%202.svg)

There are two kinds of credit card programs in use at school districts today.

Traditional bank purchasing card (P-card) programs come from US Bank, Bank of America, or JPMorgan Chase under state cooperative contracts. Modern card platforms (KleerCard, Ramp, BILL Spend & Expense, Charity Charge) ship the card and the spend management software together.

Which one fits depends less on the card features and more on the school. A public K-12 district inside a state cooperative usually has the issuer decided already. An independent school, a charter management organization, or a parish school sets its own procurement policy and has real choice.

This guide walks through the three banks that dominate public-district contracts, the modern platforms and the schools they fit, what the New York State Comptroller and GFOA look for in any program, and where each option breaks down.

Quick answer: which credit card is right for your school district

Confirm current terms with each issuer before signing.

The fast comparison of credit cards for school districts

Who this guide is for

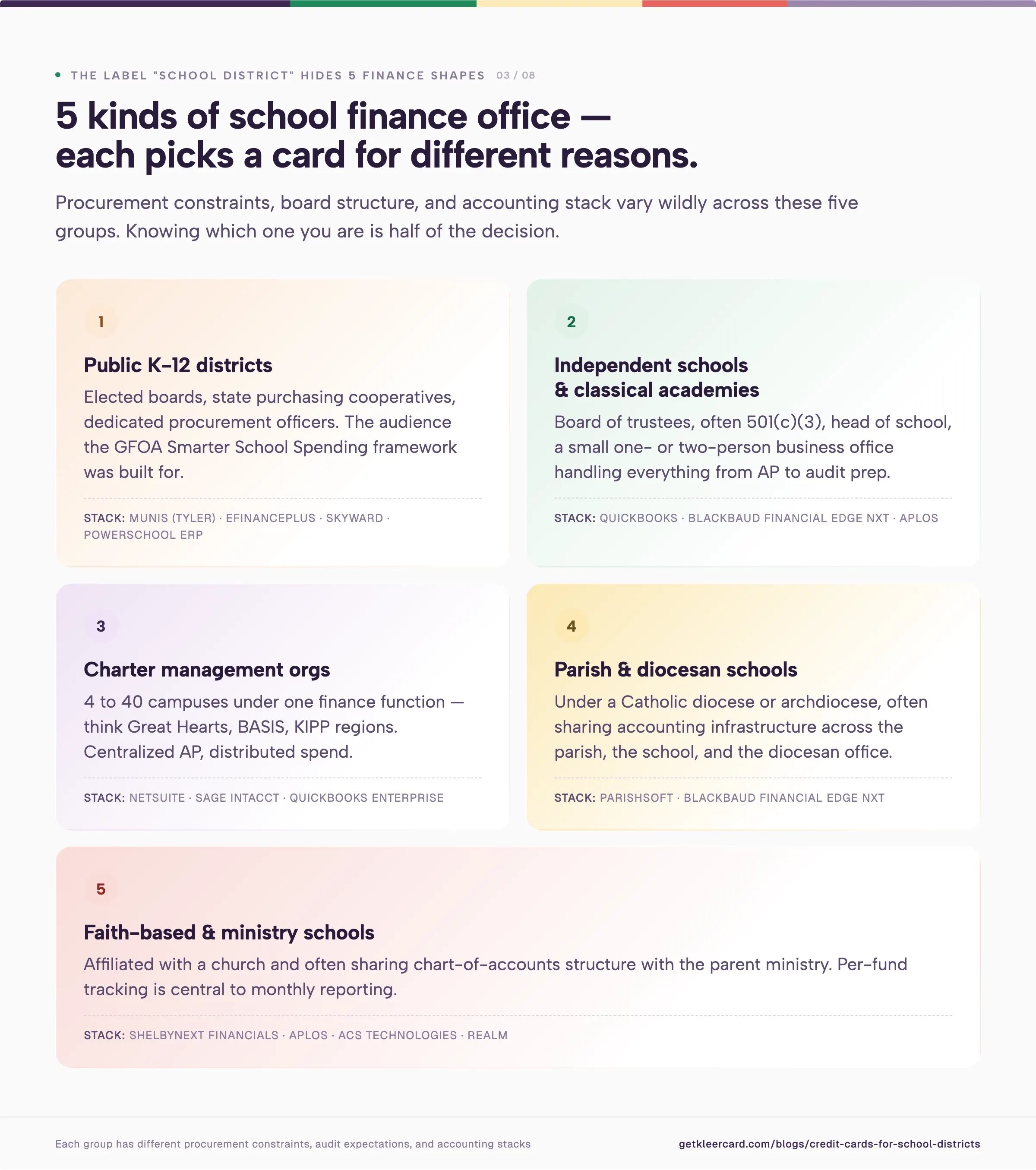

The label "school district" covers a wider range of finance offices than it sounds:

- Public K-12 districts with elected boards, state purchasing cooperatives, and procurement officers (the audience the GFOA Smarter School Spending framework was built for)

- Independent schools and classical academies governed by a board of trustees, often 501(c)(3), often with a head of school and a small business office

- Charter management organizations running 4 to 40 campuses under one finance function (Great Hearts, BASIS, KIPP regions)

- Parish and diocesan schools under a Catholic diocese or archdiocese, with shared accounting through ParishSOFT or Blackbaud Financial Edge NXT

- Faith-based and ministry schools affiliated with a church and often running ShelbyNext Financials or Aplos

Public K-12 business officers will get the most out of the next three sections: what a P-card program is, what auditors and the GFOA look for, and how the three major bank programs compare. Finance leaders at independent schools, charter networks, and parish schools can skip ahead to the modern card platforms and the evaluation framework. The 501(c)(3) schools in that group also fit the broader nonprofit credit card and spend management playbook.

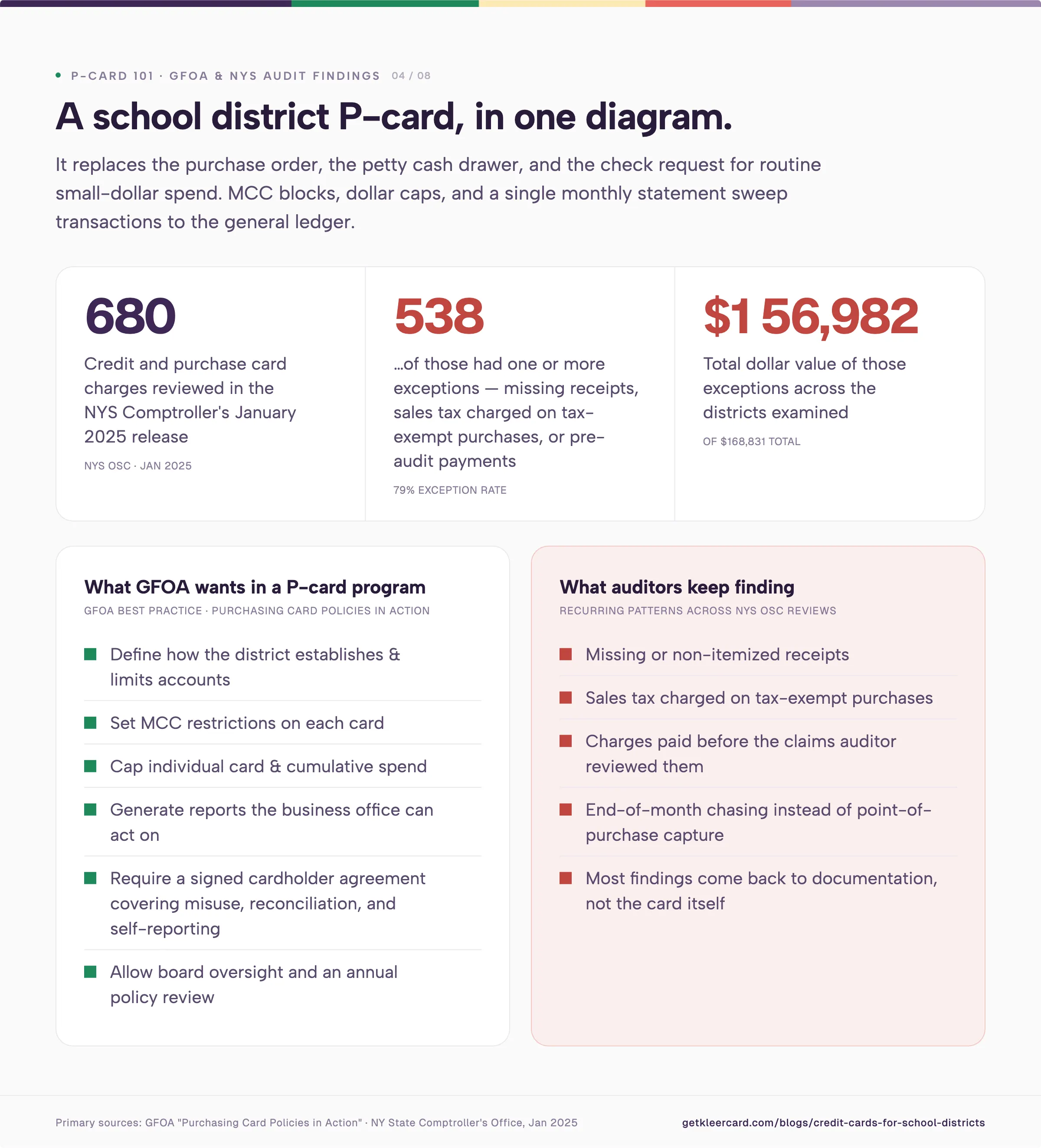

What a school district P-card does

A school district P-card (purchasing card) is a credit card issued to authorized district employees for small-dollar, high-volume purchases. It replaces purchase orders, petty cash, and check requests for routine procurement. Merchant category code (MCC) restrictions, dollar limits, and a monthly statement keep everything reconciled back to the district's general ledger.

The Government Finance Officers Association recommends that governments adopt P-card programs to clear out the paperwork around small purchases. Without one, finance teams generate purchase orders, invoices, petty cash transactions, and checks for every $40 box of paper towels. With one, a single monthly statement sweeps transactions into the general ledger by GL code and cost center.

Per GFOA best practice, a district P-card program should at minimum:

- Define how the district establishes and limits accounts

- Set merchant category code restrictions on each card

- Cap individual card spend and cumulative spend

- Generate reports the business office can act on

- Require a signed cardholder agreement covering misuse, reconciliation, and self-reporting

- Allow board oversight and an annual policy review

The New York State Comptroller's office audits school district P-card programs against most of those criteria. In a January 2025 release, auditors reviewed 680 credit card and purchase card charges totaling $168,831 across the districts examined and found that 538 charges (totaling $156,982) had one or more exceptions. The recurring patterns are familiar: missing or non-itemized receipts, sales tax charged on tax-exempt purchases, and charges paid before the claims auditor reviewed them.

Most of those findings come back to documentation rather than the card itself. Strong spend controls, clean MCC blocks, and real-time receipt capture reduce audit exposure. Manual receipt collection and end-of-month reconciliation increase it.

Traditional bank P-card programs for public school districts

Most public K-12 districts in the United States access card programs through a state cooperative purchasing agreement instead of negotiating directly with an issuer. Three programs dominate.

US Bank One Card / Visa Purchasing Card

US Bank's One Card is the most common public-district P-card across the western and Mountain West states. Granite School District (Utah), Alpine School District (Utah), and Millard School District (Nebraska) all run US Bank Visa P-card programs. The Nebraska Rural Community Schools Association offers it as a member benefit and earns a percentage of transaction fees.

A typical district setup:

- Issue one Visa P-card per authorized employee

- Let the purchasing director set MCC blocks at the district level

- Load the monthly statement into the district's AS400 or finance system around the 20th

- Have site administrators reconcile transactions before payment

- Cut one check a month for the entire district

The controls work, but they're coarse. Most districts can block restaurants, casinos, and adult-content merchants. Per-card category-level budgets and time-based locks are rarely available. Receipt collection runs through whatever process the business office sets up off the card.

Bank of America WORKS

Bank of America's WORKS payment management system is the standard P-card platform in South Carolina's state contract, used by York School District 1 and most other SC districts. Districts earn a rebate that flows back to general operations.

WORKS handles transaction allocation, GL coding, and cardholder reconciliation through a web portal. Documentation lives inside WORKS, or inside the district's accounting system, depending on how the district built the integration. Real-time visibility is more limited than what modern platforms provide.

JPMorgan Chase Commercial Card / Mastercard

North Dakota's Office of Management and Budget runs a Mastercard program through JPMorgan Chase that extends to state agencies, higher education, and political subdivisions (school districts included). The state's commercial card program covers 77 state agencies, 73 school districts, 13 colleges and universities, and dozens of counties and cities under one PaymentNet database.

Chase commercial cards also show up outside cooperative agreements, especially at independent schools and larger charter networks that already bank with Chase.

What traditional bank programs do well, and where they fall short

The strengths of bank P-card programs include established underwriting, high credit limits backed by the district's procurement budget, standard cooperative pricing, formats auditors and state comptroller offices already know how to read, and rebates that flow back into operations.

The limitations show up in a few places. MCC and dollar-cap controls are coarse, so per-card category budgets and time-based locks rarely exist. Receipt capture is manual, or bolted on through a separate expense tool. Reporting runs on a monthly cycle. Direct integration with school-specific accounting platforms (Aplos, Blackbaud, ParishSOFT, ShelbyNext, ACS Technologies) is rare or requires custom CSV mapping.

For a 35,000-student district running 800 transactions a day through a US Bank One Card program, those limitations are manageable. Procurement officers cover the missing pieces with separate expense management software, monthly reconciliation routines, and an internal audit cycle.

For a 600-student independent school or a 12-campus charter network, the same limitations land on a one- or two-person finance office, and the overhead doesn't scale down to that team size.

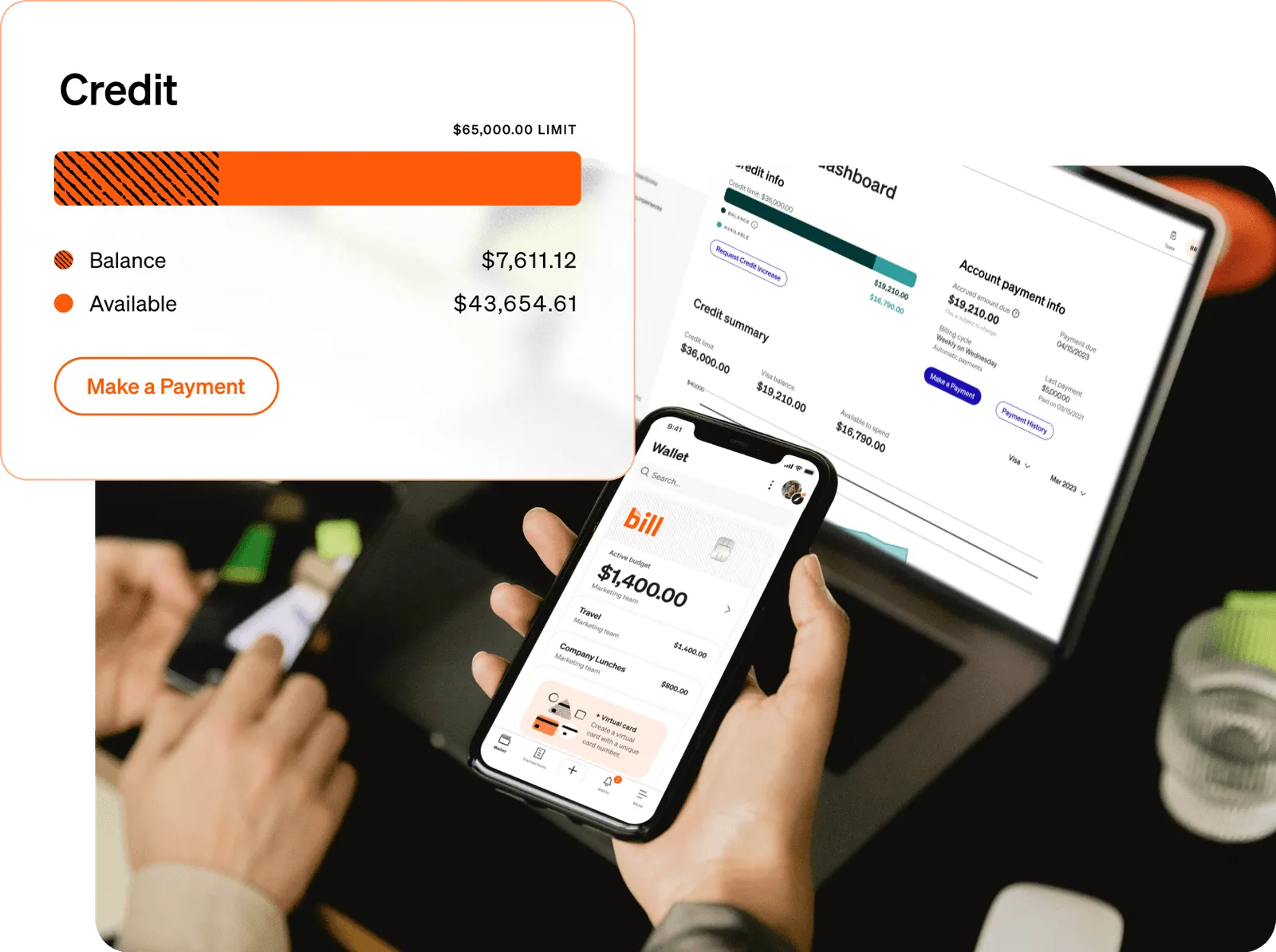

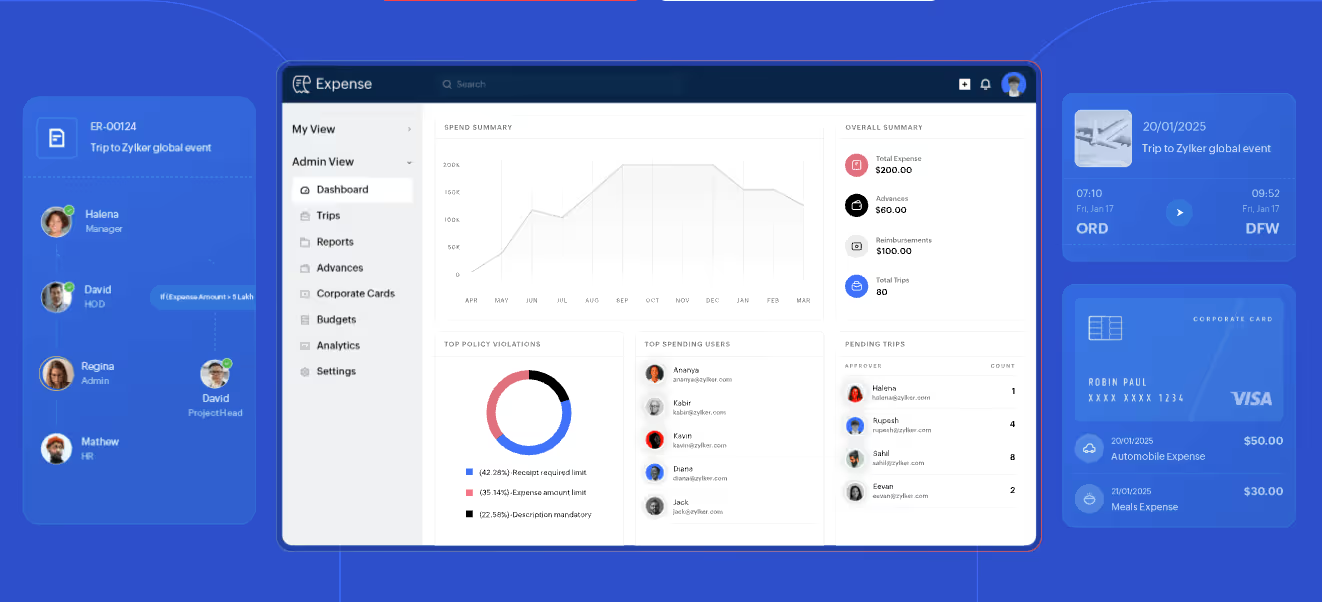

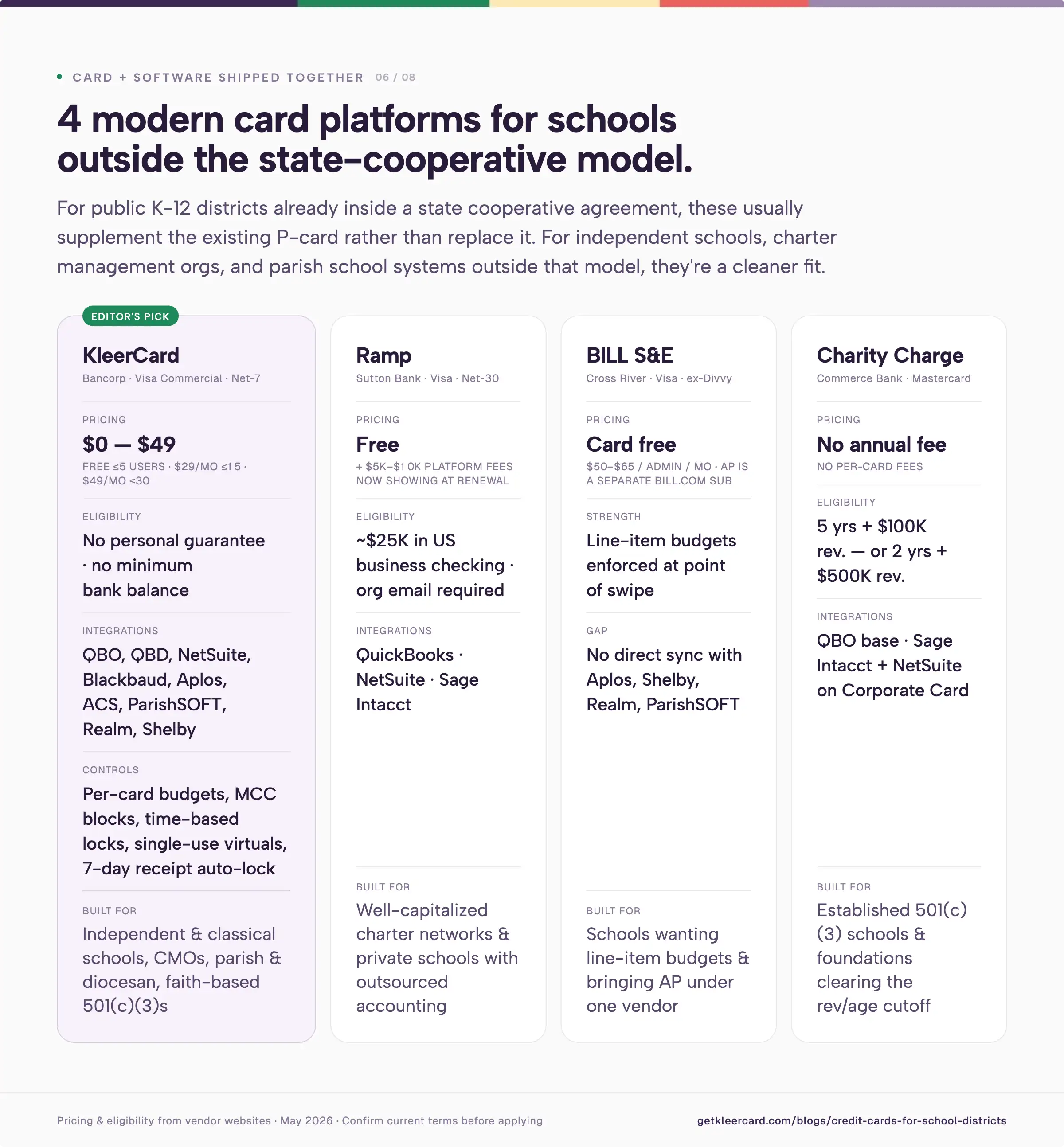

Modern card platforms for schools

Modern card platforms (KleerCard, Ramp, BILL Spend & Expense, Charity Charge, Brex) ship the card and the spend management software as one product. Controls, receipts, accounting sync, and reporting all live in the same dashboard.

For public K-12 districts already inside a state cooperative agreement, these platforms usually supplement the existing P-card. Switching the underlying bank program inside a state contract is rarely procurement-permissible. For independent schools, charter management organizations, and parish or diocesan school systems outside the state-cooperative model, modern platforms are often a cleaner fit.

KleerCard

KleerCard is built for nonprofits, churches, and schools. The KleerCard Visa Commercial card is issued by The Bancorp Bank, N.A.

The platform ships direct integrations with the accounting systems schools (including independent and faith-based schools) rely on: QuickBooks Online, QuickBooks Desktop, NetSuite, Blackbaud Financial Edge NXT, Aplos, ACS Technologies, ParishSOFT, Realm, and ShelbyNext Financials. The full list lives on the integrations hub.

A common use case is single-event spending, like a JV soccer tournament that needs hotels and meals over a weekend. The business office issues a virtual KleerCard capped at $850, restricted to lodging and restaurant MCC codes, set to expire Sunday night. The card shuts off when the tournament ends. Receipts upload through the mobile app on the bus ride home. The transactions sync to the school's accounting system overnight, coded to the athletic department's cost center. The athletic director doesn't carry a personal card or submit a reimbursement form after the trip.

I spent April 2026 on onboarding calls with school finance leaders running this kind of workflow. Tracy Taylor at Great Hearts Academies reported that consolidating onto KleerCard simplified the AP function across 24 campuses. Emily at Haven Classical School noted that the Amazon Business integration saved her staff time on routine ordering.

Pricing

- Free for up to 5 users

- Standard: $29/month for up to 15 users

- Pro: $49/month for up to 30 users

- Custom pricing above that

- Bill pay: $1 per ACH, $1.50 per check

- Cashback: available on custom plans for organizations spending roughly $30,000+/month on cards

Standard plans don't include cashback, and that's a deliberate trade-off. No card offers both unconditional cashback and the level of budget controls a school finance office usually needs. For most independent schools, predictable spending controls win out. Full details on the KleerCard pricing page.

Strengths

- Plug into the accounting platforms independent and parish schools already run

- Issue per-card budgets, MCC blocks, time-based locks, and single-use virtual cards

- Skip the personal guarantee and the minimum-bank-balance check

- Auto-lock cards after 7 days for missing receipts, so the receipt chase happens in software instead of on the business manager's plate

- Onboard in 2 to 3 thirty-minute calls, with time-to-first-transaction measured in hours

Where KleerCard does not fit

- Public K-12 districts already inside a state US Bank, Bank of America, or JPMorgan cooperative contract. Switching outside that contract usually isn't procurement-permissible.

- For-profit small businesses with 1 to 3 employees. An Amex or other personal-points card usually works better at that scale.

- Organizations that float against net-30 or net-60 receivables. KleerCard runs on a net-7 weekly payment cycle.

- Districts that need deep line-item budgeting controls of the kind BILL offers.

KleerCard's school customers are mostly independent schools, classical academies, charter management organizations, parish and diocesan schools, and other 501(c)(3) educational organizations outside the public state-cooperative model. The KleerCard application takes about eight minutes online, with approval usually within 48 hours.

Ramp

Ramp is a good fit for the organizations it was designed around. The platform launched in 2019 for tech companies and incorporated U.S. businesses, with AI-driven receipt matching, policy enforcement, and bill pay.

Public school districts and most independent schools are usually outside that core audience. Three eligibility issues come up in conversations I have with school finance leaders evaluating it.

- Ramp wants roughly $25,000 in a U.S. business checking account. Many independent schools run tight operating balances and keep reserves in money-market or endowment accounts that don't qualify.

- Platform fees of $5,000 to $10,000 are now showing up at renewal for existing customers. The pattern accelerated through early 2026 and tracks with Ramp's IPO preparation.

- Every Ramp user needs an organizational email address. Volunteer coaches, PTA and PTO treasurers, and board members on personal Gmail accounts can't be added without setup friction that KleerCard doesn't require.

For a well-capitalized charter management organization with stable cash flow and outsourced accounting, Ramp is a reasonable choice. For most independent schools, the math doesn't work out. Full breakdown in the Ramp Card review.

BILL Spend & Expense (formerly Divvy)

BILL.com acquired Divvy in 2021 and now sells the combined product as BILL Spend & Expense. The card platform itself is free. AP automation runs on a separate BILL.com subscription.

BILL's strength is line-item budgeting. You can set separate budgets for meals and lodging on the same trip, for example, and the platform enforces them at the point of swipe. For schools that want that depth, BILL is a credible choice.

There are three trade-offs to factor in. Administrator pricing runs $50 to $65 per month per administrator, which adds up when a finance team has four or five admins. There's no direct integration with fund accounting platforms like Aplos, Shelby, Realm, or ParishSOFT. And the card and bill-pay sides still don't share a fully unified data view inside BILL.com.

Full review in the BILL Divvy corporate card review.

Charity Charge Nonprofit Business Card

The Charity Charge Nonprofit Business Card is designed specifically for 501(c)(3) organizations. Commerce Bank issues the base card on the Mastercard network, with QuickBooks Online sync, no annual fee, and no per-card fees. Charity Charge also offers a Corporate Card for larger nonprofits with 180+ granular spend controls, OCR receipt capture, virtual cards, and ERP integrations including Sage Intacct and NetSuite.

The eligibility cutoff is where most smaller schools run into trouble. Per the Charity Charge FAQ, the Business Card requires either 5 years in operation and $100,000 in annual revenue, or 2 years in operation and $500,000 in annual revenue. That filters out smaller independent schools and most newer charter campuses, but it works for established schools and foundations.

Full review in the Charity Charge Nonprofit Business Card review.

What district CFOs and business officers should evaluate

The card matters less than the program built around it. Five questions cover most of what auditors and boards want to see.

1. Is the issuer inside our procurement cooperative or competitive procurement requirements?

For public K-12 districts, this question often answers most of the others. State cooperative contracts dictate the issuer, the underlying program, and most of the controls.

2. What is the spend-control granularity?

Coarse controls (MCC blocks plus a dollar cap per transaction) are the standard for traditional bank P-cards. Modern platforms add per-card budgets, time-based locks, and single-use virtual cards. Granularity matters more for athletic departments, field trips, and special events than for routine office-supply procurement.

3. How does receipt collection work?

The recurring NYS OSC audit finding (missing itemized receipts) is a documentation problem. Phone-based capture at the point of purchase, with automatic matching to the transaction, reduces it. End-of-month chasing usually doesn't.

4. How does the program integrate with our accounting system?

Public districts running Munis (Tyler Technologies), eFinancePLUS, Skyward, or PowerSchool ERP usually rely on CSV-based integration handled by the district's finance staff. Independent and faith-based schools running Aplos, Blackbaud, ParishSOFT, ACS Technologies, ShelbyNext, or QuickBooks can expect direct integrations from modern card platforms that traditional bank P-cards typically don't ship.

5. Does the cardholder agreement cover what auditors will look for?

Per GFOA, the cardholder agreement should spell out purchase limitations, repercussions for misuse, reconciliation responsibility, and how a user self-reports an unauthorized transaction. Both traditional bank programs and modern platforms ship standard cardholder agreements. The business office's job is making sure the district's adopted policy lines up with the program's controls.

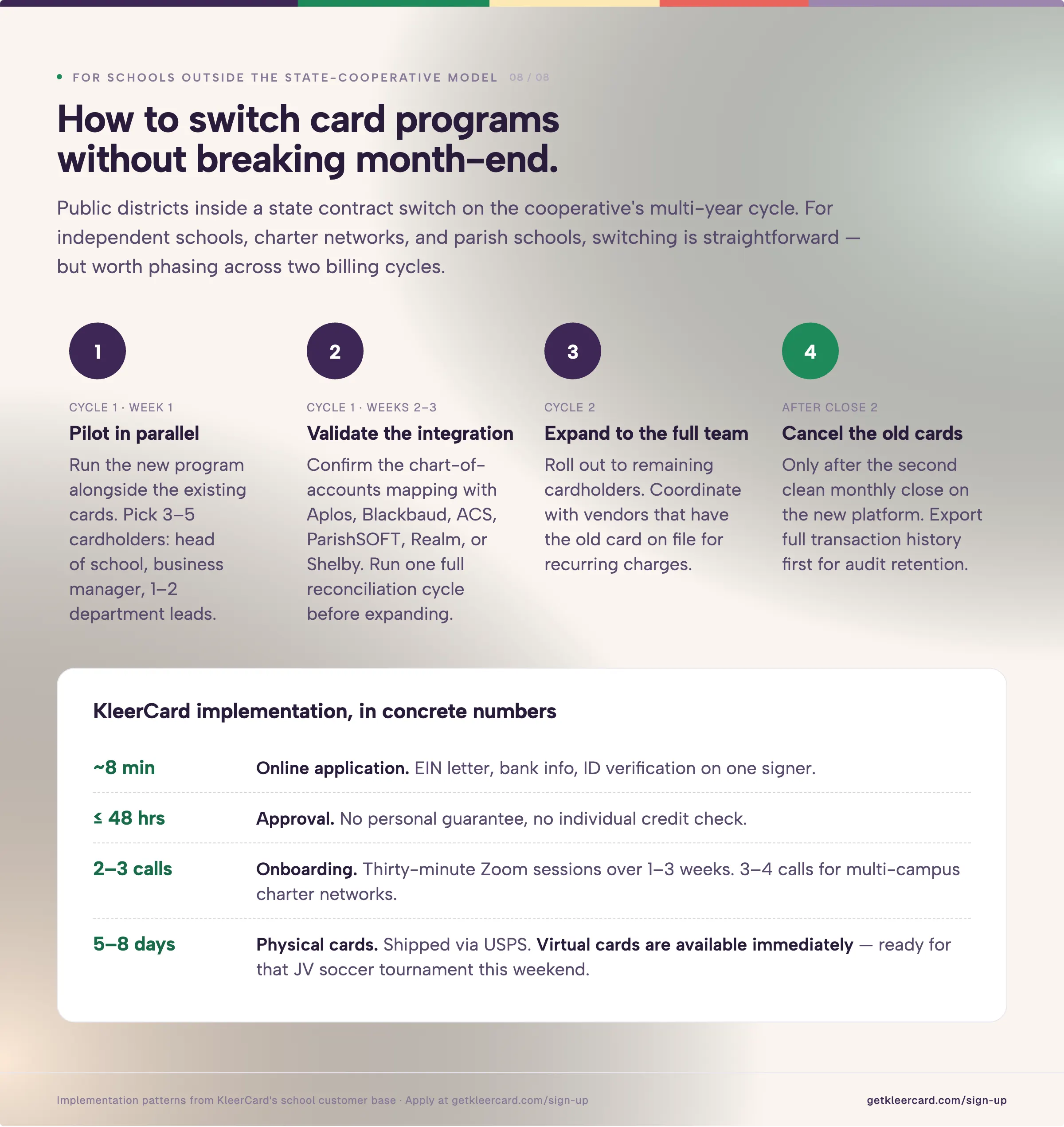

How to switch credit card programs (and what to plan for)

For a public district inside a state contract, switching the underlying issuer is a procurement event that runs on a multi-year cycle aligned with the state cooperative bid. Most districts won't run that decision themselves. The opportunity for change is at the renewal of the cooperative agreement.

For independent schools, charter networks, and parish schools outside the state-cooperative model, switching is straightforward but worth phasing.

- Run the new program in parallel with the existing cards for one billing cycle. Pick 3 to 5 cardholders to pilot: the head of school, the business manager, and one or two department leads.

- Validate the integration with your accounting system before you expand. For Aplos, Blackbaud, ACS Technologies, ParishSOFT, Realm, or Shelby, confirm the chart-of-accounts mapping and run one full reconciliation cycle.

- Expand to the full team in the next billing cycle.

- Cancel the old cards only after the second clean monthly close on the new platform.

KleerCard's typical implementation runs 2 to 3 thirty-minute setup calls over one to three weeks. Physical cards ship in 5 to 8 days via USPS. Virtual cards are available immediately.

For individual teachers spending out of pocket

The institutional card programs above are built for organizations, not individual classroom teachers. If you're a teacher covering classroom supplies and waiting on reimbursement, a personal cash-back card aimed at common classroom categories (office supplies, grocery, online retail) is often a reasonable option.

A few cards worth comparing: the Amazon Prime Visa returns 5% on Amazon and Whole Foods for eligible Prime members, the Blue Cash Everyday Card from American Express returns 3% on U.S. supermarkets, gas, and online retail, and the Wells Fargo Active Cash Card returns 2% flat on every purchase.

All three run a personal credit check and put personal liability on the cardholder. None carry institutional spending controls, fund accounting integration, or audit trails, which is why they work for personal out-of-pocket spending rather than organizational use.

If your school district handles classroom-supply reimbursement through a card program, the better setup is a virtual card with a small monthly classroom budget, capped at the right merchant categories, with receipts uploaded by phone. Platforms like KleerCard for educators run that workflow today. The conversation worth having with your business office is whether the program your school already runs supports it, or whether after-the-fact reimbursement is the only option available.

Frequently asked questions about credit cards for school districts

What is a school district P-card?

A school district P-card (purchasing card) is a credit card issued to authorized district employees for small-dollar, high-volume purchases. It replaces purchase orders, petty cash, and check requests for routine procurement, with merchant category code (MCC) restrictions, dollar limits, and a monthly statement that reconciles back to the district's general ledger.

Do school districts need a personal guarantee for credit cards?

Most district P-card programs are organizational credit programs that don't require a personal guarantee from the cardholder. The district's procurement budget backs the card.

Some smaller-volume business credit cards from traditional banks do require a personal guarantee from a board officer or business manager. Those are usually a poor fit for institutional school finance. The credit cards for nonprofits with no personal guarantee article covers the eligibility math in more detail.

Can a school district have a credit card without a state contract?

Yes. Independent schools, charter management organizations, parish schools, and other non-public K-12 institutions aren't bound to state cooperative purchasing contracts. They can pick any commercial card program that meets their procurement policy. Public K-12 districts inside a state cooperative are typically required to use the cooperative's issuer for any card program above a certain spending threshold.

What accounting software does a school district card need to integrate with?

It depends on the institution. Public K-12 districts most often run Munis (Tyler Technologies), eFinancePLUS, Skyward Business Plus, or PowerSchool ERP. Independent and faith-based schools more commonly run Aplos, Blackbaud Financial Edge NXT, ACS Technologies, ParishSOFT, Realm, ShelbyNext Financials, or QuickBooks (Online or Desktop). KleerCard ships direct integrations for the second group. Traditional bank P-cards usually rely on CSV exports for the first group.

How do school districts prevent credit card fraud and misuse?

The standard control stack is consistent across districts:

- A board-adopted credit card policy

- Signed cardholder agreements

- Merchant category restrictions

- Transaction and monthly dollar limits

- Real-time transaction alerts

- Itemized receipt requirements

- Supervisor reconciliation

- An annual internal audit

NYS Comptroller audits keep flagging missing or non-itemized receipts as the most common school district P-card finding. A program that automates receipt capture at the point of purchase reduces that exposure.

Can school districts earn cash back on a P-card program?

Many bank P-card programs return a rebate to the district based on transaction volume. Bank of America's WORKS, US Bank's One Card, and JPMorgan's commercial card all offer rebate structures that scale with volume.

Modern platforms vary. KleerCard offers cashback only on custom-priced plans (roughly $30,000+/month in card spend). Ramp offers 1% to 1.5% cashback, with the breakeven point against per-user fees landing in the 30 to 50 user range. For districts under 100 cards, cashback rarely drives program selection.

What is the difference between a P-card and a corporate credit card?

A P-card is procurement-focused, with tight MCC restrictions, individual transaction limits, and a focus on small-dollar high-volume purchases. A traditional corporate credit card is broader-use, with higher per-transaction limits, often used for travel and large-vendor relationships. Many districts run both: a P-card program for routine procurement, and a separate corporate card for the superintendent's office, executive travel, and large-event purchases.

How long does it take to set up a school district card program?

For a new program under an existing state cooperative contract, underwriting and card issuance typically runs 2 to 6 weeks. For a modern card platform like KleerCard, the application takes about 8 minutes online, approval comes within 48 hours, physical cards ship in 5 to 8 days via USPS, and virtual cards are available immediately. Full rollout across 15 to 50 cardholders usually runs 2 to 4 weeks with a phased pilot, parallel-running, and full expansion.

The bottom line on credit cards for school districts

For public K-12 districts already inside a state cooperative card program, the work is running the existing program well, with tight MCC controls, clear cardholder agreements, automated receipt capture wherever the existing platform allows it, and an internal audit cadence that lines up with state comptroller expectations.

For independent schools, charter management organizations, parish schools, and other educational 501(c)(3)s outside the state-cooperative model, modern card platforms are usually a cleaner option. KleerCard is built for that audience, with direct integrations into Aplos, Blackbaud, ACS Technologies, ParishSOFT, Realm, ShelbyNext, QuickBooks, and NetSuite, per-card budget controls, virtual cards, automated receipt capture, and no personal guarantee.

If your finance team is spending hours each month on manual receipt collection, statement reconciliation, or chart-of-accounts mapping, the program your team is using is likely a contributor. See how KleerCard works for educators, or open a KleerCard account.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)