%202.svg)

A single undocumented purchase can do more than throw off a ledger. It can weaken trust, blur accountability, and expose a church to avoidable financial risk.

Strong spending controls are not about suspicion. They are about protecting the people, donations, and mission that depend on sound oversight in church finances. Additionally, part of building strong church finances is choosing the right church accounting software.

Why Churches Need Clear Spending Controls

Every church handles money under a public trust. Members give with the expectation that offerings, designated gifts, and restricted funds will be used carefully and in line with donor intent.

That is why internal controls matter so much in a ministry setting. They protect financial integrity while also protecting pastors, staff, volunteers, and board members from preventable mistakes and false accusations.

Weak oversight often starts small. A missing receipt, a verbal approval, or a reimbursement with no supporting documentation may seem minor at first.

Over time, those gaps create room for duplicate payments, unclear authority, coding errors, and fraud risk. Good fraud prevention starts long before a crisis by building checks and balances into daily financial administration.

Clear controls also support financial transparency. When a church can explain who approved spending, what records support the payment, and how the expense fits the church budget, confidence grows.

What Spending Controls Mean in a Church Setting

In a church setting, spending controls are the rules and review steps that govern how money is requested, approved, paid, recorded, and checked later. That includes written policies, purchase authorization, expense approvals, documentation standards, and monthly review.

These controls should apply to every way money leaves the church treasury. That means cash, checks, ACH payments, online payments, church credit cards, and expense reimbursement requests.

A healthy system also covers the full path of a transaction. Someone requests the purchase, someone with authority approves it, someone processes payment, and someone else reviews the records.

The Cost of Informal Processes

Informal processes often create the same problems across churches. Common examples include duplicate invoices, undocumented ministry expenses, after-the-fact approvals, and payments made without clear budget ownership.

The reputational cost can be even higher than the accounting cost. If members begin to question how donated cash or other gifts are handled, the church can lose trust that took years to build.

Set the Foundation With Written Financial Policies

A church should not rely on memory, habit, or verbal tradition to manage spending. It needs written policies collected in a usable policy manual.

That manual should define who can spend, who can approve, who can review, and what records are required before money is released. It should also include approved payment methods, spending limits, and escalation rules when purchases fall outside normal activity.

Simple policies are more likely to be followed consistently. If staff and volunteers cannot understand the process quickly, exceptions will multiply.

Written policies also support compliance and legal and regulatory compliance. They create a repeatable system that can be reviewed by the treasurer, finance committee, or board oversight team.

Core Policy Areas to Document

At minimum, churches should document these areas in writing:

- Purchasing rules and purchase authorization steps

- Expense reimbursement requirements

- Cash handling and cash income controls

- The bank deposit process for offerings and other receipts

- Rules for general fund, designated funds, and restricted funds

- Church credit cards and cardholder responsibilities

- Required itemized receipts and other supporting documentation

- Conflict of interest disclosures

- Financial reporting and review procedures

Policies should also explain how ministry expenses are coded and who can move budgeted funds between categories. That matters because weak coding can hide overspending or misuse of restricted funds.

How to Keep Policies Current

A policy manual should be reviewed at least once a year. Churches change staff, software, payment tools, and ministry structure, and procedures need to keep pace.

The review should involve finance leaders, the treasurer, and board members with oversight responsibility. If the church adds online payments, new card programs, or multiple campuses, the rules should be updated before those changes become routine.

[[cta]]

Build an Approval Process That Matches Risk

Not every expense carries the same level of risk. A weekly supply purchase should not require the same review as a building contract or a technology subscription that renews automatically.

That is why churches need an approval matrix. It sets approval levels based on amount, fund type, purchase category, and whether the expense is routine or unusual.

A good approval workflow separates requesting, approving, paying, and reconciling whenever possible. This structure reduces the chance that one person can control the full transaction cycle without oversight.

Routine expenses should still move efficiently. The goal is not to slow ministry work but to create expense approvals that are clear, documented, and proportional.

Set Spending Limits by Role

Spending limits should match authority and responsibility. Ministry leaders may be allowed to approve small recurring expenses, while pastors, finance staff, or board members handle larger commitments.

For example, a children’s ministry director may approve supplies up to a set amount from an approved budget line. Capital purchases, contracts, or unusual expenses should require higher approval, often from senior leadership or the board.

These role-based limits are especially helpful when staff changes occur. Instead of relying on personal relationships, the church follows a documented structure.

Use Preapproval for Nonroutine Purchases

Nonroutine spending should require preapproval before any commitment is made. That includes equipment purchases, consultant contracts, event deposits, and technology upgrades.

Require quotes, written justification, or both for larger purchases. After-the-fact approvals weaken accountability because the church is no longer deciding whether to spend, only how to explain a decision already made.

Control How Money Leaves the Church

One of the clearest signs of strong oversight is a consistent disbursement process. Churches should standardize payments through checks, ACH payments, or approved card workflows rather than ad hoc methods.

Expenses should never be paid directly from offering cash or other undeposited donations. Donated cash should move through a clear collection process and bank deposit process before it is used for any purpose.

Before payment is released, the church should have an invoice or receipt, proper coding, and evidence of approval. That protects cash flow management and improves financial reporting.

Checks, ACH, and Online Payments

Checks remain useful for some churches, but they need controls. Blank signed checks should never exist, and check stock should be secured.

ACH payments and online payments need equal or stronger safeguards. Dual authorization for larger electronic payments is a smart standard because digital speed can also speed up errors or unauthorized activity.

Bank access should be restricted by role-based access settings. Payment logs should be reviewed regularly so unusual vendors, timing, or amounts are caught early.

Reimbursements and Church Cards

Expense reimbursement should require itemized receipts, the business purpose, the ministry area charged, and timely submission. A reimbursement with no receipt or vague explanation should be rejected or escalated for review.

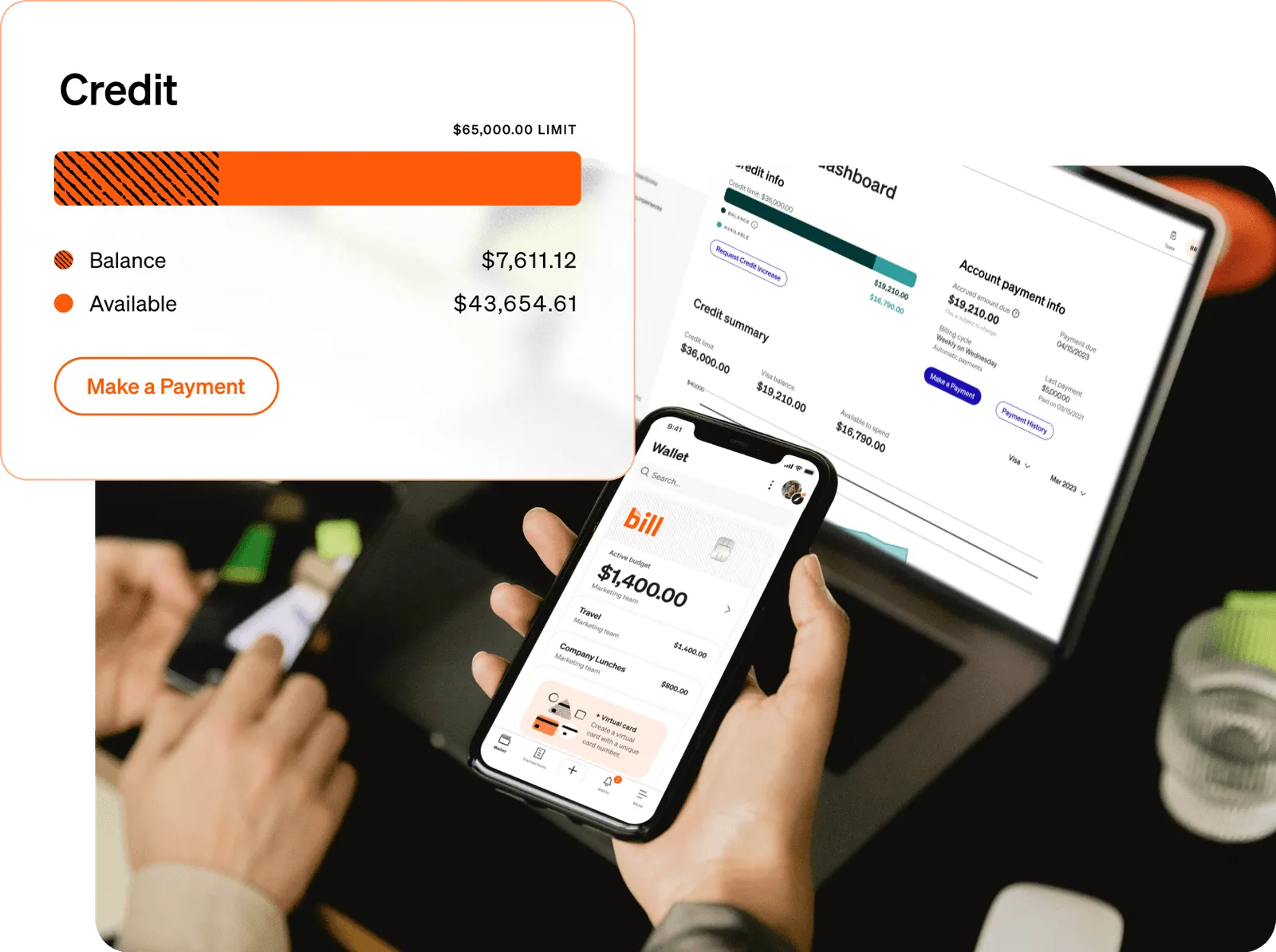

Church credit cards can simplify spending, but they need strict controls. Merchant restrictions, card limits, and monthly review of statements reduce misuse and make exceptions easier to spot.

For churches looking to tighten card and reimbursement processes, tools built for ministry finance teams and spending oversight can help centralize approvals and records.

Teams that rely heavily on volunteers may also benefit from systems designed for managing volunteer purchases with tighter guardrails.

Use Separation of Duties and Independent Review

No single person should request, approve, pay, record, and reconcile the same transaction. Separation of duties is one of the most effective nonprofit controls because it limits both fraud and unintentional error.

Many churches worry they are too small to separate tasks. Even with limited staff, some division of responsibility is usually possible through the treasurer, elders, deacons, finance committee, or trained volunteers.

Independent review adds another layer of protection. When someone not involved in the original transaction reviews reports and reconciliations, issues are more likely to be caught early.

How to Separate Duties in a Small Church

Small churches can divide work in practical ways:

- Counting teams should rotate and work in pairs

- The person who counts offerings should not post contributions alone

- The person who issues payments should not complete the bank reconciliation

- The pastor should not be the only approver for all expenses

- Finance review should stay independent from counting and deposit preparation

Cash handling deserves special care because cash is harder to trace than digital payments. A clear collection process, documented counts, secure storage, and prompt deposits are essential cash income controls.

Churches with multiple locations face added complexity. A system built for coordinating spending across several campuses can help standardize approvals while preserving local visibility.

What Should Be Reviewed Monthly

A strong monthly review should include:

- Bank reconciliation reports

- Budget-to-actual report results

- Card statements

- Unusual transactions

- Vendor changes

- Exceptions to policy

- Outstanding reimbursements

Document who reviewed the reports and what follow-up was required. That record matters because oversight should be visible, not assumed.

[[cta]]

Tie Spending Controls to the Budget and Fund Rules

A church budget is not just a planning document. It is a control tool that guides spending decisions before money is committed.

When leaders compare proposed purchases to approved budget lines, they create discipline around priorities. This makes variance analysis easier and helps identify policy gaps before they become recurring problems.

Churches also need clear rules for the general fund, designated funds, and restricted funds. These terms are often confused, but they do not mean the same thing.

The general fund supports normal operations. Designated funds are set aside for a purpose identified by the church or donor, while restricted funds carry donor intent that must be honored.

Budget Guardrails That Prevent Overspending

Useful budget guardrails include:

- Line-item spending limits

- Required approval for budget transfers

- Preapproval for unbudgeted purchases

- Review of recurring subscriptions

- Review of contract renewals before automatic rollover

A budget-to-actual report should be reviewed each month, not just at year end. Regular variance analysis helps the church see where spending is drifting and whether controls are being bypassed.

Respect Donor Intent

Restricted gifts should only be used for the purpose for which they were given. If a donor gives toward missions, benevolence, or a building project, that money should not quietly cover payroll or general ministry expenses.

The accounting system should track designated funds and restricted funds clearly. Respecting donor intent is both an ethical duty and a core part of financial transparency.

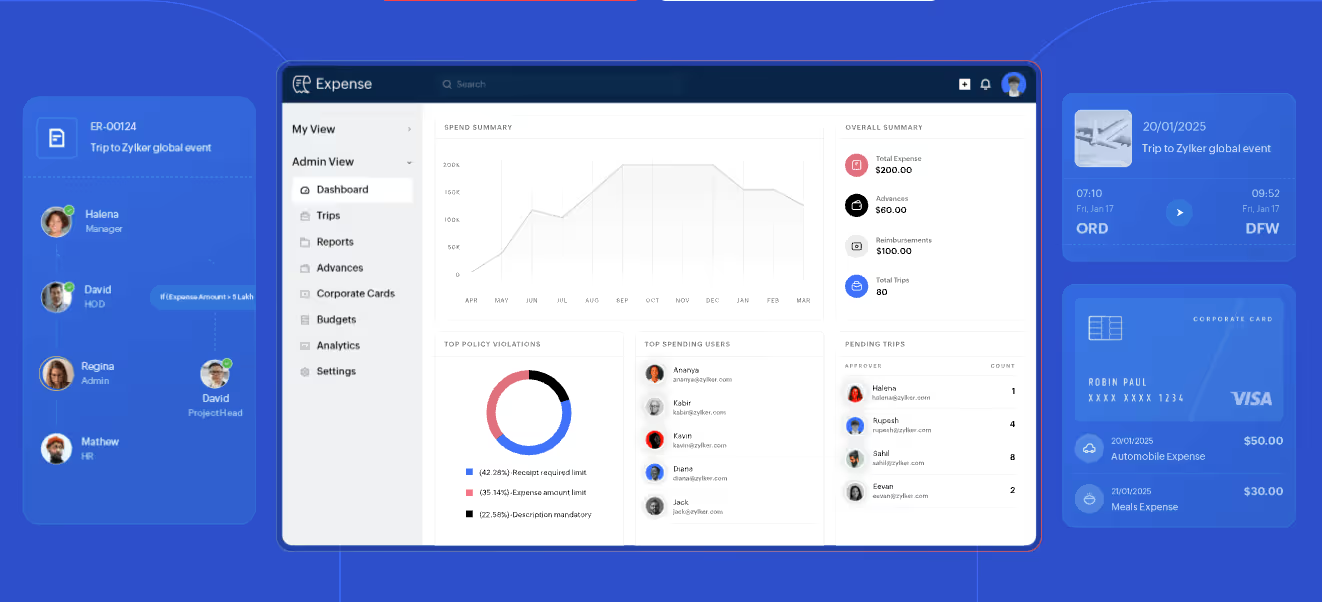

Use Technology Without Losing Oversight

Accounting software can clean up recordkeeping, but software alone does not create accountability. A weak process inside a digital system is still a weak process.

The best tools support approval workflow, document storage, and cleaner financial reporting. They also make it easier to maintain an audit trail for each transaction.

Look for systems that support role-based access, receipt capture, vendor management, and approval routing. Keeping payment history and supporting documentation in one place reduces confusion during review.

Churches exploring modern expense systems may find value in this breakdown of expense management improvements for ministry teams. Some organizations also compare options through resources tailored to ministry outreach and administrative needs.

Helpful System Features

Helpful features include:

- Role-based access

- Approval routing

- Receipt capture

- Audit trail visibility

- Vendor records in one system

- Searchable payment history

- Exportable financial reporting

These features support oversight, but they do not replace review by people with authority. Human review remains central to financial administration.

Common Technology Mistakes

Common mistakes include shared logins, broad admin access, weak permissions, and missing backup records. Convenience should never override approval rules.

Another mistake is assuming that a posted transaction has been properly reviewed. Software can record activity, but it cannot judge whether the purchase was wise, authorized, or aligned with policy.

Common Mistakes Churches Should Avoid

Most control failures are not dramatic. They are routine habits that slowly weaken accountability.

High-risk habits often appear in churches with sincere people and busy schedules. That is why prevention depends on clarity and consistency, not just good intentions.

High-Risk Practices

Watch for these warning signs:

- Single-person control over approvals and payments

- Missing receipts

- Blank checks

- Undocumented reimbursements

- Payments from donated cash before deposit

- No conflict of interest disclosure

- No board oversight of unusual spending

How to Correct Them Quickly

Start with simple fixes:

- Use approval forms

- Require itemized receipts

- Create a payment checklist

- Schedule monthly review meetings

- Train all staff and volunteers on the same process

Staff training matters because inconsistent practice creates exceptions. A control is only effective if people understand how to follow it.

A Simple Rollout Plan for Better Spending Controls

The best rollout plan starts with the highest-risk areas first. Cash handling, reimbursement rules, bank access, and approval thresholds usually deserve immediate attention.

From there, churches can build a stronger system without making daily operations unnecessarily complex. The goal is steady improvement backed by measurable review.

First 30 Days

In the first month, document the current process for spending, approval, payment, and reconciliation. List who has bank access, card access, and authority to approve ministry expenses.

Fix urgent gaps right away. That may include tightening cash handling, stopping payments from undeposited offerings, and requiring receipts for every expense reimbursement.

Next 60 to 90 Days

Finalize written policies and publish the policy manual. Assign reviewers, confirm the approval matrix, and train staff and volunteers on the same rules.

Then begin monthly reporting on approvals, variances, exceptions, and unresolved follow-up items. Over time, this rhythm strengthens accountability, financial integrity, and trust.

FAQ

What Is the 80 20 Rule in Churches?

In church finance discussions, the 80/20 idea usually means a small group often carries most giving or ministry work. It is not a formal spending control.

It does, however, show why churches need broad accountability, careful donor communication, and disciplined budgeting rather than depending too heavily on a small number of people.

What Is the 70/20/10 Rule Money?

The 70/20/10 rule is a personal money framework that divides income into spending, saving, and giving. A church may mention it in teaching, but it is not a control framework for church finances.

Church spending decisions should be based on written policies, expense approvals, fund restrictions, and budget oversight.

Who Controls the Money in a Church?

No single person should control all church money. Good practice uses shared oversight among finance staff, a treasurer or finance committee, senior leadership, and the board.

Approval, payment, reconciliation, and review should be separated whenever possible. That structure creates stronger checks and balances.

What Is the 80% Rule for Churches?

The 80% rule can mean different things depending on the setting, such as budget planning or facility use. It is not a standard internal control rule.

Churches should rely on written financial policies, clear approval thresholds, and consistent review instead of informal rules that vary by context.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)