%202.svg)

Picture this: your church receives a $25,000 gift for the new youth building. Six months later, a cash crunch hits, and someone moves a portion of those funds to cover payroll. Nobody flags it. Nobody tells the donor. The books get reconciled at year-end, and suddenly your auditor is asking hard questions.

This scenario plays out more often than most church leaders realize. And it is not always a result of bad intentions. It is usually the result of no system. KleerCard offers simple expense tracking solutions for churches and nonprofits, including the ability to create cards dedicated for specific types of expenses, a feature that is especially useful for ministries.

Restricted fund tracking is one of the most consequential financial responsibilities a church or nonprofit carries. When a donor designates a gift for a specific purpose, you are legally obligated to honor that intent. Document it. Report on it. Spend it only as directed. Fail any of those steps and the consequences range from damaged donor relationships to IRS penalties to loss of tax-exempt status.

This guide walks you through exactly how to do it right, from setting up your chart of accounts to closing your books faster every month.

What Are Restricted Funds?

Before building a tracking system, it helps to be clear on what you are actually tracking.

A restricted fund is a type of money that a nonprofit receives from donors or grantors, limited to being utilized in certain ways. The donors or grantors spell out the purpose, time frame, or conditions under which the money must be spent.

This is the opposite of unrestricted funds, which your leadership can direct toward any legitimate operating expense: staff salaries, utilities, office costs, whatever the organization needs.

The Three Types of Restricted Funds

Not all restrictions work the same way. Knowing the difference matters for how you track and report each type.

Temporarily Restricted Funds are the most common type churches encounter day to day. These are designated for a specific purpose or time period. Once those conditions are met, the funds are released for general use. An example would be a grant to fund a summer youth program in 2026. Building campaigns, short-term disaster relief gifts, and program-specific grants all fall here.

Permanently Restricted Funds are intended to be held indefinitely, with only the earnings available to spend. The principal balance is intended to be maintained in perpetuity, such as with an endowment. The organization can typically use the earnings, but not the principal. Memorial funds established in someone's honor are a familiar example in a church context.

Board-Designated Funds are technically unrestricted by the donor, but your leadership has set them aside internally for a specific purpose. Because the board created the limitation, the board can also lift it. This makes them considerably more flexible than donor-imposed restrictions.

One terminology note worth keeping in mind: for audit purposes, temporarily and permanently restricted funds are combined into one category called "with donor restrictions." For internal tracking and decision-making, it is often more useful to track them separately.

Understanding these distinctions is the foundation of solid church fund accounting. Get the categories right and the rest of the system follows much more naturally.

Why Getting This Wrong Is So Costly

Some accounting errors are recoverable with minimal damage. Mismanaging restricted funds is not one of them. The fallout tends to be serious across three fronts.

Donor Trust

Donors give with a purpose. If they learn that their gift was not used as they intended, say, a scholarship gift that ended up covering payroll, they are far less likely to give again. Improper allocation can lead to a damaged reputation within your community.

That damage compounds quietly. One unhappy major donor influences others. Foundations conduct due diligence before renewing grants. A pattern of mismanaged funds can cut off future giving long before leadership understands why.

Restricted fund tracking and church financial transparency go hand in hand. Donors who can see exactly how their gifts are being used are the ones who give again, give more, and bring others along with them.

Legal Liability

Churches face serious risks if they fail to honor donor restrictions: legal liability where donors may sue to reclaim their contributions, loss of trust where mismanagement damages the church's reputation and donor relationships, and tax compliance concerns where returning contributions can have implications for both the donor and the church.

Courts have sided with donors in cases involving diverted restricted gifts. One Maine ruling found that unreasonable delays in fulfilling the purpose of a restricted donation could be grounds for a full refund to the donor.

IRS Penalties

If the IRS discovers misuse, your organization could face penalties such as fines or even the loss of your tax-exempt status. For a church or nonprofit whose funding model depends on donors making tax-deductible contributions, losing 501(c)(3) status is an existential threat.

Poor tracking often comes to light during an audit and may lead to reclassifications, management letter comments, repeat findings, or in severe cases, a modified audit opinion if restricted net assets are materially misstated. Any of those outcomes erodes credibility with grantors and major donors who rely on audits to evaluate whether your organization is worth funding.

The good news is that all of this is preventable. It starts with how your accounting system is structured.

Setting Up Your Chart of Accounts for Fund Accounting

Your chart of accounts is the foundation everything else depends on. Every report, audit, and donor communication flows from how well this is built.

Every nonprofit should customize its chart of accounts to fulfill its unique reporting needs, and to account for restricted and unrestricted funds. Within your chart of accounts, create separate account categories for restricted and unrestricted funds under a broader net assets category. Developing individual accounts for each restricted fund project allows you to track revenue and expenses associated with those specific funds easily.

Your three main net asset categories will be funds without donor restrictions (your general operating fund and any board-designated reserves), funds with temporary donor restrictions (building funds, program grants, capital campaigns), and funds with permanent donor restrictions (endowments and memorial funds). Each restricted fund needs its own line so deposits and expenditures are coded correctly from day one.

Do not rely on spreadsheet notes or memory to sort things out later. That approach works until it does not, and when it breaks, it usually breaks during an audit.

The Two-Column Reporting Format

Once your chart of accounts is set up, your financial statements should reflect it with a two-column format: one column for funds with donor restrictions, one for funds without.

The most effective practice is to display grants and contributions with donor restrictions in a separate column. This two-column approach works for both the income statement and the balance sheet. When the time or purpose restriction has been met, a journal entry is made to transfer funds from the With Donor Restrictions column to the Without Donor Restrictions column using the "release from restrictions" line item.

This is not just best practice. It is what FASB ASC 958 requires nonprofits to present. The "Without Donor Restrictions" column is especially valuable for leadership because it shows what is genuinely available for operations, without the distortion that large restricted gifts can create.

A note on multi-year grants specifically. Accounting rules require a nonprofit to record all the income of a multi-year grant in the year it is received. If an organization's income statement shows just total income and expenses without separating the restricted dollars, inflated surpluses can appear in year one of the grant period, along with possible artificial deficits in the remaining years. Without the two-column format, leadership may genuinely believe the organization has more flexibility than it does, which leads to exactly the kind of spending mistake that ends in an audit conversation.

How to Track Restricted Funds: A Step-by-Step Process

With the right structure in place, here is how to execute tracking cleanly from the moment a gift arrives to the moment a restriction is released.

Step 1: Document Donor Intent at the Point of Gift

Most tracking problems do not start in the accounting system. They start at the front door, when a gift arrives without anyone recording what the donor intended.

When in doubt, document. Even if a donor's restriction is made verbally, follow up in writing to confirm intent. This creates a paper trail that protects both you and the donor relationship.

Restrictions can arrive through more channels than a formal letter. Donors may write their intent in the memo line of a check, a digital note on an online giving platform or payment app, or an accompanying letter or email. Pay careful attention to what is written in all these areas and ensure you record and track restrictions accurately.

Train everyone who handles donations to flag any language that might signal a restriction before the gift is processed. That includes administrative staff, volunteers, and anyone managing your giving platform.

Step 2: Assign Restriction Codes Immediately

Once a gift is identified as restricted, it needs a code before it enters your general ledger. Not at month-end. Not when someone gets around to it.

Assign program, project, or restriction codes from the start to avoid later confusion and ensure that expenses are linked to their correct funding source.

Correcting miscoded entries after the fact is time-consuming and error-prone. It is also exactly the kind of issue that shows up in audit findings and requires an explanation.

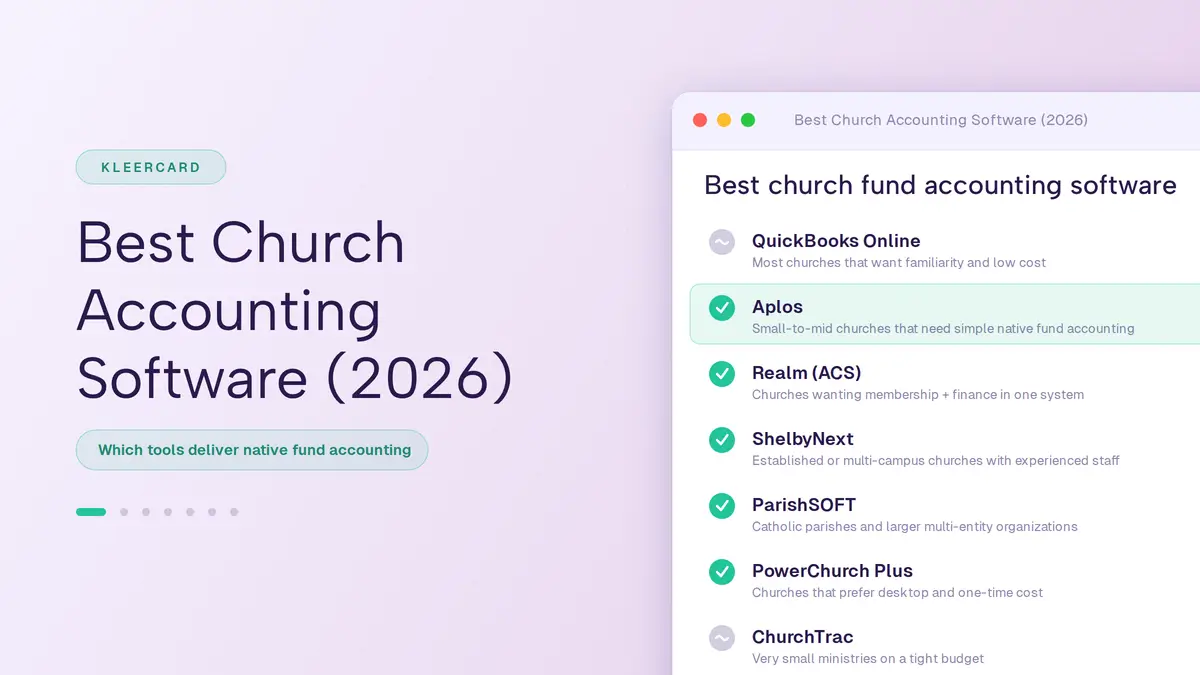

Step 3: Use Fund Accounting Software Built for Nonprofits

Standard business accounting software does not think the way nonprofit fund accounting requires. General-purpose platforms can be customized for nonprofit use, but purpose-built fund accounting tools offer structures that align naturally with how restricted and unrestricted giving actually works in a ministry context.

If you are evaluating your options, the complete guide to church accounting software covers what features to look for and how to choose the right system for your organization's size and complexity.

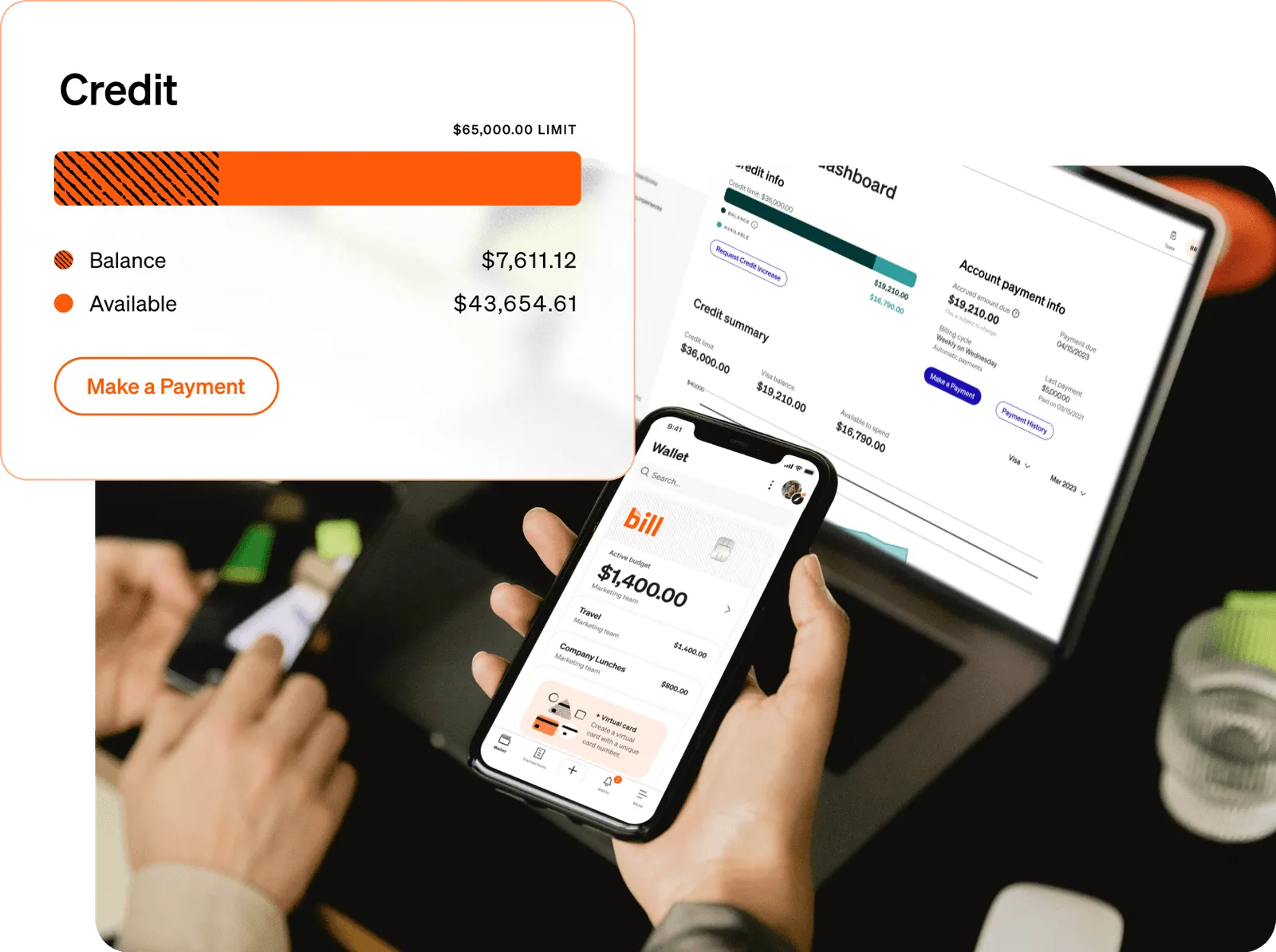

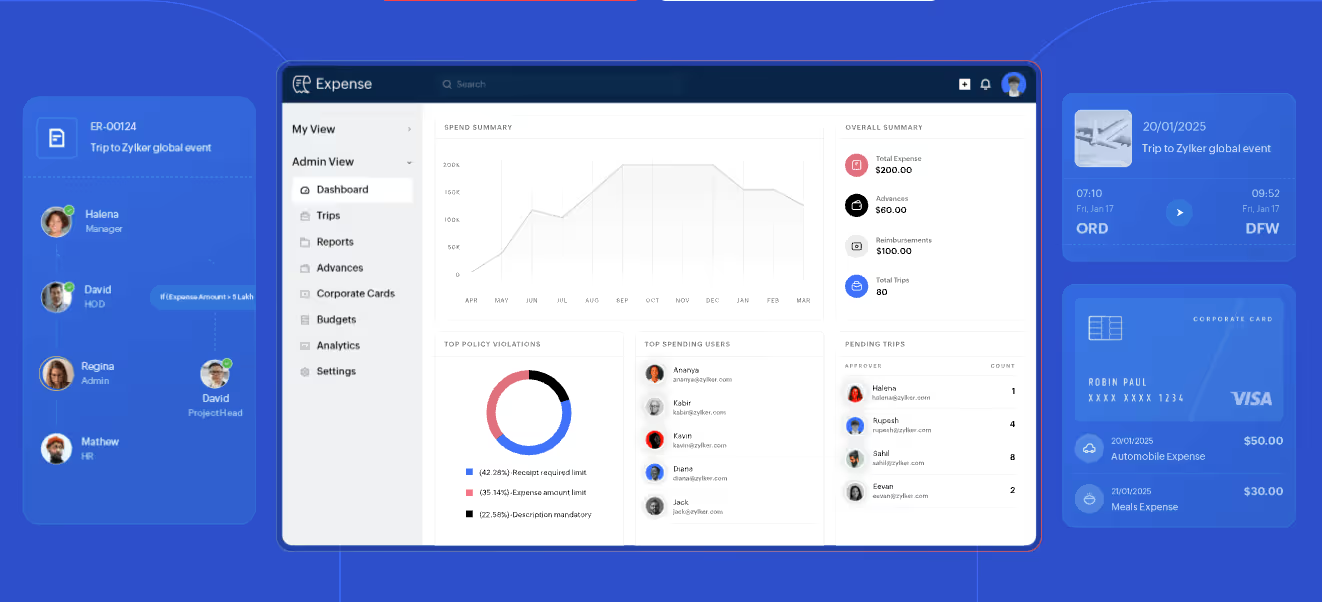

KleerCard was built specifically for churches and nonprofits facing this challenge. Its AI-driven fund classification categorizes transactions automatically as they happen, so your restricted balances stay accurate without manual coding. Instead of spending hours at month-end reconciling which expenses came from which fund, your team sees real-time balances for every restricted fund from a single dashboard. Faster closes, cleaner audits, more time for mission.

Step 4: Track Revenue and Expenses by Program

Restricted fund tracking is not just about where money came in. It means tracing every dollar through to its intended use.

Track revenue and expenses by program using a dedicated function in your accounting software. You also want to track activity by funder separately. With that setup, you can run reports showing your revenue and expenses by both program and funding source, which tells you where you have funds remaining to spend and where you need to focus additional fundraising efforts.

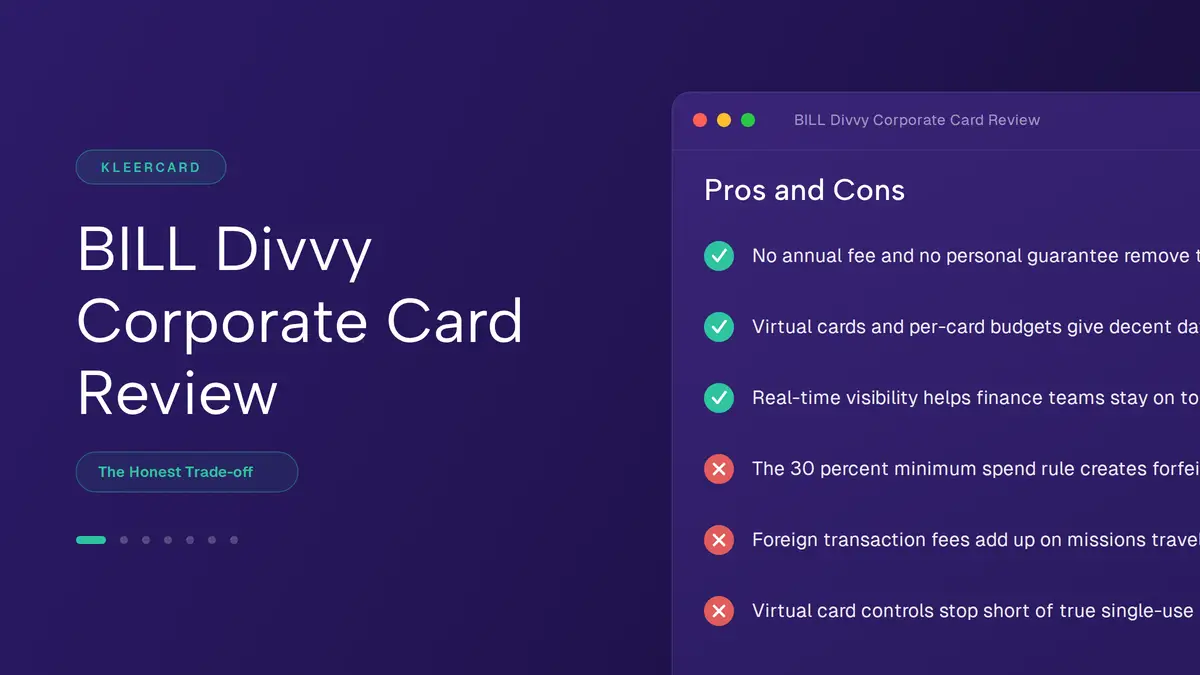

KleerCard adds another layer here through card-level controls. You can assign spending limits to specific cards tied to specific funds, so a staff member using the youth ministry card cannot accidentally draw from the building campaign fund. The separation is enforced automatically, not just reconciled after the fact. For more on how spending controls protect your organization, see the guide on church spending controls and financial oversight.

Step 5: Reconcile Restricted Balances Monthly

Year-end reconciliation is too late. By December, months of miscoded transactions mean a painful scramble to reclassify entries, explain discrepancies to auditors, and in some cases, call donors to address shortfalls.

Review and reconcile restricted balances regularly. Do not wait until year-end; ensure that spending is properly tracked monthly or quarterly. Do not just reconcile balances, reconcile donor intent.

That second sentence is the one most organizations miss. You are not just making sure numbers add up. You are verifying that the way those numbers were generated actually honors what each donor asked for.

Step 6: Release Funds from Restrictions Properly

When the conditions of a restricted gift are met, a formal accounting step is required before you move on.

When the time or purpose restriction has been met, a journal entry is made to transfer funds from the With Donor Restrictions column to the Without Donor Restrictions column using the "release from restrictions" line item.

Document this release clearly, tie it to evidence that the restriction was fulfilled (project completion, end of grant period, etc.), and have it reviewed before posting. This journal entry is what keeps your Statement of Activities accurate and audit-ready.

Common Mistakes and How to Avoid Them

Knowing what goes wrong is just as valuable as knowing the right steps. The most common errors are usually not the result of dishonesty. They are the result of unclear policies, manual processes, and systems that were never set up to handle fund accounting correctly.

The most frequent mistake is commingling restricted and unrestricted funds. Keep restricted funds in separate general ledger lines, or a separate bank account for larger funds. The second most common is relying on verbal donor agreements. Always follow up with written confirmation, even a brief email recap is enough to create a record. Third, coding donations at month-end instead of at receipt is a process that consistently creates downstream errors. Assign restriction codes at the point of entry, before the gift hits the ledger. And finally, assuming small organizations are exempt from FASB rules is a dangerous misconception. GAAP and FASB requirements are not dependent on organization size. Even small nonprofits and churches are expected to use the current methodology for tracking restricted funds.

The Cash Crunch Problem Deserves Extra Attention

Using restricted funds to cover operating shortfalls is the most common serious error, and the one with the most severe consequences.

Once money is restricted, that restriction is permanent. The funds cannot be redirected to other purposes, even if the budget picture becomes bleak. It is a difficult situation to face unpaid bills or payroll with nothing in the operating account but $50,000 sitting in a Scholarship Fund. The IRS is serious about restricted funds. Improper use can result in severe penalties, or even loss of exempt status. Boards can be sued by donors for misuse of such funds.

If a situation is serious enough that you are considering repurposing restricted funds, the only compliant path is to obtain written permission from the original donor to release or modify the restriction. Act first and explain later is never the right sequence.

Communicating with Donors About Their Restricted Gifts

Accurate tracking behind the scenes is only part of the job. Keeping donors informed is what transforms good bookkeeping into genuine stewardship, and genuine stewardship is what keeps donors giving.

Provide periodic reports to donors to assure them you are using their contributions responsibly. Tell them how you have spent their funds so far and include the remaining balance. Communicate any changes in fund use and how you plan to handle them. Emphasize the impact donors' contributions have on your cause.

These updates do not need to be elaborate. A quarterly email showing building campaign progress or an annual letter summarizing grant activity builds the kind of trust that leads to renewed and increased giving.

97% of donors say creating a positive impact is their main reason for giving, so adding impact information can satisfy donors and encourage them to contribute again.

With KleerCard's reporting tools, generating a fund-specific summary for a donor takes minutes. Pull activity by fund, show beginning and ending balances, attach receipts or expense documentation, all from one place. What used to take hours becomes a routine part of donor relations.

Watch Your Solicitation Language

One of the most overlooked sources of restricted fund headaches is the language used to ask for gifts in the first place.

When your church runs a campaign for a specific need, any donation received in response may be considered restricted, even if you did not intend it that way. This is a problem that originates in your bulletins and giving pages, not your accounting system.

Appeal language should make it clear when your ministry is seeking flexible support and when you are asking for a restricted gift. Use pledge forms and acknowledgements that clearly indicate unrestricted versus restricted funds, and keep your website, bulletins, and solicitation materials consistent with that message.

The practical fix is straightforward. "Give to our new sanctuary" creates a restriction. "Give to support our ministry's needs, including our new sanctuary" preserves flexibility. Review every donation envelope, giving page, and campaign communication with a finance-aware eye before it goes out.

Frequently Asked Questions

What is the difference between restricted and designated funds in a church?

Restricted funds carry donor-imposed limitations that are legally binding. Designated funds are typically set aside internally by the board and can be redirected by board decision. The key distinction is who set the limitation and whether the donor has an expectation about how the funds will be used.

Can we use restricted funds to cover operating expenses if we are short on cash?

No, and this matters more than most people realize. Restricted funds cannot be moved to cover general operations unless the restriction is lifted in writing. If you genuinely need to repurpose restricted funds, get written permission from the original donor first. There is no shortcut.

Do small churches have to follow the same fund accounting rules as large nonprofits?

Yes. Size does not create an exemption. GAAP and FASB requirements apply to organizations of every scale, which means even a small congregation tracking a single restricted gift needs to handle it correctly.

Are restricted donations tax-deductible for donors?

It depends on how the restriction is structured. In order for a donor to claim a tax deduction, he or she must relinquish control and give your church the ability to use the donation at its discretion. If a donor restricts a gift so narrowly that the organization cannot exercise real discretion, the contribution may not qualify as tax-deductible. When in doubt, consult a nonprofit accountant or church law attorney.

What happens if we accidentally misuse restricted funds?

Act quickly. If misused, the nonprofit may need to reimburse the restricted fund from unrestricted resources. This could also result in donor fallout, negative audit findings, or IRS penalties if it affects your Form 990 reporting. Contact the donor, correct the books, and bring in a nonprofit accountant as soon as possible.

How do we handle excess restricted funds when a project is completed?

Contact the donor and ask for permission to reallocate. If you obtain the donor's permission, be sure to reclassify the funds in your accounting system and report the release of net assets from restrictions in your Statement of Activities.

Is restricted fund tracking required on Form 990?

Yes. Form 990 requires nonprofits to differentiate restricted and unrestricted revenue in their financial statements. Improper categorization can trigger audit flags and public scrutiny, which is why accurate classification from the start matters so much.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)