%202.svg)

In-kind donations are non-cash gifts of goods or services. See how nonprofits value, record, and report them, and what the IRS and GAAP require of you.

An in-kind donation is a non-cash gift of goods or services your nonprofit would otherwise have to buy. Donated equipment, supplies, professional services, and the use of space all count. U.S. accounting rules call these contributed nonfinancial assets. The IRS calls them noncash contributions, and both names point to the same kind of gift.

These gifts are generous, and they carry a little more work than a check. You value the gift, record it, thank the donor correctly, and sometimes report it. The rules differ from cash in a few places that catch people out.

I co-founded KleerCard after two decades in nonprofit finance, and I keep the books for my own church as its treasurer. So I have handled the bookkeeping side of donated goods and services, and the donor side too. Here is how the whole thing works, from the gift arriving to the line on your Form 990.

An in-kind donation is any non-cash contribution to your organization. Someone gives goods or services instead of money, and you put them to work.

The value of the gift is what you would pay for the same thing on the open market. A donated laptop is worth its retail price. A donated week of legal work is worth the attorney's normal fee.

Two terms describe these gifts. Accountants follow U.S. GAAP and call them contributed nonfinancial assets. The IRS uses noncash contributions on its forms. Same gift, two labels.

For a lean nonprofit, an in-kind gift changes the budget in a real way. A donor who covers a month of food for your pantry frees up the money you set aside for food. I work with a lot of small churches and startup nonprofits, and that kind of swing matters when every dollar is already spoken for.

In-kind gifts arrive in a few common forms. Most of what you receive will land in one of these categories.

Donated securities are a special case. You value them at their quoted market price on the day of the gift. You also treat them as financial assets rather than as goods or services, which changes how a couple of the rules below apply to them.

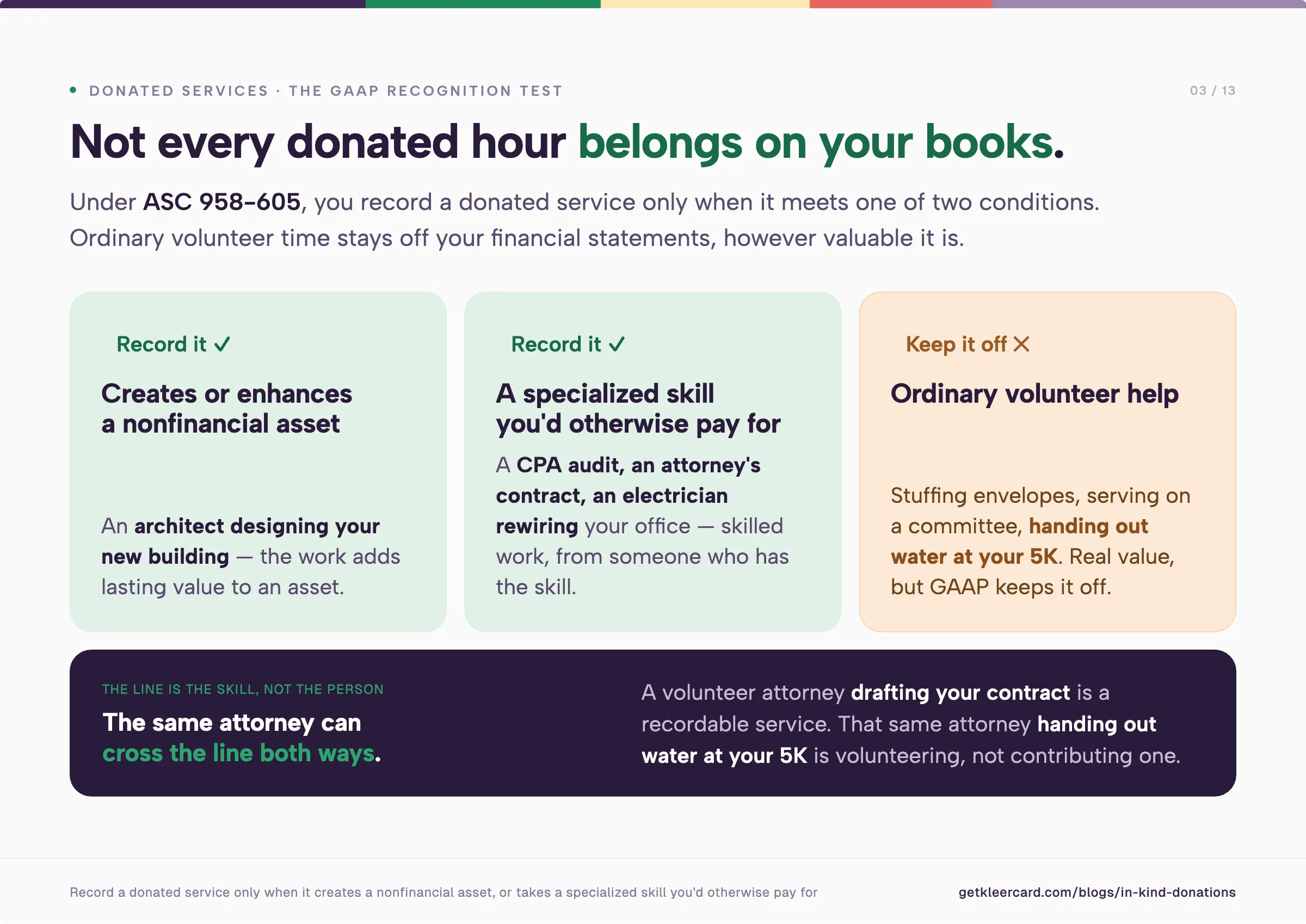

Donated services are the trickiest category, because not every donated hour belongs on your books.

Under ASC 958-605, you record a donated service only when it meets one of two conditions. The first is that the service creates or enhances a nonfinancial asset, like an architect designing your new building. The second is that the service takes a specialized skill, comes from someone who has that skill, and is work you would otherwise pay for.

This table sorts the common cases.

A volunteer attorney drafting your contract meets that second condition. So does a CPA running your audit or an electrician rewiring your office.

Ordinary volunteer time does not. Stuffing envelopes or serving on a committee has real value, but GAAP keeps it off your financial statements. The same attorney handing out water at your 5K is volunteering, not contributing a recordable service.

Every recorded gift needs a fair value, and the right method depends on what you received.

Treat a donor's own estimate with some caution, since owners tend to value their items generously. A brand-new donated tablet is worth its list price, whatever the box says it cost.

Write down where each number came from. An auditor who asks how you valued a gift gets the answer from a saved comp or a rate sheet in seconds.

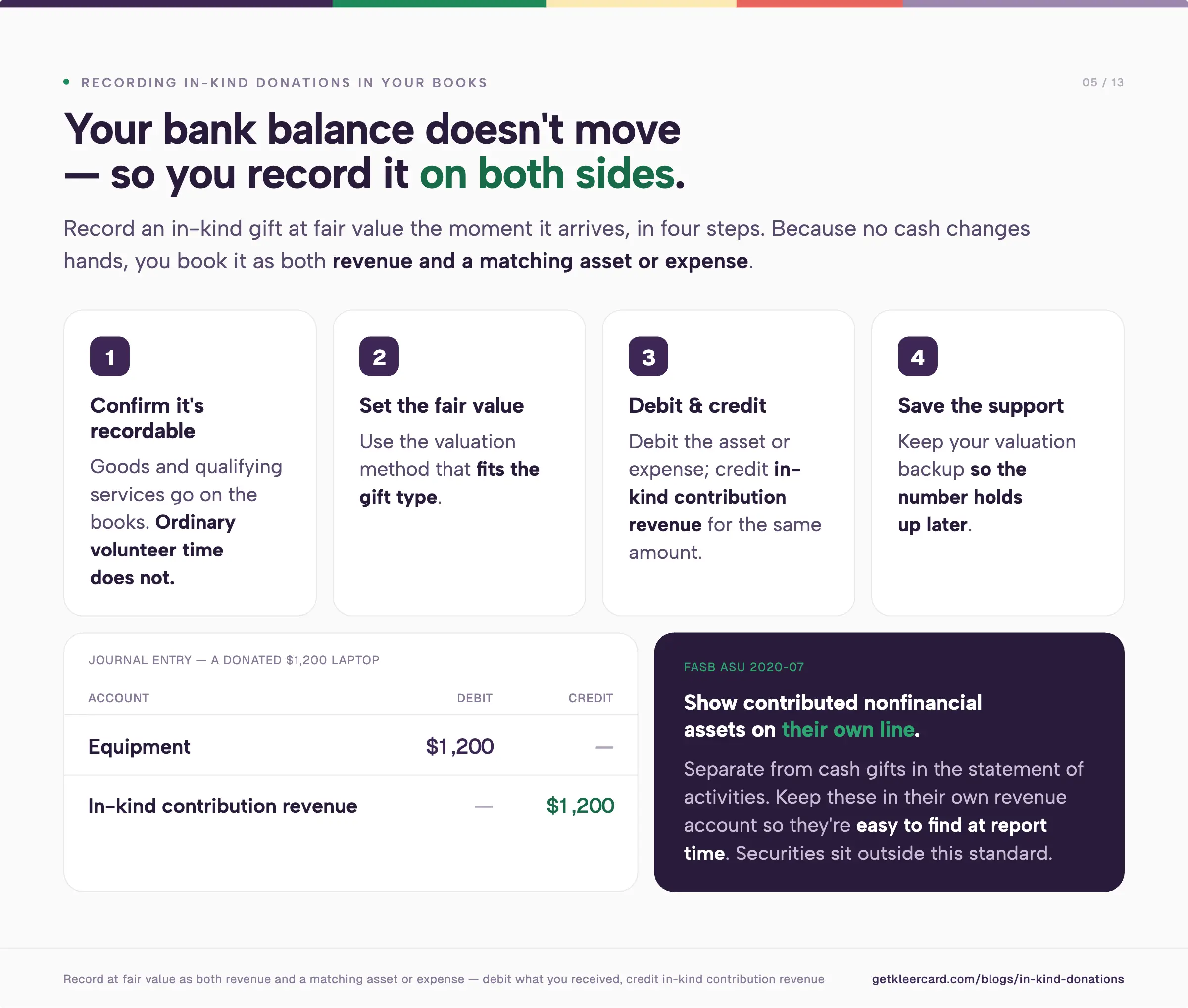

Recording an in-kind gift is straightforward once you see what it does to your books. You record it at fair value the moment it arrives, in four steps.

Your bank balance does not move, so you record the gift as both revenue and a matching asset or expense. A donated $1,200 laptop looks like this.

Keep these gifts in their own revenue account so they are easy to find at report time. If you want a fuller picture of how the pieces fit, our guide to how nonprofit accounting works walks through the rest of the setup.

FASB ASU 2020-07 tells nonprofits to show contributed nonfinancial assets on their own line in the statement of activities, separate from cash gifts. For each category of in-kind gift, the disclosures cover:

The standard changed where these gifts appear and what you disclose, not how you value or recognize them. It applies to fiscal years beginning after June 15, 2021. Securities sit outside its scope, since they are financial assets rather than nonfinancial ones.

Some gifts arrive with strings attached. A donor might give equipment for one program and nothing else. You track that gift to its purpose, the same way you would handle restricted funds on the cash side.

The same gift can end up in different places on your audited financials and your tax return. The split surprises a lot of organizations, so here it is side by side.

The lines below walk through each piece in order.

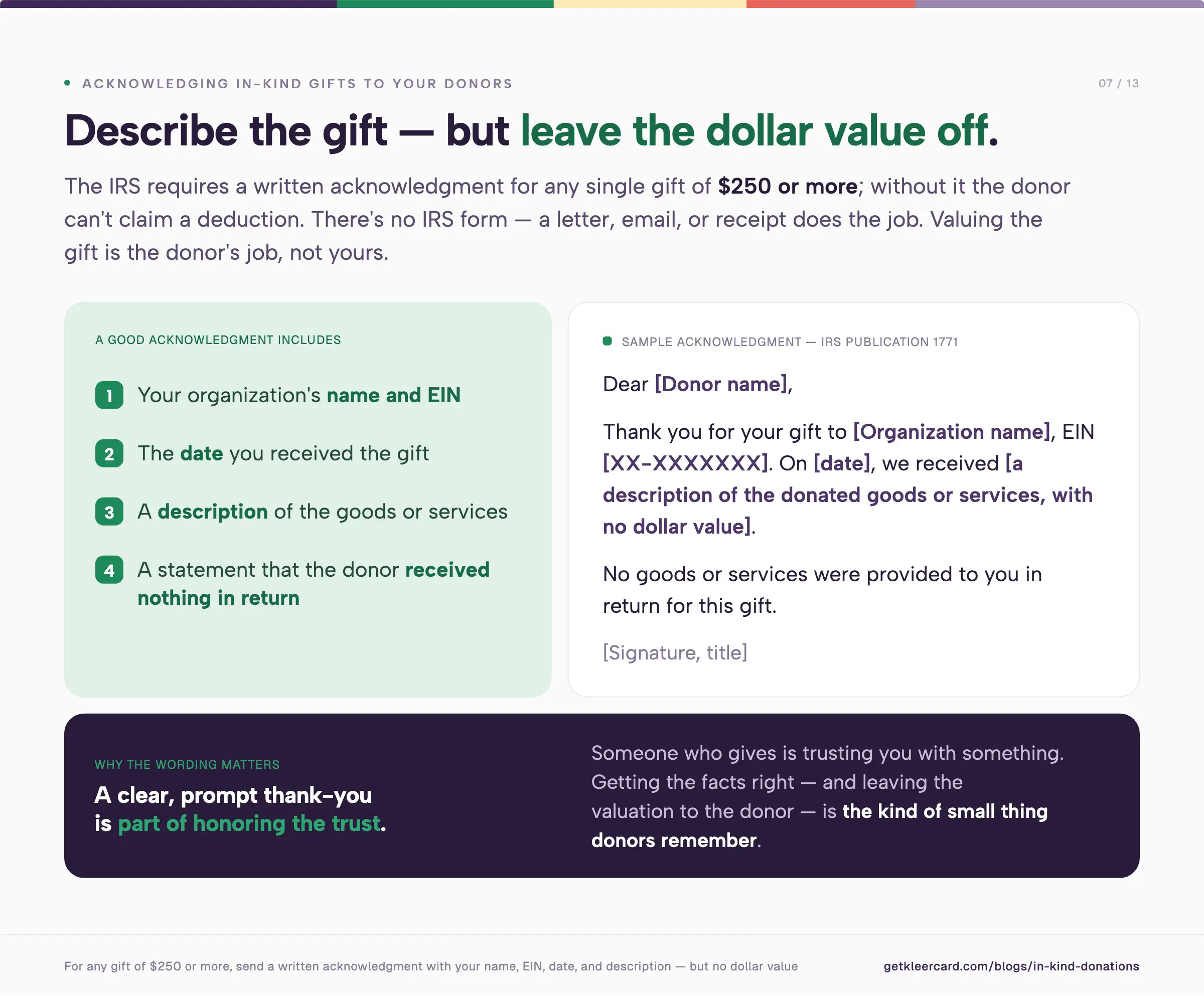

Your donors count on you for one thing at tax time: a proper acknowledgment. Without it, they cannot claim their deduction.

The IRS requires a written acknowledgment for any single gift of $250 or more. For in-kind gifts, your acknowledgment describes what you received but does not state a dollar value. Valuing the gift is the donor's job, not yours.

A good acknowledgment includes:

There is no IRS form for this. A letter, an email, or a receipt does the job, and Publication 1771 lays out the details. A short version reads like this.

Dear [Donor name],

Thank you for your gift to [Organization name], EIN [XX-XXXXXXX]. On [date], we received [a description of the donated goods or services, with no dollar value].

No goods or services were provided to you in return for this gift.

[Signature, title]

I take this part seriously, and not only because the IRS does. Someone who gives to a nonprofit is trusting you with something. A clear, prompt thank-you that gets the facts right is part of honoring that trust, and it is the kind of small thing donors remember.

Larger noncash gifts bring extra paperwork, and most of it sits with the donor. Knowing the split keeps you from doing the donor's job or skipping your own.

A donor files Form 8283 when their total noncash deductions for the year pass $500. For a single item or group of similar items worth more than $5,000, the donor also gets a qualified appraisal and completes Section B.

On those Section B gifts, you sign as the recipient. Your signature confirms you received the item. It does not mean you agree with the donor's valuation, and you are never the appraiser for a gift you receive.

Publicly traded securities are the exception. A donor reports them in Section A, with no appraisal required and no signature from you, even when the gift is worth more than $5,000.

Some in-kind gifts show up on your annual return, and some do not. The line between them surprises a lot of organizations.

You report donated goods as noncash contributions on Form 990, Part VIII, line 1g. Donated services and the donated use of facilities stay off the Form 990 revenue statement, even when your audited financials include them under GAAP.

You file Schedule M when your total noncash contributions for the year top $25,000. You also file it whenever you receive certain special gifts, like art or qualified conservation property, regardless of the amount. Schedule M breaks your gifts down by type, counts them, and asks how you set their value.

Schedule M also asks, on line 31, whether your organization has a gift acceptance policy. That question is a good reason to write one before you need it.

The hardest moment with in-kind gifts is the one you cannot use. The freezer that does not fit. The expired food. The equipment that costs more to haul away than it is worth.

A gift acceptance policy saves you from that moment. It sets out what your organization will accept and on what terms, before anything shows up at your door.

Before you take a large gift, your policy should help you answer a few practical questions:

A written policy also lets your team decline a gift gracefully. You point to the rule, not to the donor, and nobody has to feel ungrateful in the moment.

Publishing your policy tells supporters what would help most. A clear wish list turns vague goodwill into the gifts you need.

A handful of slip-ups show up again and again. None of them is hard to avoid once you know where to look.

Once your books and policy are in order, you can ask for in-kind gifts with confidence. A few habits can help make the asks easier.

Start with a specific wish list instead of a general appeal. "Ten cases of canned vegetables" gets a better response than "food," because it tells a donor exactly how to help.

Look first at supporters who already work for companies with giving or volunteer programs. Then reach out to local businesses whose work lines up with your mission, and offer them recognition in return.

Run every offer past your gift acceptance policy before you say yes. The goal is gifts you can use, not a storage room full of good intentions.

In most cases yes, for the donor, as long as you provide a written acknowledgment. The donor claims the deduction based on the gift's fair value, and any single gift of $250 or more needs that acknowledgment from you. You describe the gift, and the donor assigns the value. The IRS covers the donor's side in Topic 506.

Generally no. Ordinary volunteer time does not go on your books under GAAP. The exception is a service that takes a specialized skill you would otherwise pay for. Donated legal or accounting work counts, and you record it at fair value.

Record it at fair value as both revenue and a matching asset or expense, with no change to cash. You debit the asset or expense and credit in-kind contribution revenue for the same amount. Keep these gifts in their own revenue account so they are easy to report.

Your organization's name and EIN, the date, a description of the gift, and a statement of anything given in return. Leave the dollar value off, since valuing the gift is the donor's responsibility. No special IRS form is required, so a letter or an email works.

Donated goods are reported on Form 990, Part VIII, line 1g, as noncash contributions. Donated services and the use of facilities are left off that statement. You file Schedule M when total noncash contributions pass $25,000 for the year.

An in-kind donation is goods or services instead of money, so you value it and record it differently. You acknowledge it without stating a dollar value, and only some in-kind gifts reach your Form 990. Cash gifts are simpler to value and report.

In-kind gifts are worth the extra steps, and the steps are manageable once you set the routine. You value the gift, record it at fair value on its own line, thank the donor without a number, and report it past the thresholds.

After two decades doing this work, I will take a simple process I run every month over a perfect one I attempt once a year. Consistency is what keeps your books audit-ready and your donors thanked on time.

In-kind gifts are only one side of nonprofit finance. The cash you spend needs the same clean records and controls. We built KleerCard for nonprofits, churches, and schools. If tidy card and expense records are the piece you are still working on, that is the part we handle. If it is not your need today, the recording habits above will carry you on their own.

Speak to a member of our team and we can have you up and running in minutes, not weeks.