favors Ramp. The company qualifies on cash and falls short of Brex's $1M revenue threshold for bootstrapped accounts. Ramp's free tier covers card issuance, bill pay, and QBO sync. Total platform cost: $0. Cashback at 1-1.5% on $30,000 of monthly card spend returns $300-$450 a month.

Scenario 2: Series A startup, $4M raised, 8 employees, mostly remote

Either platform works. Brex's category-rich rewards and global card issuance tilt the math when most of the team sits overseas. The 7x rideshare and 4x restaurant multipliers add up for travel-heavy founder schedules. The Capital One acquisition is the variable to weigh. A Series A founder picking Brex in May 2026 is betting on a roadmap that may shift toward enterprise priorities under bank ownership.

Scenario 3: Nonprofit with $1.2M annual budget, 9 staff, several program directors

Neither product is a natural fit for this org shape. Ramp will approve the nonprofit and run the cards, and the bookkeeper will still tag each transaction by hand against the right restricted fund at month-end. Brex will likely route the application into case-by-case review and take weeks to evaluate. A platform built for nonprofits with native fund classification and church-accounting integrations is usually the better tool.

Where KleerCard fits

KleerCard sells neither Ramp nor Brex. We make a corporate card for churches, schools, and nonprofits, and we compete with both for that specific buyer. For most for-profit SMBs, KleerCard isn't the right answer.

KleerCard tends to be a good fit when:

- You run Aplos, Shelby Financials, Realm, ParishSOFT, ACS Technologies, or Blackbaud Financial Edge NXT as your accounting platform. Ramp and Brex don't integrate natively with any of these.

- You track spending against restricted funds, designated giving, missions budgets, VBS budgets, or capital campaigns. KleerCard maps card transactions to fund classifications at the point of swipe, with the GL code following from the fund assignment.

- You issue cards to volunteers, ministry leaders, or non-finance staff without organizational email addresses. KleerCard supports personal-email cardholders without setup friction.

- Your monthly card spend doesn't justify a $5,000-$15,000 platform fee. KleerCard pricing starts at $29/month (Standard, up to 15 users) or $49/month (Pro, up to 30 users), with no per-user fees on top.

- You want pricing predictability. We built KleerCard's pricing to hold up from day one, not as subsidized growth followed by post-IPO price hikes at renewal.

KleerCard tends to be the wrong fit when:

- You need to float net-30 or net-60 receivables. KleerCard runs on weekly billing cycles. For organizations whose grants pay 30-60 days after invoicing, SBA loans or a commercial line of credit are the right tools.

- You're a venture-backed startup with high international spend and 7x category rewards as a real budget line. Brex fits that profile better than we do.

- You want procure-to-pay automation, vendor negotiation tooling, and AI-powered savings intelligence as core features. Ramp's product depth on that side is ahead of ours.

For for-profit SMBs without nonprofit-specific needs, the choice comes down to Ramp vs Brex.

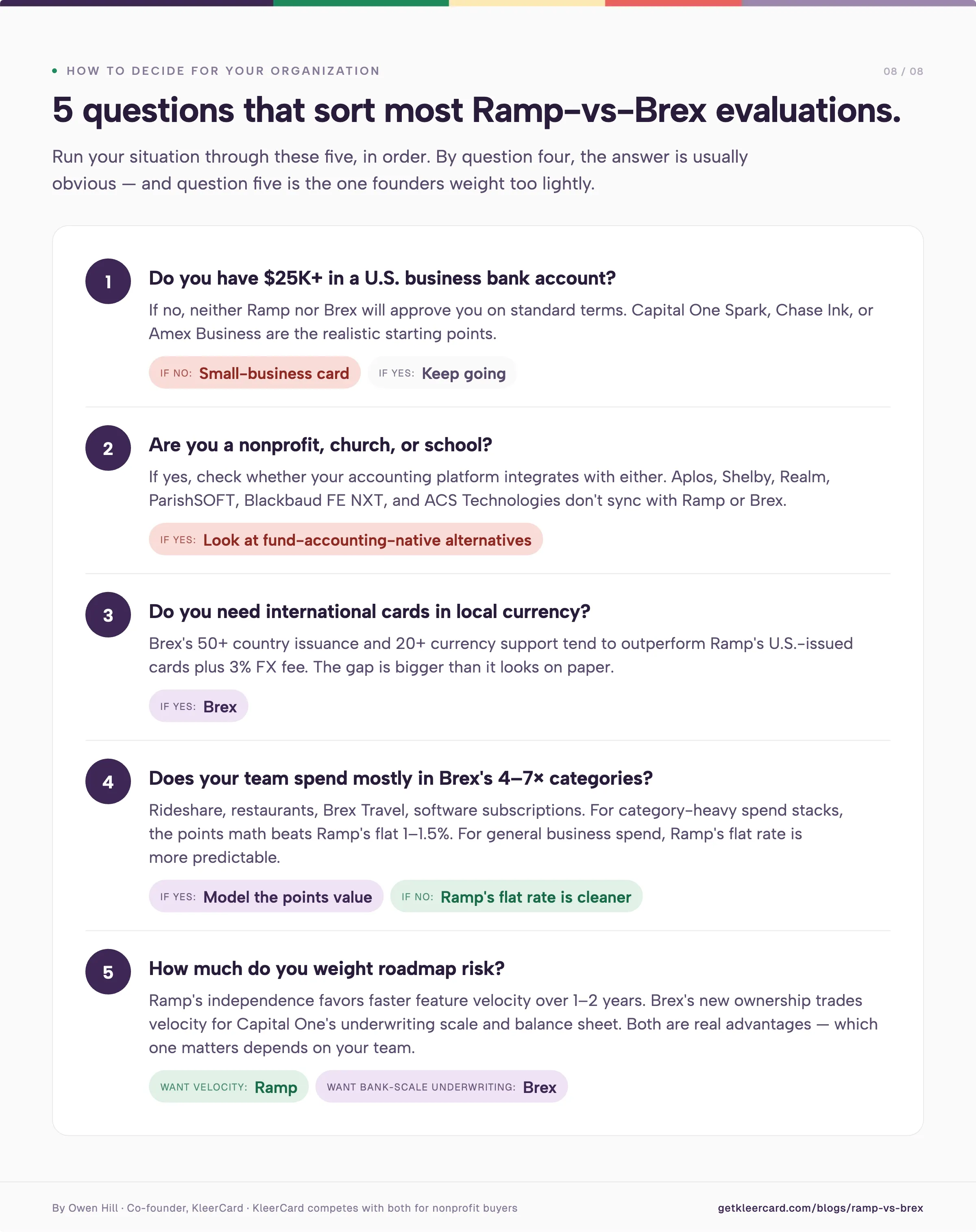

How to decide for your organization

Five questions tend to sort most evaluations:

- Do you have $25,000+ in a U.S. business bank account? If no, neither Ramp nor Brex will approve you on standard terms. Small business cards from Capital One Spark, Chase Ink, or Amex are the realistic path.

- Are you a nonprofit, church, or school? If yes, check whether your accounting platform integrates with Ramp or Brex. Aplos, Shelby, Realm, ParishSOFT, Blackbaud Financial Edge NXT, and ACS Technologies don't sync with either. Fund-accounting-native alternatives are worth a look. Our best credit cards for nonprofits guide covers a few.

- Do you need international cards in local currency? If yes, Brex's 50+ country issuance and 20+ currency support tends to outperform Ramp's U.S.-issued cards plus 3% FX fee.

- Does your team spend mostly in 4-7x Brex categories (rideshare, restaurants, travel, software)? If yes, it's worth modeling the Brex points value against Ramp's flat 1-1.5% cashback. For some spend profiles, the points math wins.

- How much do you weight roadmap risk? Ramp's independence favors faster feature velocity over the next year or two. Brex's new ownership trades velocity for Capital One's underwriting scale and balance sheet. Both are real advantages, and which one matters more depends on your team.

For most U.S. SMBs, Ramp tends to win on price, free-tier capability, ERP integrations, and roadmap independence. For globally distributed venture-backed startups with heavy travel and software spend, Brex tends to win on rewards and international infrastructure. For nonprofits, churches, and schools, neither is usually the best answer.

Frequently asked questions

Is Brex going away after the Capital One acquisition?

No. Brex still operates under its own brand with co-founder Pedro Franceschi as CEO. The acquisition closed on April 7, 2026, and Capital One says products, pricing, and support are unchanged for now. What will change over time is the product roadmap, the underwriting model, and the integration with Capital One's broader commercial banking stack. Capital One hasn't defined any of those changes yet.

Is Ramp or Brex cheaper?

For most small and mid-sized businesses, Ramp is cheaper on a published-price basis. Ramp's free tier covers cards, bill pay, expense management, and accounting sync. Brex's Essentials tier is also free, with fewer features. The paid comparison is closer. Ramp Plus costs $15/user/month plus a platform fee that varies by company size. Brex Premium costs $12/user/month last published. Both have negotiation room at scale. A 10-person team without multi-entity workflow needs tends to come out ahead on Ramp's free product.

Do Ramp or Brex work for nonprofits?

Ramp accepts nonprofits as eligible applicants. Brex evaluates nonprofits case-by-case and requires 501(c)(3) documentation, articles of incorporation, and board governance information. Neither has native integrations with church or nonprofit accounting platforms like Aplos, Shelby Financials, Realm, ParishSOFT, ACS Technologies, Blackbaud, or PowerChurch. Neither supports fund accounting in its data model. Most nonprofit users end up exporting CSVs and reformatting them by hand for fund tracking, which is often the work the card was supposed to eliminate.

Does Ramp or Brex require a personal guarantee?

Neither requires a personal guarantee or a personal credit check. Both evaluate your business's cash balance, revenue, and funding history to set a credit limit. Traditional small business cards from issuers like Capital One Spark or Chase Ink usually require a personal guarantee from the business owner and pull a personal FICO score.

Can I use Ramp or Brex as a sole proprietor?

No. Both platforms restrict eligibility to incorporated businesses: corporations, LLCs, and limited partnerships. Ramp's documentation states this directly. Brex requires a formal business structure with a U.S. EIN. Sole proprietors and unregistered businesses are usually better served by small business credit cards from major issuers.

What's the difference in rewards between Ramp and Brex?

Ramp offers up to 1.5% flat cashback, with the actual rate set by Ramp and varying by customer, per NerdWallet's review. Brex uses a points-based program with category multipliers: 1x base, up to 7x on rideshare, 4x on restaurants and travel booked through Brex Travel, and 2x on software subscriptions. For spend profiles heavy in those categories, Brex points can outpace Ramp's cashback. For spend that runs mostly software subscriptions and general business expenses, Ramp's flat rate is more predictable.

Will the Capital One acquisition affect Brex pricing or eligibility?

Capital One hasn't announced changes. Integration is expected to be gradual over the months following the April 7, 2026 close. One thing worth watching: Capital One's underwriting standards differ from Brex's startup-cash-balance model, and a shift toward bank-style credit standards could affect existing customers at renewal. Brex's customer base spans early-stage startups to large enterprises. Capital One's commercial banking customers tend toward larger, more established businesses. A roadmap shift toward those customers would change Brex's product priorities over time.

Which is better for a venture-backed startup right now?

Brex tends to be the better fit for most venture-backed startups in May 2026. Higher credit limits, 7x category rewards, 50+ country card issuance, and a more mature travel product all favor the funded-startup profile. The Capital One acquisition is the part to weigh. A founder who values an independent roadmap might look at Ramp for the 24-month window. A founder who values bank-backed underwriting scale and a larger credit ceiling gets that reinforced under Brex's new ownership.

A note on this comparison

Owen Hill, co-founder of KleerCard, wrote this article. KleerCard sells neither Ramp nor Brex. We make a corporate card for nonprofits, churches, and schools, and we compete with both products for that buyer.

If you want the church and nonprofit angle on either platform, our Ramp Card review for nonprofits and KleerCard vs Ramp for churches and nonprofits go deeper. To see what KleerCard does for your organization, sign up takes about five minutes.

Owen Hill co-founded KleerCard, a corporate card built for nonprofits, churches, and schools. He previously served as Budget Director at Compassion International, where he managed program budgets across dozens of country offices, and ran Switch Consulting, a fractional CFO practice for nonprofits. This article reviews KleerCard alongside Ramp, Brex, and other corporate cards.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)