%202.svg)

The short answer

Here are seven Brex alternatives worth looking at if you run a nonprofit, church, or school:

- KleerCard: built for nonprofits, churches, and schools with fund accounting

- Ramp: a good fit for funded startups and mid-market businesses with stable cash

- BILL Spend & Expense: works for small and mid-size businesses with cash flow but no venture funding

- Charity Charge: a 501(c)(3) card with cashback rewards

- Relay: a small-business banking platform with basic cards included

- Mercury: a banking platform for tech-adjacent 501(c)(3)s

- Airwallex: useful for international nonprofits with significant non-USD spend

Brex was built for venture-backed startups and mid-market commercial businesses. Their own help page says they work with nonprofits on a case-by-case basis, and the published underwriting thresholds make it hard for most churches, K-12 schools, and small-to-mid nonprofits to qualify.

Capital One closed its $5.15 billion acquisition of Brex on April 7, 2026, which is also worth thinking about if you're evaluating Brex for a multi-year relationship.

I'm one of the co-founders of KleerCard, so I want to be upfront about that. I've included KleerCard in this comparison because I think it's a real option for the audience this guide is for, but I've tried to write about it the way I'd write about any other card. Where another option is a better fit, I'll say so.

Brex alternatives at a glance

These numbers reflect publicly disclosed pricing and terms as of May 2026. They change often, so please verify with the provider before you apply.

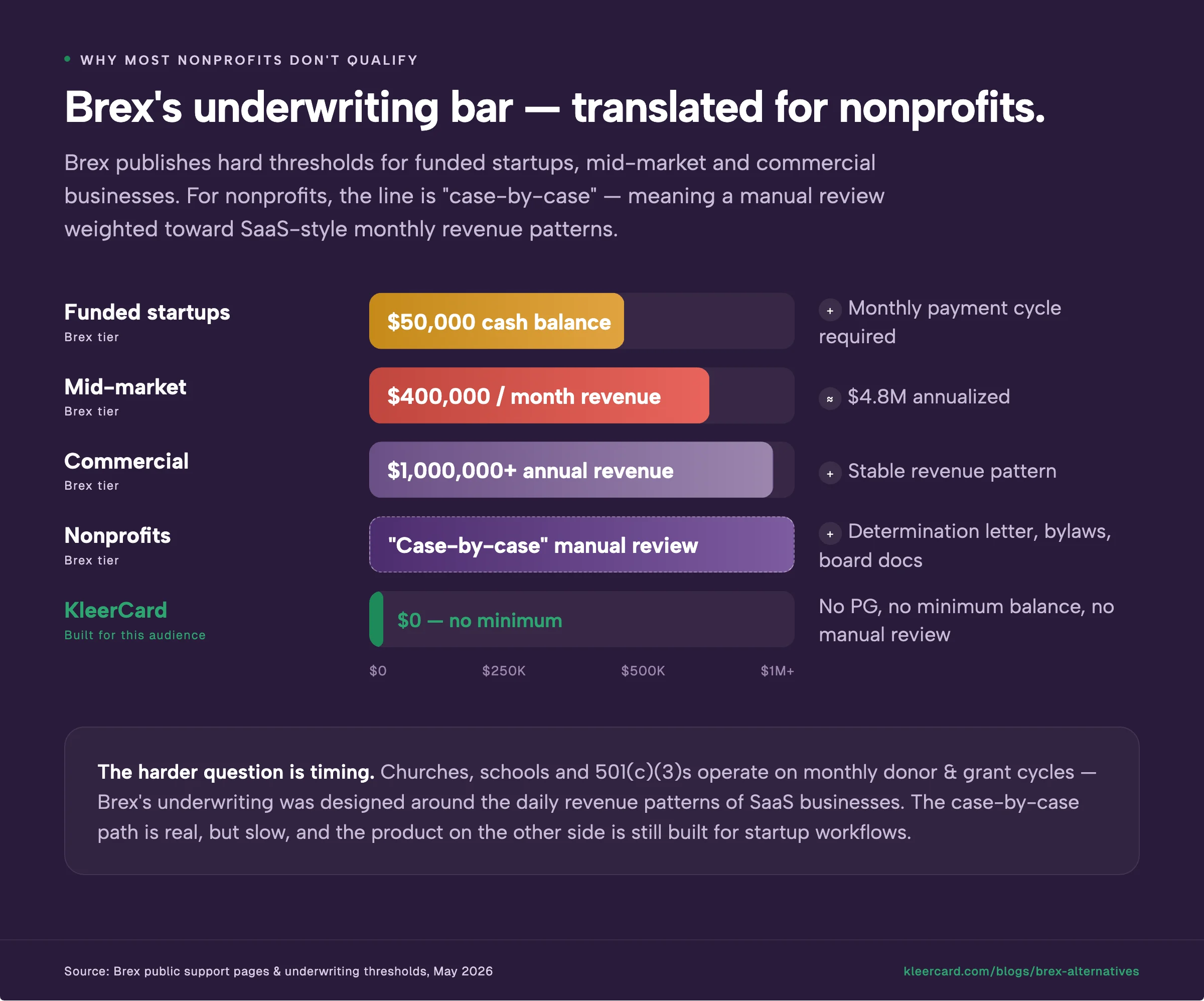

Why most nonprofits don't qualify for Brex

Brex requires you to be a US-incorporated entity with an EIN, a US address, and US operations. From there, their published thresholds are:

- Funded startups: $50,000 minimum cash balance to qualify for monthly payments

- Mid-market companies: more than $400,000 in monthly revenue (about $4.8M annual)

- Commercial businesses: more than $1 million in annual revenue

- Nonprofits: "We work with nonprofits on a case-by-case basis"

The nonprofit line is worth reading carefully. If you apply as a 501(c)(3), Brex will ask for your determination letter, articles of incorporation, board governance documents, and bylaws. Whether you're approved depends on their manual review, not a standard underwriting score.

A church with $1M in annual giving has the cash. A school district has the budget. A national 501(c)(3) running grants has the revenue.

The harder question is timing. All three operate on monthly donor or government funding cycles, while Brex's underwriting model was designed around the daily revenue patterns of SaaS businesses.

The case-by-case path is real, but it's slow, and the product you end up with is still designed for startup workflows. Credit limits move with your bank balance. Auto-pay runs daily or monthly. Rewards are weighted toward rideshare and SaaS subscriptions.

If you're a youth pastor trying to buy supplies for a weeklong VBS or a school administrator funding a senior trip, that workflow is going to feel like it was designed for a different kind of organization. Because it was.

What Capital One's acquisition of Brex means for your decision

Capital One announced the deal on January 22, 2026 and closed it on April 7, 2026. Brex CEO Pedro Franceschi is staying on. Day-to-day operations are continuing as before, and the product itself hasn't changed. Brex's own support pages now identify the company as a wholly owned subsidiary of Capital One, N.A.

The longer-term direction is the open question. Capital One is the sixth-largest US bank by assets and has committed nearly $1 billion to integration and retention over three years. Brex's roadmap, pricing, and underwriting decisions now sit inside a bank-led organization with different priorities than the independent fintech that built the original product.

I spent a few years as Budget Director at Compassion International before starting KleerCard, and I know that for a nonprofit, vendor stability isn't a minor concern. Annual budgets are set twelve months ahead. A mid-year pricing surprise from a card vendor can mean an emergency board conversation and a hole in the budget that has to come from somewhere. If you're choosing a card for a multi-year relationship, the acquisition is worth a few minutes of thought.

The 7 Brex alternatives compared

1. KleerCard

Best for: Nonprofits, churches, and schools running fund accounting.

KleerCard is a corporate card and spend management platform. The card is issued by The Bancorp Bank, N.A.

We built KleerCard for 501(c)(3) nonprofits, churches, and K-12 schools specifically. It isn't a card for venture-backed SaaS companies, e-commerce sellers, or global businesses running treasury operations in 20 currencies.

The integration list is where you can confirm what we focused on: Aplos, ACS Technologies, Realm, ChurchTrac, ParishSoft, Shelby, PowerChurch, Blackbaud, plus QuickBooks Online, QuickBooks Desktop, and NetSuite. These are the accounting platforms churches, schools, and nonprofits use.

Here's what KleerCard does for this audience:

- No personal guarantee and no individual credit check

- Per-card budgets with hard spending limits and merchant category controls. A card capped at $250 for restaurants will decline at $251.

- An auto-lock feature for missing receipts, so the finance team isn't the one chasing volunteers

- Fund accounting depth. Transactions tag to the right fund (general, missions, building, benevolence) at the moment of purchase, rather than at month-end.

- Flat pricing: $29/month for up to 15 users, $49/month for up to 30. No per-seat scaling.

- A weekly billing cycle (net-7)

KleerCard only offers cash back for organizations doing over $30k per month in spend.

KleerCard isn't the right tool for organizations that need to float receivables. The net-7 cycle doesn't cover net-30 or net-60 government and grant contracts.

Last quarter I had a conversation with the head of a workforce-development foundation running tutoring programs against net-60 partnership contracts, and we worked out together that what he needed was commercial banking and an SBA line of credit, not a card. KleerCard is a card platform, not working capital.

So: if you're a church, school, or nonprofit running fund accounting on Aplos, ACS, Shelby, or QuickBooks Online, KleerCard is likely a good fit. If you're a Series A SaaS company that needs to spend in 20+ currencies, it isn't.

See KleerCard pricing or open a KleerCard account.

2. Ramp

Best for: Funded startups and commercial mid-market businesses with stable monthly cash flow.

Ramp is the alternative Brex customers mention most often, and it's earned that reputation. They launched in 2019, they're independently owned, and they've built a strong product around corporate cards, expense automation, and bill pay. For the businesses Ramp was designed for, it's a good card. Their independence is also a real point in their favor now that Brex is owned by Capital One.

There are two places where Ramp tends to be a harder fit for ministry and nonprofit organizations.

The first is eligibility. Ramp requires at least $25,000 in a US business bank account, and they approve you based on the connected account.

A church with $40,000 in operating cash across designated funds might qualify on paper, but the underwriting model treats restricted funds as if they were available. For an organization running fund accounting, that's a different conversation. Restricted missions giving isn't the same as payroll cash.

The second is pricing predictability. Ramp's base tier remains free for the card and expense management, and that's a strong offer. What we've heard from churches and nonprofits in the past year is that platform fees of $5,000 to $10,000 have been appearing at renewal time, alongside per-user fees on paid tiers.

In April 2026, we heard from 13 churches and small nonprofits that this Ramp renewal pricing is becoming more common. For an organization on a fixed annual budget, that's the harder thing to plan around.

What Ramp does well: a mature product, fast feature development, deep ERP integrations (NetSuite, Sage Intacct, Workday, Oracle), and strong vendor management workflows. Where it's a harder fit for ministry: there are no native integrations with Aplos, ACS, Shelby, PowerChurch, ParishSoft, or Realm, and per-user pricing adds up when an organization issues cards to volunteers.

See our KleerCard vs Ramp for churches and nonprofits comparison for the head-to-head, or the Ramp card review for a full walkthrough.

3. BILL Spend & Expense (formerly Divvy)

Best for: Small and mid-size businesses with cash flow but no venture funding.

BILL Spend & Expense is the renamed Divvy product, now part of BILL.com. The underwriting reaches further into the small-business segment than Brex or Ramp. BILL will work with small businesses that don't have venture funding or a five-figure cash floor, and the platform combines corporate cards with per-budget controls, expense tracking, and bill pay.

For a nonprofit, BILL is worth considering if you want a card platform but have a thin cash position, if per-budget controls matter more to you than fund accounting depth, and if your books live in QuickBooks Online (which BILL syncs with natively).

Where it's a harder fit for churches and ministry-native organizations: BILL has no native sync with Aplos, ACS, Shelby, ParishSoft, Realm, ChurchTrac, or PowerChurch. Per-card budgeting works, but mapping transactions back to individual funds takes manual work in the accounting platform. Their rewards forfeiture rules have also been a point of contention with some customers historically, which our BILL Divvy Corporate Card review goes through in detail.

For traditional small businesses, BILL is a reasonable Brex alternative. For ministry organizations, the integration question is the one to look at most carefully.

4. Charity Charge

Charity Charge has a structure that's worth understanding before you compare it to anything else: they offer two different products through two different bank partners.

The Nonprofit Business Card is issued through Commerce Bank. The Nonprofit Corporate Card is issued through Fifth Third Bank by way of Corpay. Both are for 501(c)(3) organizations and both offer cashback rewards, but the feature sets and underwriting are different between them.

If a Charity Charge representative is showing you one of them, it's worth asking which of the two products you're being shown.

Both products share the same core value proposition: cashback flows back to the nonprofit's mission rather than to individual cardholders. For a national nonprofit with $5M in annual card spend, the cashback adds up to a real number.

Charity Charge is a good fit for 501(c)(3) organizations where cashback is something the board wants, for nonprofits whose books live in QuickBooks Online or a similar widely-supported platform, and for organizations that don't need ministry-specific fund accounting workflows.

It's a harder fit for churches and schools on Aplos, ACS, Shelby, ParishSoft, Realm, ChurchTrac, or PowerChurch (no native sync) and for organizations that need per-card budget caps with auto-decline. Of the two products, the Nonprofit Corporate Card has more spend controls than the Nonprofit Business Card.

See our Charity Charge Nonprofit Business Card review for the side-by-side comparison.

5. Relay

Relay is a digital business banking platform with built-in cards. It's not a corporate spend management tool the way Brex or Ramp is, and it doesn't try to be one. If you're a small nonprofit that wants a business checking account plus basic cards with light controls, Relay covers the basics. There's no minimum balance and no monthly fee on the base tier.

Relay tends to be a good fit for small nonprofits and microchurches under $250K in annual revenue, for organizations that want banking and cards in the same platform, and for teams of five or fewer cardholders.

It runs out of room when you grow past 10 cardholders and start needing real budget controls or fund accounting integration. Multi-campus or multi-ministry workflows are also outside what Relay is designed to handle.

6. Mercury

Mercury is a banking platform built for startups, and it has a strong reputation among technology founders. The 501(c)(3) audience Mercury serves well is on the narrow side: civic tech organizations, research foundations, and modern grantmaking entities. They offer checking and savings, a debit card (and an IO charge card for larger accounts), and basic spend management.

Mercury is worth considering if you're a technology-adjacent nonprofit, an organization under $5M with relatively simple finance needs, or a team that wants banking and cards from the same provider.

It's a harder fit for traditional ministry. There are no church accounting integrations, and the per-card spend controls are lighter than what KleerCard, Ramp, or BILL offer. Mercury applied for a national bank charter with the OCC in December 2025 and received conditional approval on April 27, 2026, which should reduce some of the historical concerns about sudden account closures.

7. Airwallex

Airwallex is built for organizations with international operations. International NGOs, mission-sending agencies funding field offices in multiple countries, and global advocacy groups all run into 3% foreign transaction fees and forced currency conversions when paying through US-domestic cards. On a six- or seven-figure annual international budget, those fees add up to real money.

Airwallex offers local accounts in 20+ currencies across 60+ countries, plus corporate cards that spend in local currency without conversion fees.

The fit is best for international nonprofits with field offices or contractors in multiple countries, for mission-sending organizations moving funds across borders every month, and for any 501(c)(3) where more than 20% of annual spend is in a currency other than US dollars.

If your operations are US-only, Airwallex isn't the right tool. The expense management layer is functional but less automated than Ramp or KleerCard for domestic workflows, and the integration depth is built around global treasury rather than US church accounting.

Best Brex alternative by organization type

Small nonprofits (under $500K annual revenue)

KleerCard is a good fit for this segment. The $29/month tier covers up to 15 users with no per-seat scaling, no personal guarantee, and no cash balance minimum. A small church with 3-5 cardholders usually starts with 2-3 cards in the first billing cycle and adds ministry leaders and volunteers over the next month or two. Our nonprofit credit card page walks through the broader workflow.

Relay is worth looking at if you want to consolidate banking and cards in one place and don't need granular spend controls. BILL Spend & Expense is a third option for small SMB-style nonprofits with a thin cash position and a QuickBooks Online setup.

Brex isn't a fit at this size. Ramp's $25,000 cash balance requirement screens most small nonprofits out before they finish the application.

Mid-size nonprofits ($500K-$5M annual revenue)

KleerCard's $29-$49/month tier scales to 15-30 users without per-user fees. Most mid-size customers spend a few weeks on onboarding (two or three half-hour calls), pilot with 2-5 cards for a billing cycle, and then roll out to the full team.

Ramp is a fit at this size if you have stable monthly cash flow, you can maintain $25,000+ in a US business checking account, and you don't depend on church accounting integrations. Charity Charge is a fit when cashback is important to your board and your books live in QuickBooks Online.

Brex's case-by-case nonprofit path opens up at this revenue level, but the product you end up with is still designed for SaaS workflows.

Churches (any size)

KleerCard is the most direct fit for churches. The integration list (Aplos, ACS, Realm, ChurchTrac, ParishSoft, Shelby, PowerChurch, Blackbaud, plus QuickBooks Desktop and Online) covers the accounting platforms most churches use. Transactions tag to the right fund (general, missions, building, benevolence, designated giving) at the moment of purchase, so there's no month-end re-coding.

A few examples from this year. A Tennessee church treasurer managing a $1M annual budget with 6 cardholders moved to KleerCard from CenterCard at $29/month after CenterCard's acquisition by Amex changed terms for churches under $4M in revenue. A Utah pastor switched from Concur ahead of the September 2026 Concur shutdown for similar reasons; the PowerChurch integration mattered most to him.

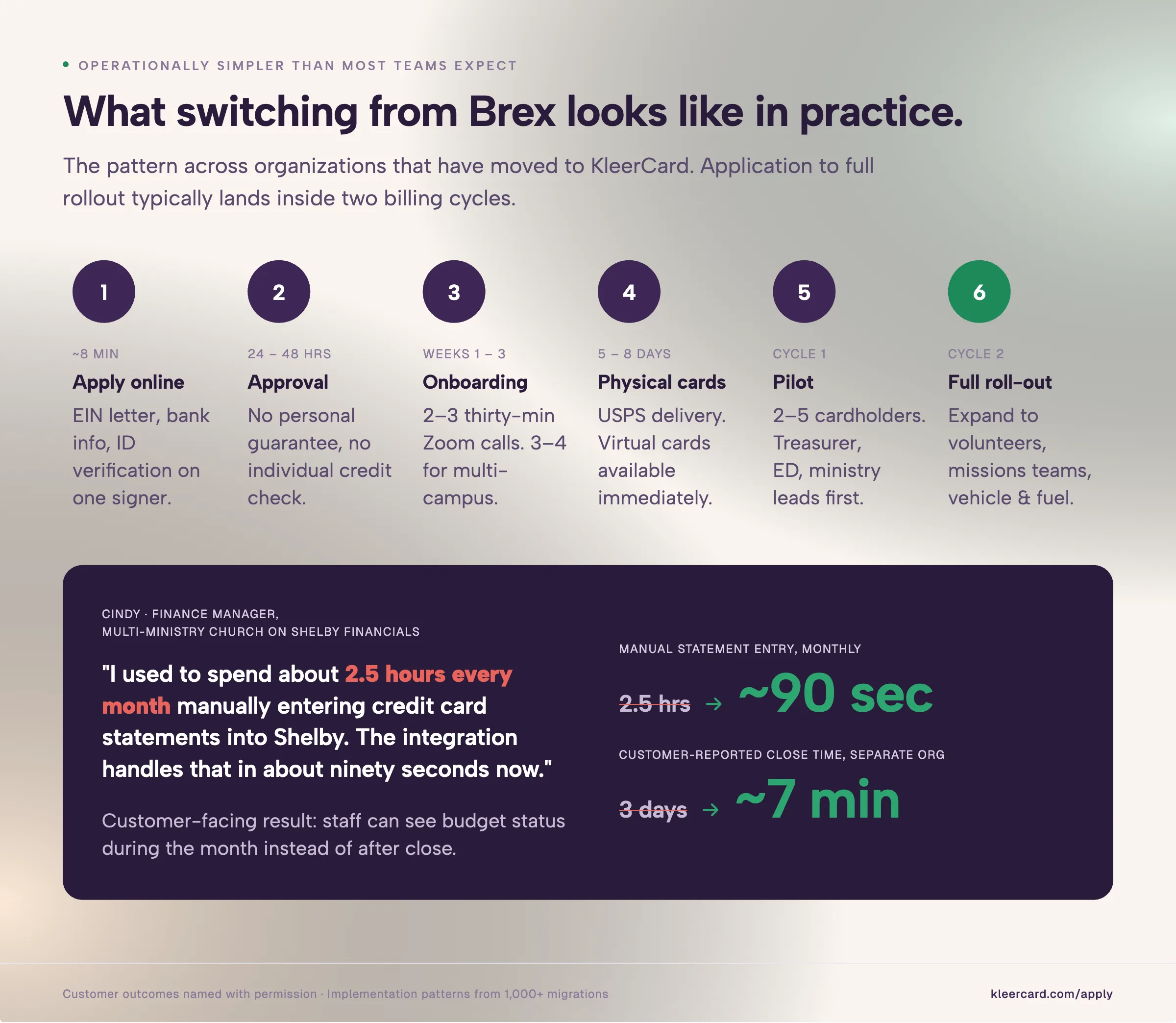

Cindy, a finance manager at a multi-ministry church on Shelby Financials, used to spend about 2.5 hours each month manually entering credit card statements before her team moved to KleerCard. The Shelby integration handles that work in about 90 seconds now, and her staff can see budget status during the month rather than after she closes the books.

Brex's case-by-case nonprofit path technically opens to churches. The product fit makes it harder. There are no church accounting integrations, no per-fund tagging, and the charge card semantics with daily or monthly auto-pay don't line up well with churches whose income arrives in monthly waves.

Our KleerCard for churches page goes into the workflow in more detail.

School districts and private schools

KleerCard is a good fit for K-12 schools running departmental cards, field trip cards, and discretionary purchases across athletics, music, and other programs.

An administrator can issue a virtual card preloaded with $500 for a teacher leading a field trip, set to expire after the trip ends. The card will decline at $501 and shut off when the trip is over. Teachers can capture receipts on the mobile app at the moment they make a purchase, which removes the reimbursement-and-paper-trail workflow that most schools are still running.

The Cindy example above translates fairly directly to K-12. The accounting platform is different, but the bottleneck looks the same: someone in the finance office spending hours re-keying card transactions every month, with no visibility for staff in between.

Brex isn't designed for this kind of workflow. Ramp can issue similar per-event cards, but the $25,000 minimum in a connected business checking account doesn't always line up with how school treasurer accounts are set up.

Our KleerCard for educators page goes through the school-specific workflow.

Ramp would be the next right fit, if you want a solution that’s not custom-built for nonprofits.

When Brex is the right answer

Brex makes sense when:

- You're a US-incorporated, venture-backed startup or a commercial mid-market business with $400K+ in monthly revenue

- Your accounting platform is NetSuite, Sage Intacct, or QuickBooks Online (not Aplos, ACS, Shelby, PowerChurch, or a church accounting system)

- You want credit limits that adjust dynamically with your bank balance

- Your team spends meaningfully on rideshare, SaaS subscriptions, and travel, where Brex's rewards categories add up

- You're comfortable with a bank-led, Capital One-backed underwriting model

If you're a venture-backed nonprofit that operates more like a tech startup (a small slice of 501(c)(3) organizations, usually civic tech or foundation-backed research orgs), Brex's case-by-case nonprofit path can work for you. For traditional churches, K-12 schools, and most small-to-mid 501(c)(3) nonprofits, the eligibility and the product design are both pulling in a different direction.

What switching looks like in practice

If you're thinking about switching cards, the operational question is usually how long it takes and what it costs the team internally. Across the organizations that have moved to KleerCard, a typical implementation looks like this:

- Application: about 8 minutes online. EIN letter, bank info, and ID verification on one signer.

- Approval: 24-48 hours. No personal guarantee required.

- Onboarding meetings: two to three thirty-minute Zoom calls for smaller organizations, three or four calls over three to four weeks for larger or multi-campus deployments.

- Physical cards: 5-8 business days by USPS. Virtual cards are available right away.

- Pilot rollout: one billing cycle with 2-5 cardholders.

- Full team rollout: the following billing cycle.

Most churches and nonprofits start with the treasurer card, the pastor or executive director card, and one or two ministry leader cards. After a billing cycle of working with those, they tend to expand to volunteers, hospitality, missions teams, vehicle and fuel cards, and seasonal program leaders. Larger deployments (multi-campus churches, school networks, the 24-campus systems we've onboarded) follow the same pattern at a larger scale.

The internal time cost is the part that tends to surprise people. After the initial setup, most of our customers run a weekly close on KleerCard with receipt capture and fund coding done by Tuesday morning each week. The 2.5-hours-per-month problem Cindy described earlier becomes a 30-second weekly check.

FAQs

What are the best Brex alternatives in 2026?

For most US-based nonprofits, churches, and schools, the realistic options are KleerCard (nonprofits, churches, schools), Ramp (funded startups and commercial mid-market), BILL Spend & Expense (SMBs with cash flow), Charity Charge (501(c)(3) cashback), Relay (small banking-plus-cards), Mercury (tech-adjacent 501(c)(3)s), and Airwallex (multi-currency operations).

Is Brex still operating after the Capital One acquisition?

Yes. Capital One completed the acquisition on April 7, 2026. CEO Pedro Franceschi is staying on, day-to-day operations have continued, and Capital One has committed nearly $1 billion over three years to integration and retention. Changes to the product, pricing, or underwriting are likely over time but haven't been announced as of May 2026.

Can nonprofits qualify for Brex?

Brex's support page says they work with nonprofits on a case-by-case basis. If you apply as a 501(c)(3), you'll be asked to submit your determination letter, articles of incorporation, board governance documents, and bylaws. There's no published cash or revenue threshold for nonprofits, but approval depends on Brex's manual review, which weights monthly revenue cycles and cash position heavily.

What's the best Brex competitor for a church?

For most churches, KleerCard is the most direct fit. It integrates with the accounting platforms churches use (Aplos, ACS, Realm, ChurchTrac, ParishSoft, Shelby, PowerChurch, Blackbaud) and tags transactions to the right fund at the moment of purchase. Pricing is flat at $29-$49/month, with no personal guarantee and no minimum cash balance.

What's the best Brex alternative for a school?

KleerCard, for the same reasons. Schools can issue per-department, per-teacher, and per-event cards with hard spending limits and merchant category controls. An administrator can issue a $500 single-event card that expires after the trip and declines on the first dollar over budget.

Which Brex alternatives work without a personal guarantee?

KleerCard, Ramp, Mercury, Airwallex, and Charity Charge underwrite the organization rather than the individual. None of them require a personal guarantee or a personal credit check. BILL Spend & Expense may ask for a personal guarantee depending on the underwriting profile. Our credit cards for nonprofits with no personal guarantee guide has the full comparison.

What's the cheapest Brex alternative?

For an organization under 15 users, KleerCard at $29/month and BILL Spend & Expense (no monthly fee for the card platform) are the lowest published costs. Ramp's free base tier looks competitive on paper, but the renewal-time platform fees of $5,000-$10,000 that some customers have reported in 2025-2026 can change the math significantly.

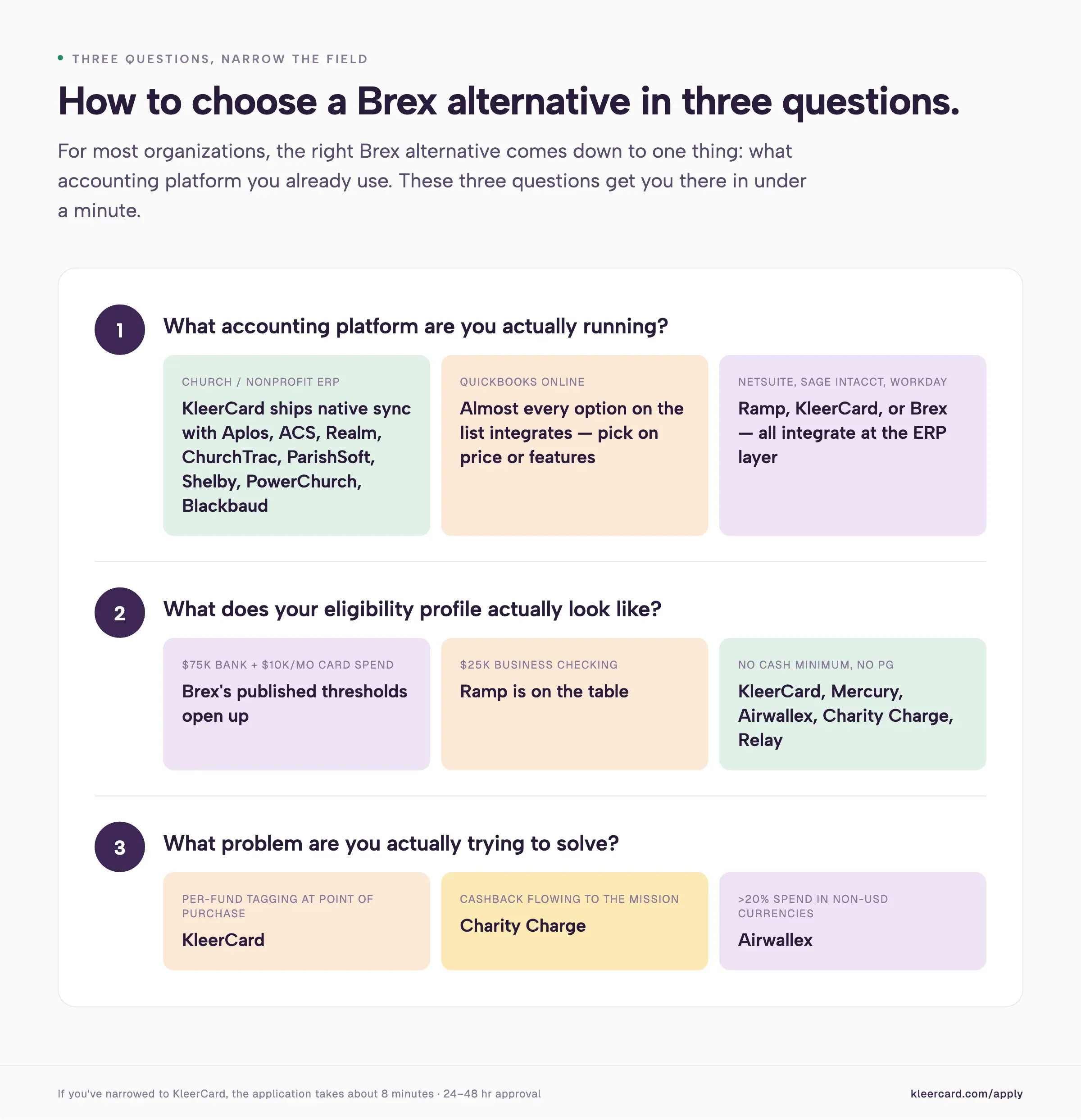

How to choose

For most organizations, the right Brex alternative comes down to one question: what's your accounting platform?

If your fund accounting runs on a church-specific platform (Aplos, ACS, Shelby, ParishSoft, Realm, ChurchTrac, PowerChurch, Blackbaud), the integration question narrows the field. KleerCard is the only platform on this list that integrates natively with all of them.

If cashback is a board-level priority and your books live in QuickBooks Online, Charity Charge is worth a closer look. If more than 20% of your annual spend is non-USD, Airwallex is the answer. If you're venture-backed and running NetSuite or Sage Intacct with stable monthly cash flow, Ramp is a strong option, and so is Brex.

For most churches, K-12 schools, and small-to-mid 501(c)(3) nonprofits, the right card is the one that integrates with the software you already use. If that's KleerCard, you can open an account here or see our pricing. If it's something else on this list, I hope this guide has been useful in helping you figure that out.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)