%202.svg)

Last updated: April 27, 2026

If you handle finances for a church, nonprofit, or school, the BILL Divvy Corporate Card has probably landed on your shortlist. No annual fee. No personal guarantee. Free expense management software bundled in. The pitch is genuinely strong.

Full disclosure before we go further: KleerCard publishes this review, and we make a card that competes with Divvy. We've tried to keep this honest, and we'll point out where Divvy outperforms us along with where it falls short. If you want a fully independent take, NerdWallet, Nav, and Bankrate all have detailed reviews worth reading alongside this one.

We've spent years working with church treasurers, nonprofit CFOs, and school business managers. We've watched dozens of them sign up for Divvy, run it for six to nine months, and then call us frustrated about a rewards rule they didn't see coming or a control they assumed the card had but didn't. This review is the version we wish someone had handed them on day one.

Quick verdict up front: Divvy is a strong tool for stable for-profit SMBs with predictable monthly spend. For churches, nonprofits, and schools with seasonal cash flow or event-driven spending, the rewards program structure can erase what you'd otherwise earn, and some of the granular controls finance teams expect aren't available.

Key Takeaways

- BILL Divvy is a corporate charge card paired with free expense management software. No annual fee, no APR (it's pay-in-full), no personal guarantee.

- Rewards depend on how often you pay your balance. Weekly payers earn up to 7x on restaurants and 5x on hotels. Monthly payers earn 1x on most purchases.

- You generally need to spend at least 30% of your credit line each month to earn rewards for that period. Months below that threshold typically don't earn points, and skipping spending or missing payments can put accumulated rewards at risk.

- Points generally can't be redeemed until you've held the card for 12 months and accumulated at least 5,000 points.

- Foreign transaction fees apply, which matters for nonprofits running international missions.

- Virtual cards support budgets and expiration dates but aren't true single-use cards. There's no time-of-day restriction option, and there's no native integration with most church or donor management systems.

A note on KleerCard's trade-offs, since this table tilts in our favor: we don't offer cash back or points of any kind, and we charge a tier-based subscription. If your organization runs predictable monthly spend and you want rewards, Ramp's flat 1.5% is simpler than Divvy's tiered structure and doesn't carry the same penalties. We're a better fit for organizations that prioritize control over rewards.

What Is the BILL Divvy Corporate Card?

BILL Divvy is a corporate charge card paired with the BILL Spend & Expense platform. BILL.com acquired Divvy in 2021 for $2.5 billion and rebranded the product line to BILL Spend & Expense in 2023. Most people still call the card "Divvy."

A few things to understand up front:

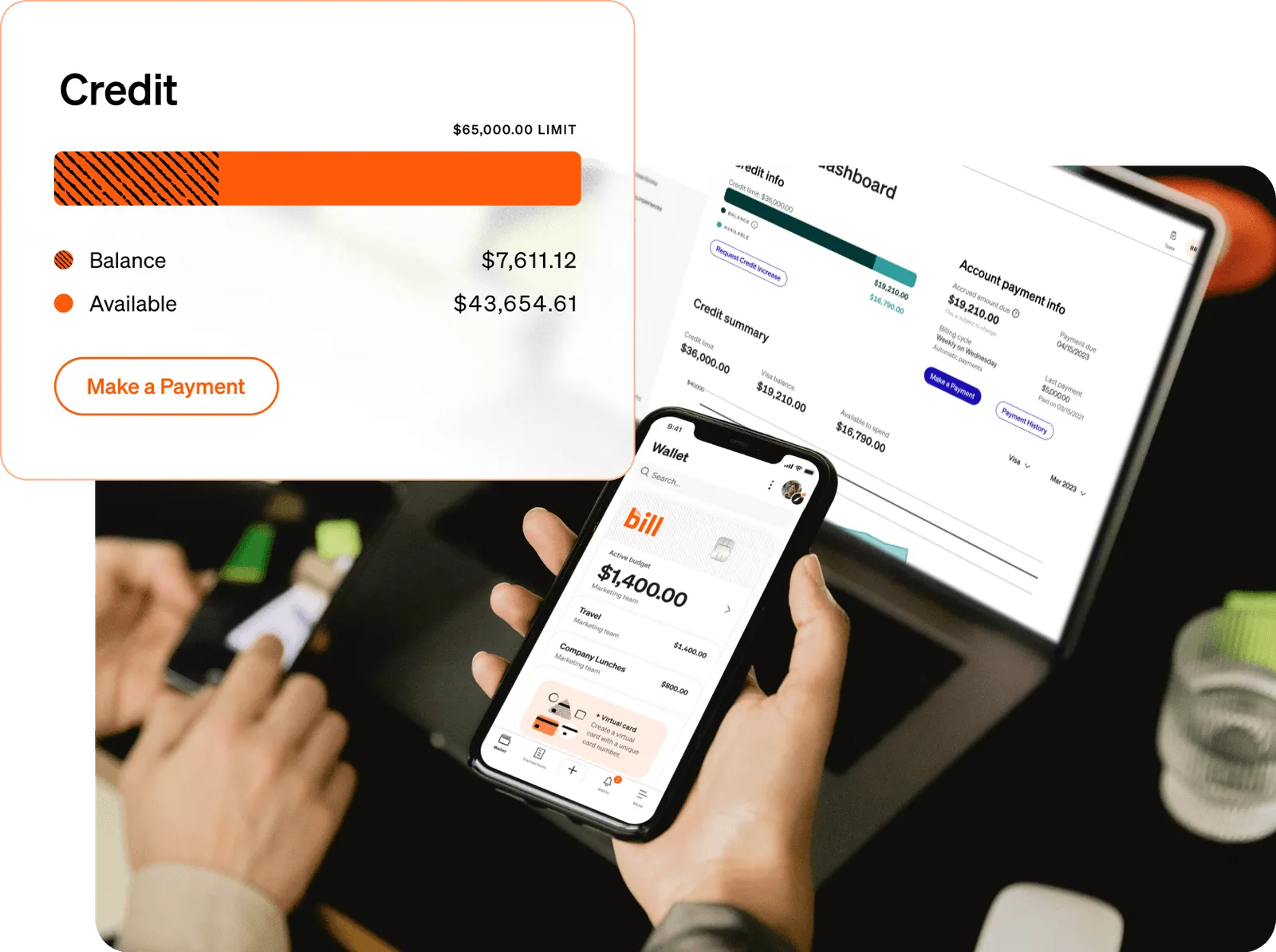

It's a charge card, not a credit card. You pay the full balance every billing cycle. There's no APR, no carrying a balance, and no minimum payment.

It's underwritten to your business, not to you personally. BILL evaluates your organization's bank balance, cash flow, and revenue history. Personal credit doesn't enter the equation, and no board member or executive needs to sign a personal guarantee. For nonprofit boards weighing personal liability concerns, that matters a lot.

The free spend management software is the real reason Divvy lands on so many shortlists. Standalone expense tools cost $5-$15 per user per month. Getting that functionality bundled with a no-fee corporate card is a serious offer, and one of the genuinely strong things about the product.

The catches show up in how the rewards work and what the card can't do. Both are worth understanding before you apply.

Rates, Fees, and Payment Structure

BILL Divvy keeps the fee structure clean:

- Annual fee: $0

- APR: None (it's a charge card)

- Foreign transaction fee: Yes, applies to international purchases

- Late fees: Apply if you miss a billing cycle, and missed payments can suspend your account

- Employee card fees: $0 (unlimited cards for staff)

You pick your billing cycle when you open the account: weekly, semi-monthly, or monthly. Most reviews don't tell you that this choice has a much bigger impact than just scheduling. It directly determines how many rewards points you earn.

For nonprofits and churches with international missions, the foreign transaction fee deserves more attention than it usually gets. If you send teams overseas or buy from international vendors, every purchase abroad costs you 1-3% extra. Ramp and Brex waive these fees, and so do we. Divvy doesn't.

How the BILL Divvy Rewards Program Actually Works

Most reviews bury the lead here. Divvy's rewards aren't really about what you buy. They're about how often you pay.

Multipliers vary by exact category and current promotional terms. Sources: NerdWallet, The Points Guy, and Bankrate.

Translation: pay weekly and the rewards look strong. Pay monthly and most of the marketing claims don't apply to you.

A few rules that often surprise new cardholders:

The 30% minimum spend rule. You generally need to run at least 30% of your credit line through the card each month to earn rewards for that period. So a $50,000 credit line means you need to push roughly $15,000 monthly to earn points that month. (NerdWallet confirmed this in their 2026 review.)

Risk to accumulated rewards. Inactive months and missed payments can put your accumulated points at risk. NerdWallet notes you can lose accrued rewards if you don't use the card in a given month, miss a payment, close your account within the first year, or fall below the spending threshold near year-end. The exact rules matter, so read your terms carefully before you commit. The practical effect: organizations with seasonal or irregular spending face real exposure here.

The 12-month redemption hold. You generally can't redeem points until you've held the card for 12 months and accumulated at least 5,000 points.

The bonus category cap. The 7x and 5x bonus rates apply only to the first $5,000 you spend in those categories each month. Everything above that drops to the base rate.

For a stable for-profit SMB with consistent monthly spend, this structure can be lucrative. For a church that runs heavier in November and December (year-end giving) and lighter in January and February, or a nonprofit that gets paid in irregular grant tranches, the math gets harder. Months below the 30% threshold don't earn rewards, and inactivity creates risk to what you've already accumulated.

This is the single biggest reason we don't recommend Divvy as the primary card for most churches and nonprofits.

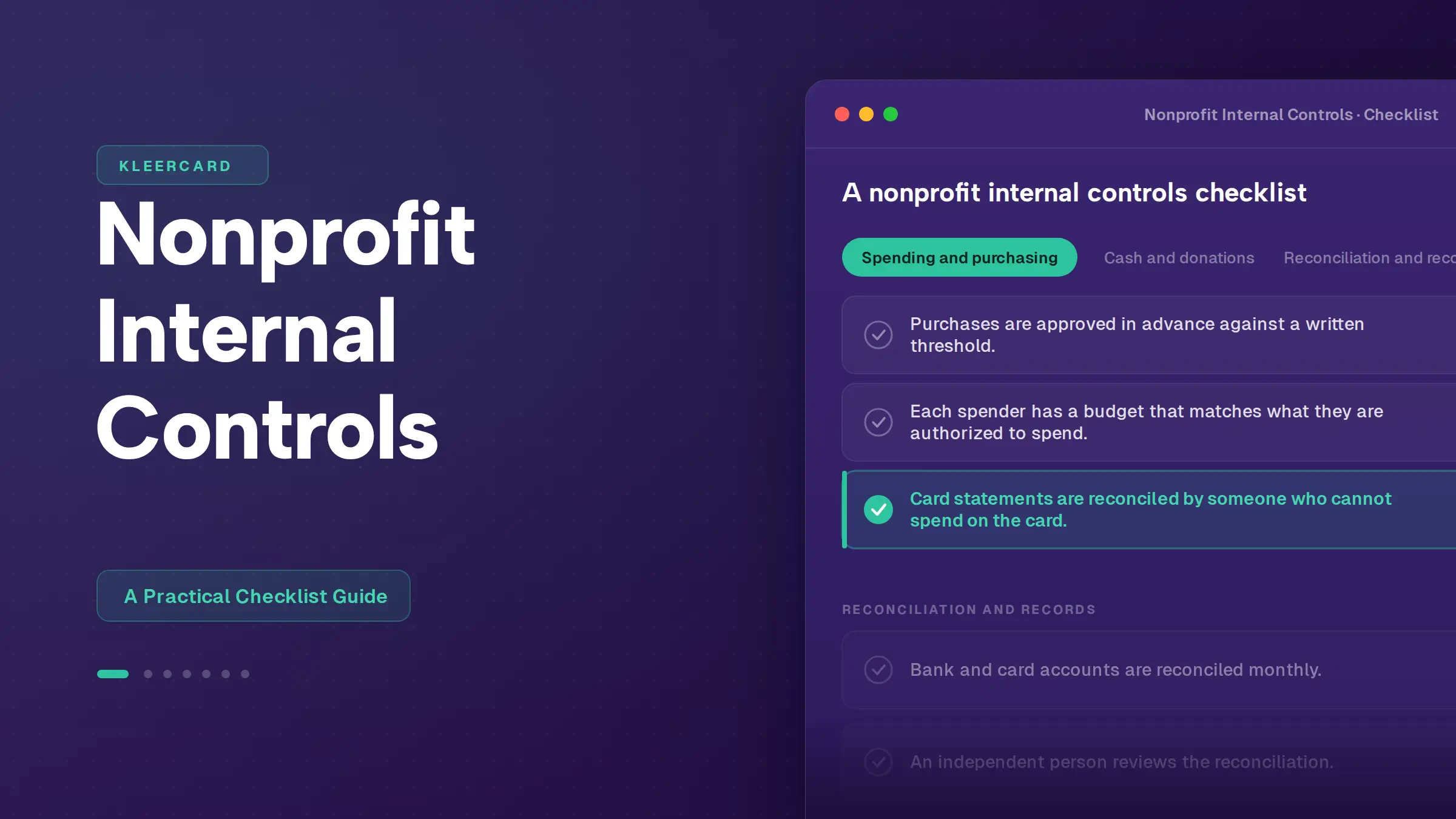

Expense Management and Card Controls

The expense software is where Divvy earns most of its loyal users. The platform itself is solid:

- Budgets. Set spending budgets by department, project, vendor, or employee. Managers approve any spend that pushes over the budget.

- Cards. Issue unlimited physical and virtual cards, each tied to a specific budget.

- Receipt capture. Employees photograph receipts in the mobile app and the system attaches them to the matching transaction.

- Accounting integrations. Divvy syncs with QuickBooks Online, NetSuite, Sage Intacct, and Xero.

- Real-time visibility. Admins see every transaction the moment it posts.

That's a serious toolkit for a free product. A finance team drowning in expense reports and chase-the-receipt emails can recover real hours every week by switching to Divvy. Credit where it's due: the platform is one of the most polished free spend management tools available, which is why so many SMBs adopt it.

But there are gaps that matter for organizations with stricter spending policies.

Virtual cards are flexible but not truly single-use. Divvy lets you create virtual cards with set budgets and expiration dates, which works well for ongoing vendor relationships and time-bound projects. What it doesn't offer is a card that automatically shuts off after a single transaction. For a one-time event purchase (a youth pastor's hotel booking, a single field trip vendor payment), a true single-use card adds an extra layer of protection against double-charges or accidental re-use. KleerCard and Ramp both offer single-use cards. Divvy's are budget-and-expiration based.

No time-based limits. Divvy lets you cap dollars and merchant categories. You cannot say "this card works on Saturday only" or "this card stops working after 8 p.m." For event-based spending (a weekend retreat, a one-day field trip), this is a meaningful limitation.

Limited integrations with nonprofit-specific tools. Divvy connects to mainstream accounting platforms but doesn't integrate directly with donor management software like Blackbaud or church management systems. Organizations whose financial workflow depends on those tools will handle reconciliation manually or build workarounds. KleerCard's integrations cover more of the nonprofit-specific stack.

Real user complaints from G2 and Reddit. Looking at BILL Spend & Expense reviews on G2, the most consistent themes are: the QuickBooks sync requires extra manual steps for some setups, customer support gets sluggish after the initial onboarding, and the app's auto-categorization gets things wrong often enough to require regular cleanup. Plenty of users also rate the platform highly, especially for the budgeting tools and ease of receipt capture. Read a sample of reviews yourself to gauge whether the complaints are dealbreakers in your context.

Pros and Cons for Churches, Nonprofits, and Schools

What Divvy gets right:

- No annual fee, no per-card fee, no per-user fee

- No personal guarantee, which protects board members and executives

- Strong, free expense management platform that compares well against paid standalone tools

- Direct integration with QuickBooks Online and other major accounting platforms

- Reports to the Small Business Financial Exchange, helping you build business credit

- Solid mobile app for employees uploading receipts on the go

- High potential rewards if you can pay weekly and have consistent spend

Where Divvy falls short for mission-driven organizations:

- The 30% monthly spend threshold makes rewards inconsistent for seasonal organizations

- Accumulated rewards can be at risk during inactive months or missed payments

- 12-month redemption hold delays any benefit from the rewards program

- Virtual cards aren't truly single-use (they're budget-and-expiration based)

- No time-based card restrictions

- Foreign transaction fees apply to international purchases

- Customer support quality varies, especially after onboarding

- No native integrations with donor management or church management systems

Who Should Consider BILL Divvy

Divvy works well for:

- Stable for-profit SMBs with consistent monthly spend across multiple departments and employees

- Companies with predictable cash flow that can pay weekly or semi-monthly to maximize rewards

- Teams replacing standalone expense management software where the bundled free platform alone justifies the switch

- Organizations with mostly domestic spending that won't run into foreign transaction fees

- Larger nonprofits with stable monthly operating expenses that comfortably exceed 30% of any reasonable credit line

If your organization spends $15,000+ monthly through a corporate card, has a finance team that can stay on top of weekly billing cycles, and lives mostly in the QuickBooks or Sage Intacct world, Divvy can be a strong pick.

Who Should Look Elsewhere

Divvy may not be the best fit if:

- Your spending is seasonal. Churches with year-end giving spikes and nonprofits with grant-driven income face inconsistent rewards earning and risk to accumulated points.

- You issue cards for one-time events. Field trips, mission trips, retreats, and conferences benefit from true single-use virtual cards.

- You need time-of-day or day-of-week restrictions. Volunteer-heavy organizations often want a card that only works during a specific event window.

- You spend internationally. Foreign missions, overseas conferences, and international vendor relationships make Divvy's foreign transaction fee a recurring cost.

- You use church management or donor management software. Divvy's lack of native integration creates manual reconciliation work every month.

- Your organization is small. If you can't comfortably hit 30% of whatever credit line you qualify for, the rewards program effectively becomes a non-feature.

For these organizations, KleerCard was built specifically for the way churches, nonprofits, and schools spend. We're transparent about our trade-offs: we don't offer cash back or points, we're a smaller and newer player than BILL, and we charge a per-user subscription rather than monetizing through interchange. We do offer single-use virtual cards, time-based limits, vendor-category restrictions, no foreign transaction fees, and direct integrations with the accounting and donor tools many nonprofits already use.

If you want both rewards and modern expense controls in a single product, Ramp is worth a look (1.5% flat cash back, no foreign transaction fees, no minimum spend). Brex offers tiered points with different rules than Divvy. Both are reasonable alternatives depending on your priorities.

How BILL Divvy Compares to KleerCard for Mission-Driven Organizations

The honest difference between the two products comes down to what you're optimizing for: rewards, or control.

Divvy optimizes for rewards. The whole product is built around getting you to pay weekly, spend at least 30% of your line, and run as many transactions as possible through the card. The expense management software is excellent, but it's there to support the rewards model.

KleerCard optimizes for control. We don't offer rewards because our customers tell us a small cash-back percentage isn't worth giving up the spending guardrails nonprofits actually need. A church treasurer would rather prevent a $300 unauthorized purchase than earn $3 in cash back on it.

That's a real trade-off. If your organization has predictable monthly spend and you'd rather earn rewards than tighten controls, Divvy or Ramp will serve you better than we will. We're upfront about that.

Concretely, here's what a school using KleerCard can do that a school using Divvy cannot:

- Issue a single-use virtual card to a teacher leading a field trip, preloaded with $500, that expires the day of the trip

- Set a card that only works at restaurants between 6 p.m. and 9 p.m. during a specific weekend retreat

- Block a card from working at certain merchant categories (no liquor stores, no streaming services)

- Issue refilling monthly stipend cards for each teacher's classroom budget that don't roll over unused funds

- Avoid foreign transaction fees on a missions trip abroad

If you've ever chased a volunteer for a receipt three weeks after an event, KleerCard's controls answer the actual problem. If you're already running a tight finance operation and just want bundled software with rewards, Divvy or Ramp will serve you well.

See how KleerCard compares for nonprofit, school, and church workflows, or explore the alternatives we recommend if you want a broader comparison.

Frequently Asked Questions

Is BILL Divvy a credit card?

Technically no. BILL Divvy is a corporate charge card, which means you pay the full balance every billing cycle. Unlike a traditional credit card, you can't carry a balance from month to month, and there's no APR. The benefit is that you avoid interest charges entirely. The drawback is you can't use the card to manage cash flow during slow months.

What credit score do you need for the BILL Divvy Corporate Card?

BILL recommends a business credit score in the good-to-excellent range, generally 670 or higher. Personal credit isn't checked, since BILL underwrites the card to the organization rather than to an individual. Approval depends more on your business's bank balance, cash flow patterns, and revenue history than on credit score alone.

What is the credit limit for the BILL Divvy Corporate Card?

Credit lines range from a few thousand dollars to $15 million, depending on your organization's revenue, cash reserves, and business history. BILL determines your specific limit during underwriting based on bank balances and cash flow rather than a fixed formula. Smaller nonprofits and churches often start with limits in the $5,000-$50,000 range.

Do you need a personal guarantee for the BILL Divvy Corporate Card?

No. One of Divvy's biggest advantages is that it doesn't require a personal guarantee. BILL evaluates your organization's financials, not your personal credit. This is a meaningful benefit for nonprofit board members and church leaders who don't want to be personally liable for organizational debt.

Does BILL Divvy charge foreign transaction fees?

Yes. Foreign transaction fees apply to international purchases. For organizations that send teams abroad on mission trips or buy from international vendors, this can add 1-3% to every overseas transaction. Ramp, Brex, and KleerCard all waive foreign transaction fees, making them better fits for organizations with international spending.

How does the BILL Divvy rewards program work?

Rewards depend on how often you pay your balance. Weekly payers earn up to 7x points on restaurants, 5x on hotels, 2x on software subscriptions, and 1.5x on everything else. Monthly payers earn 1x on most purchases. There's also a roughly 30% minimum monthly spend requirement to earn rewards, rules that put accumulated points at risk during inactive months or missed payments, and a 12-month hold before you can redeem. Read your cardholder agreement for the exact terms.

Can BILL Divvy help build business credit?

Yes. BILL Divvy reports payment activity to the Small Business Financial Exchange (SBFE), which shares data with major business credit bureaus like Equifax Business. Paying your balance on time consistently helps your organization establish or strengthen its business credit profile, which can improve access to financing later.

Is BILL Divvy good for nonprofits or churches?

It depends on your spending patterns. Nonprofits and churches with stable, predictable monthly spend can use Divvy effectively. Organizations with seasonal giving, grant-driven cash flow, or low monthly transaction volume often run into the 30% minimum spend rule and the rewards-forfeiture risks. For mission-focused organizations, KleerCard and other nonprofit-native cards typically offer better-fitting controls, though without the rewards potential Divvy offers when its rules work in your favor.

What's the difference between BILL Divvy and BILL Spend & Expense?

They're the same product, just renamed. BILL.com acquired Divvy in 2021 and rebranded the product to BILL Spend & Expense in 2023. The card is now formally called the BILL Divvy Corporate Card, and the platform that supports it is BILL Spend & Expense. Most users still refer to the whole package as "Divvy."

Can I redeem BILL Divvy rewards immediately?

No. You generally have to hold the card for 12 months and accumulate at least 5,000 points before you can redeem anything. Past that threshold, you can redeem for travel (highest value), gift cards, statement credits, or cash back. Travel offers the best per-point value.

The Bottom Line

BILL Divvy is a well-designed corporate charge card with one of the strongest free expense management platforms on the market. For stable for-profit SMBs with consistent spending and the discipline to pay weekly, the rewards stack up. The platform alone is good enough that plenty of organizations adopt the card just to get the software.

For churches, nonprofits, and schools with seasonal giving, grant tranches, irregular event-driven spend, foreign mission trips, or one-time volunteer purchases, Divvy's rules create friction. You'll either work around them constantly or accept that rewards will be inconsistent for your organization.

If you're a nonprofit, church, or school evaluating Divvy, here's our honest take. The expense management software is genuinely good. The card itself is a fine choice if your spending is steady, predictable, and large enough to clear the rewards thresholds. If it isn't, look at alternatives that don't tie rewards to spending consistency.

KleerCard was built specifically for organizations like yours. Single-use virtual cards, time-based controls, vendor-category restrictions, no foreign transaction fees, and direct integrations with the tools you already use. We don't offer rewards, by design, because our customers tell us they'd rather have control. That's a trade-off worth considering, not a clear-cut win.

Whatever you choose, do it with eyes open. Read the cardholder agreement carefully, talk to a few peer organizations using the card, and check the third-party reviews from NerdWallet and Nav for an independent take.

See how KleerCard compares for your organization, or browse our full breakdown of the best credit cards for nonprofits if you want more options.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)