%202.svg)

The Association of Certified Fraud Examiners estimates the typical organization loses 5% of its revenue to fraud every year. For a nonprofit running on lean budgets and donated dollars, that loss lands harder than the number suggests.

This article is for treasurers, finance directors, executive directors, and board members who want to understand how fraud happens in mission-driven organizations and how to lower the risk without building a corporate bureaucracy.

Nonprofit fraud is the misuse of an organization's money, assets, or financial reporting by someone inside or connected to it. Common forms include embezzlement, skimming cash before it is recorded, fake vendor billing, payroll schemes, expense reimbursement abuse, and misstating the financial records. The IRS treats it as the misuse of charitable assets.

We'll walk through what counts as fraud, what it actually costs, why nonprofits are exposed, the schemes that show up most often, the warning signs worth watching, why audits alone fall short, and the practical controls a small team can put in place.

What Counts as Fraud in a Nonprofit

Nonprofit fraud is the misuse of an organization's money, assets, or financial reporting by someone inside or connected to it. Common forms include embezzlement, skimming cash before it is recorded, fake vendor billing, payroll schemes, expense reimbursement abuse, and misstating the financial records. The IRS treats it as the misuse of charitable assets.

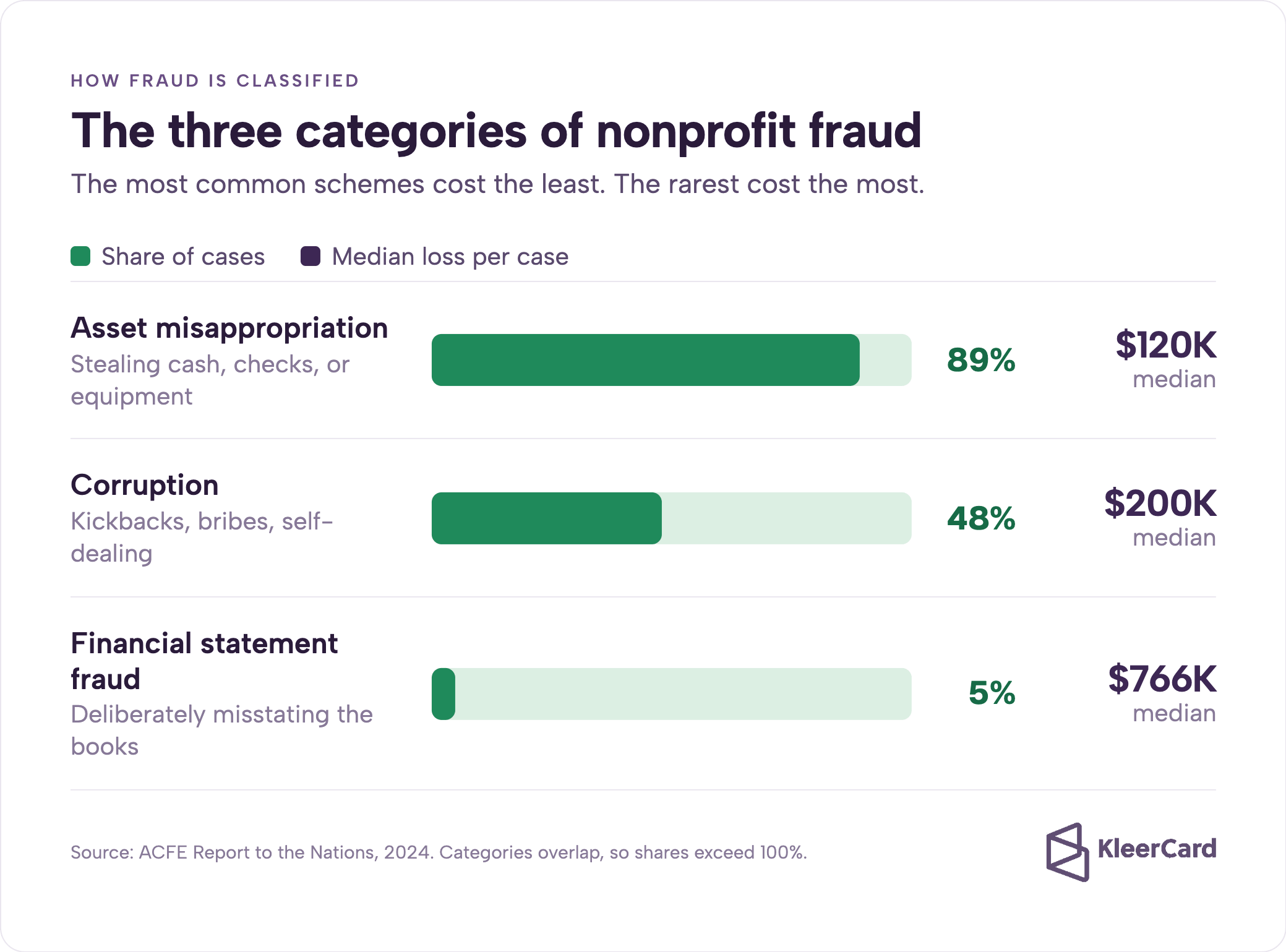

Fraud examiners sort almost every scheme into three buckets:

- Asset misappropriation. Someone steals or misuses cash, checks, inventory, or equipment. This is the most common category by a wide margin.

- Corruption. Someone uses their position for private benefit, through kickbacks, bribes, conflicts of interest, or self-dealing.

- Financial statement fraud. Someone deliberately misstates the books, often to hide one of the first two or to inflate reported impact.

Many cases mix more than one category, and a single dishonest actor often runs several schemes at once.

How Much Nonprofit Fraud Costs

The numbers from the ACFE Report to the Nations give a clear picture:

A stolen $76,000 is a program that does not run. The reputational hit with donors, grantors, and the public can outlast the financial one. In my work with nonprofits, I've seen organizations spend months rebuilding trust after a single incident that could have been caught earlier with basic visibility.

Why Nonprofits Are Easy Targets

Several conditions create opportunity in mission-driven organizations:

- A culture of trust. Leaders hire people who believe in the mission, then extend that trust to the checkbook.

- Lean finance teams. In a two- or three-person office, one person often requests, approves, records, and reconciles the same dollar. There is no second set of eyes.

- Volunteers and turnover. Seasonal volunteers and frequent staff changes make it hard to train people and keep duties separated.

- Cash, grants, and aid. Donations arrive as cash and checks. Grants and assistance flow out to other parties. Both directions invite skimming and diversion.

- Thin oversight budgets. Money goes to the mission first, so controls and training come last.

For most of the organizations we work with at KleerCard, the real exposure is not a sophisticated criminal. It is a manual, paper-based process where no one can see a transaction until the monthly statement arrives. Visibility, not suspicion, is what closes most of that window.

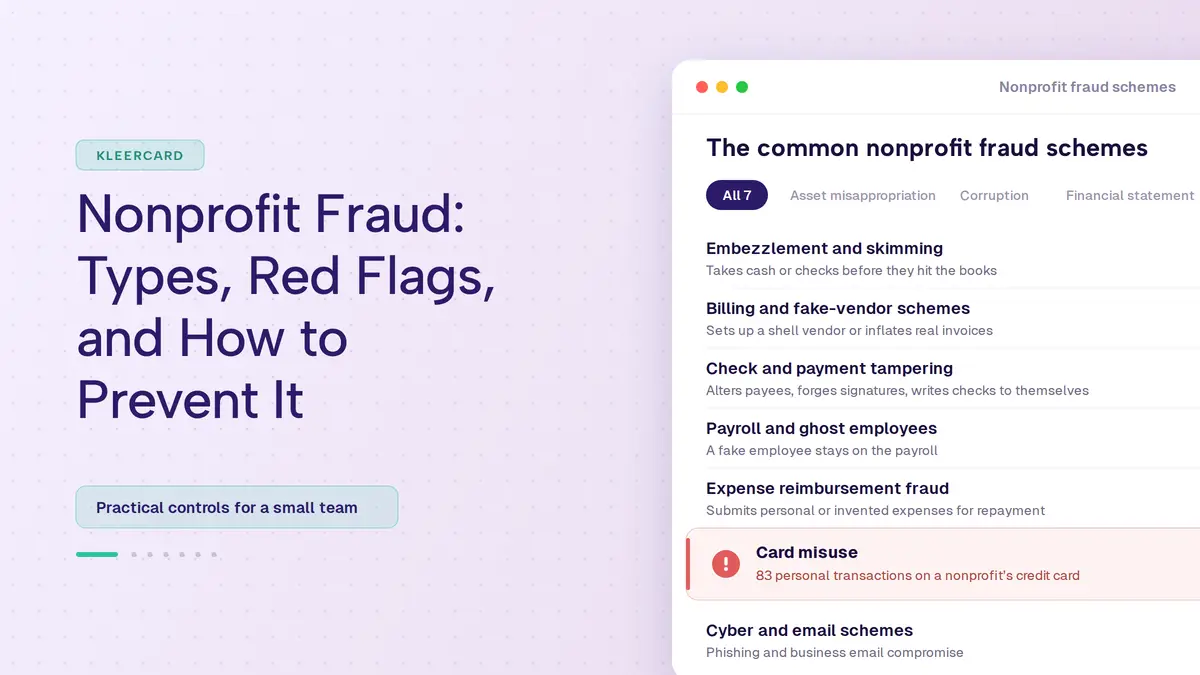

The Common Nonprofit Fraud Schemes

These are the schemes that actually show up in nonprofits:

Embezzlement and skimming

An insider takes cash or checks before they hit the books, or moves recorded funds to a personal account. Skimming is hard to detect because the money never entered the records.

Billing and fake-vendor schemes

A staffer sets up a shell vendor or inflates real invoices, then routes the overpayment to themselves. Billing schemes are among the most common in smaller organizations.

Check and payment tampering

Someone alters payees, forges signatures, or writes checks to themselves. Checks remain a heavy fraud target because they are still widely used.

Payroll and ghost employees

A fake employee stays on the payroll, or a real one gets unauthorized raises and hours. Whoever runs payroll alone can do this quietly for years.

Expense reimbursement fraud

A worker submits personal or invented expenses for repayment. Loose receipt rules make this one easy to start and hard to spot.

Card misuse

An organization card with a high limit gets used for personal purchases. In one widely reported case, an employee ran 83 personal transactions on a nonprofit's credit card before anyone noticed.

Cyber and email schemes

Phishing and business email compromise trick staff into wiring money or sharing credentials. Nonprofits hold donor data and often lack security training, which raises the risk.

Warning Signs of Fraud

Red flags fall into clear groups. None of them prove fraud on their own, but more than half of cases show at least one before discovery.

In the numbers and transactions

- Vendors with only a P.O. box, initials for a name, or an address that matches an employee's.

- Purchases that suddenly spike with one vendor, or invoices split into smaller amounts to slide under a review threshold.

- Transactions at odd hours, on weekends, or out of season.

In the documents

- Missing, altered, or backdated records.

- Originals that cannot be produced.

- Missing or questionable signatures.

In the structure

- One person controls spending, recording, and reconciliation with no review.

- Bank reconciliations that run months behind.

- A staffer who refuses to take vacation or hand off duties.

In the person

- Living visibly beyond their means.

- Unusually close ties to a vendor.

- Defensiveness about sharing access to records.

Red flags are signals to look closer, not proof.

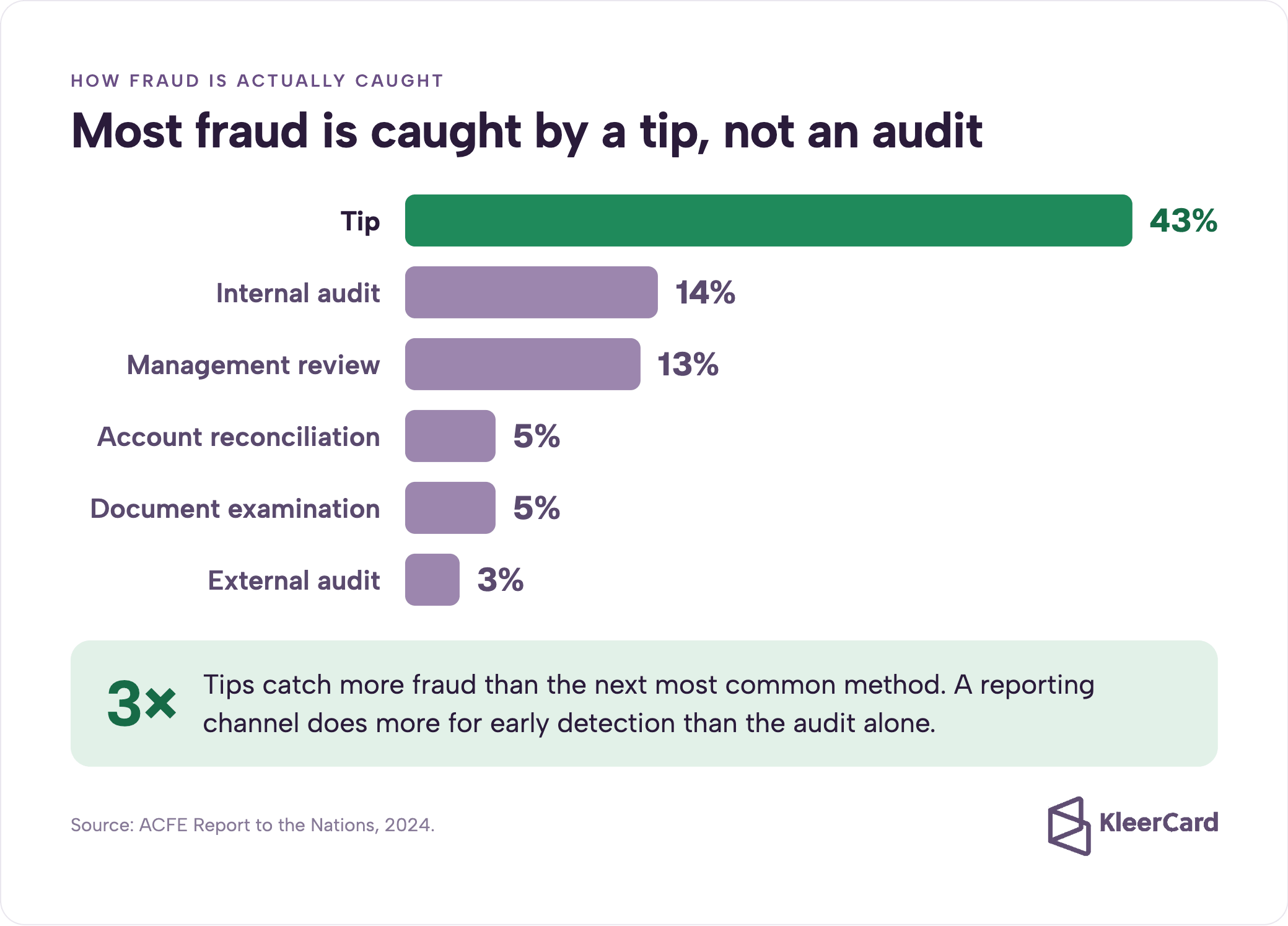

Why Audits and Good Intentions Are Not Enough

An annual audit is valuable, but it is not built to catch fraud. Auditors check whether the financial statements are fairly stated, and they rely in part on what the organization tells them.

Most fraud is caught by a tip, not an audit. Tips account for 43% of detections, more than three times the next method. A reporting channel does more for early detection than the audit alone. The point is not that audits fail. The point is that audits are one layer, and the layers that catch fraud early are visibility and a way for people to speak up.

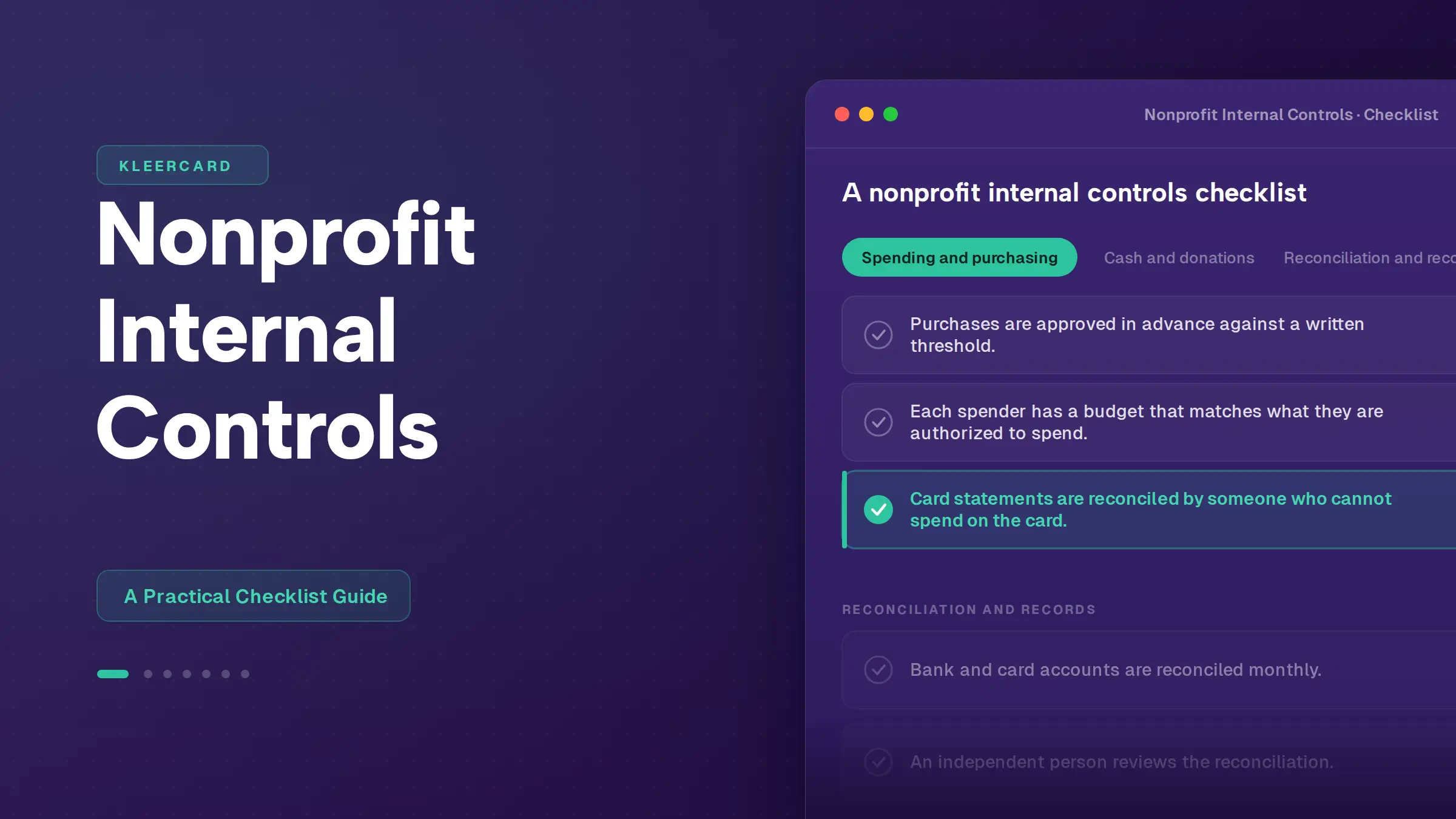

How to Prevent Fraud in Your Nonprofit

Practical controls for a small team focus on visibility and right-sized authority rather than heavy bureaucracy.

Separate who can spend, record, and reconcile

The person who spends money should not also record it and reconcile the account. For a team too small to split all three, use compensating controls such as having a board member or the treasurer review the monthly statement and reconciliation independently.

Give people a reporting channel

A simple, anonymous way to report concerns catches more fraud than any audit. Put a basic whistleblower policy in place with a hotline or web form, and name an independent person, often the audit committee chair, to receive reports.

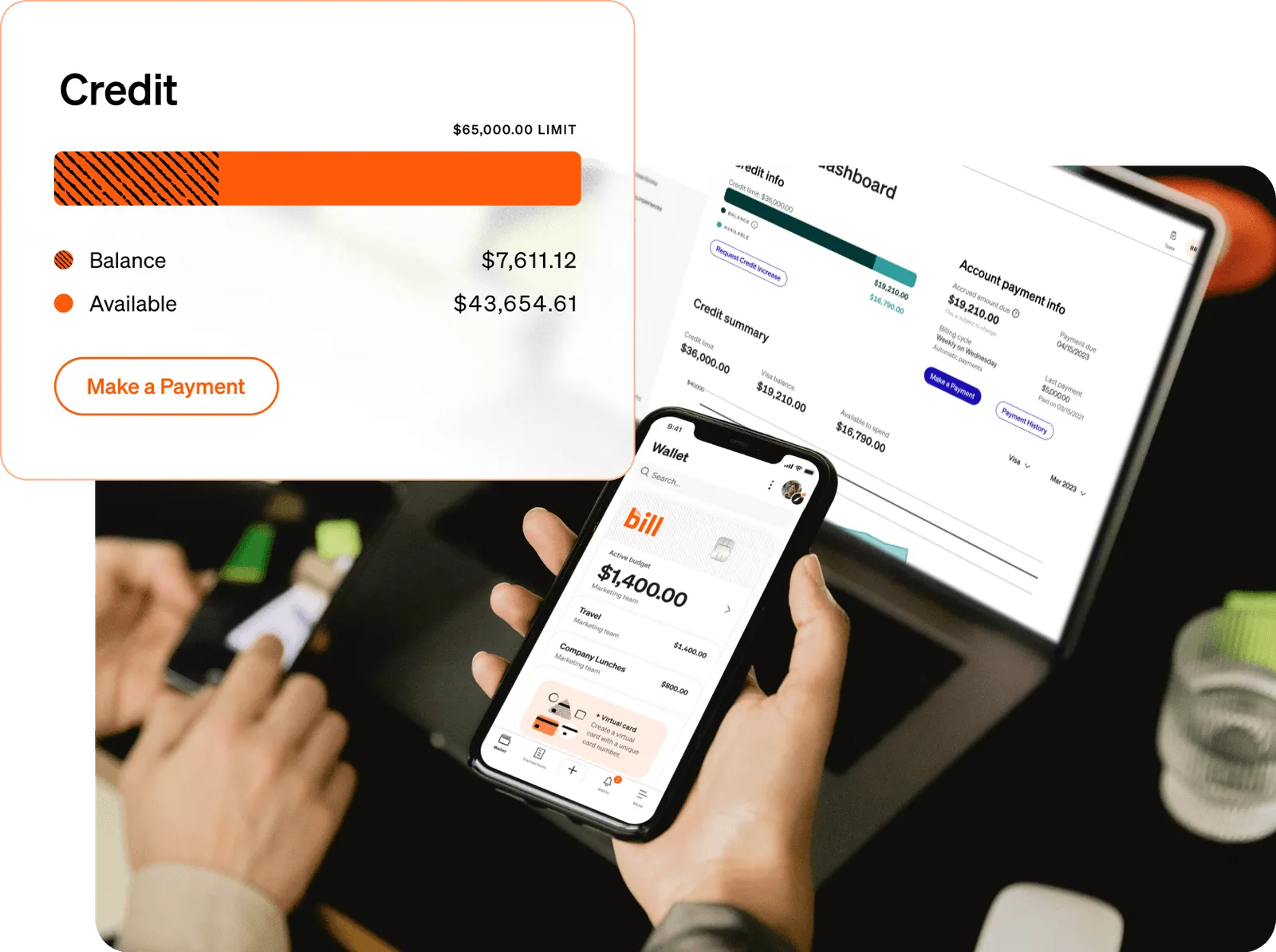

Right-size spending authority instead of leaning on high-limit cards

A single high-limit card kept in a drawer feels safe and is not. The person holding it could spend far beyond anything the organization intended, and no one would know until later.

We built KleerCard so each person gets their own card with a budget sized to what they actually need. The act of getting funds approved before a purchase is the control. If someone tries to spend beyond their budget, the card declines. That replaces the rule stacking that larger platforms rely on.

This approach fits small and high-trust finance teams. We do not run complex, multi-tier approval chains, and we do not plan to. Organizations that need rigid enterprise approval workflows should weigh that openly. Learn more about approvals for nonprofits.

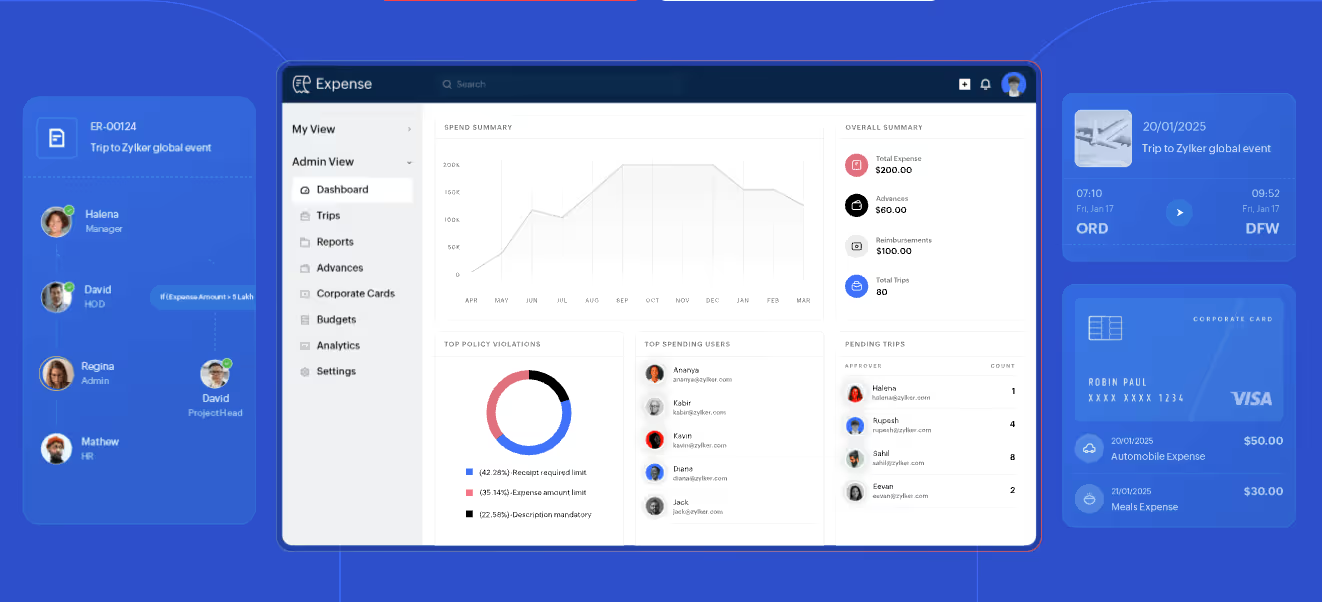

Make spending visible in real time

The longer fraud hides, the more it costs. Real-time visibility shrinks that window. When every transaction appears the moment a card is swiped, a questionable charge surfaces in days, not at month end.

At one private school we work with, the finance office can see each cardholder's charges as they happen. The one scare they had turned out to be a staffer's own forgotten subscription renewal, surfaced and resolved quickly because the charge was visible right away.

Pair real-time visibility with receipt capture at the point of sale, so documentation is attached before memories fade. See how expense management works and receipt tracking.

Lock down cash, checks, and reconciliations

Restrict access to cash and check stock the way you would protect cash itself. Require two people when counting cash. Keep bank reconciliations current, and bring in temporary help if they fall behind.

Set the tone from the board down

A written financial controls policy, board review of financials, and visible follow-through send the message that someone is watching. Most fraud needs the perception that no one is.

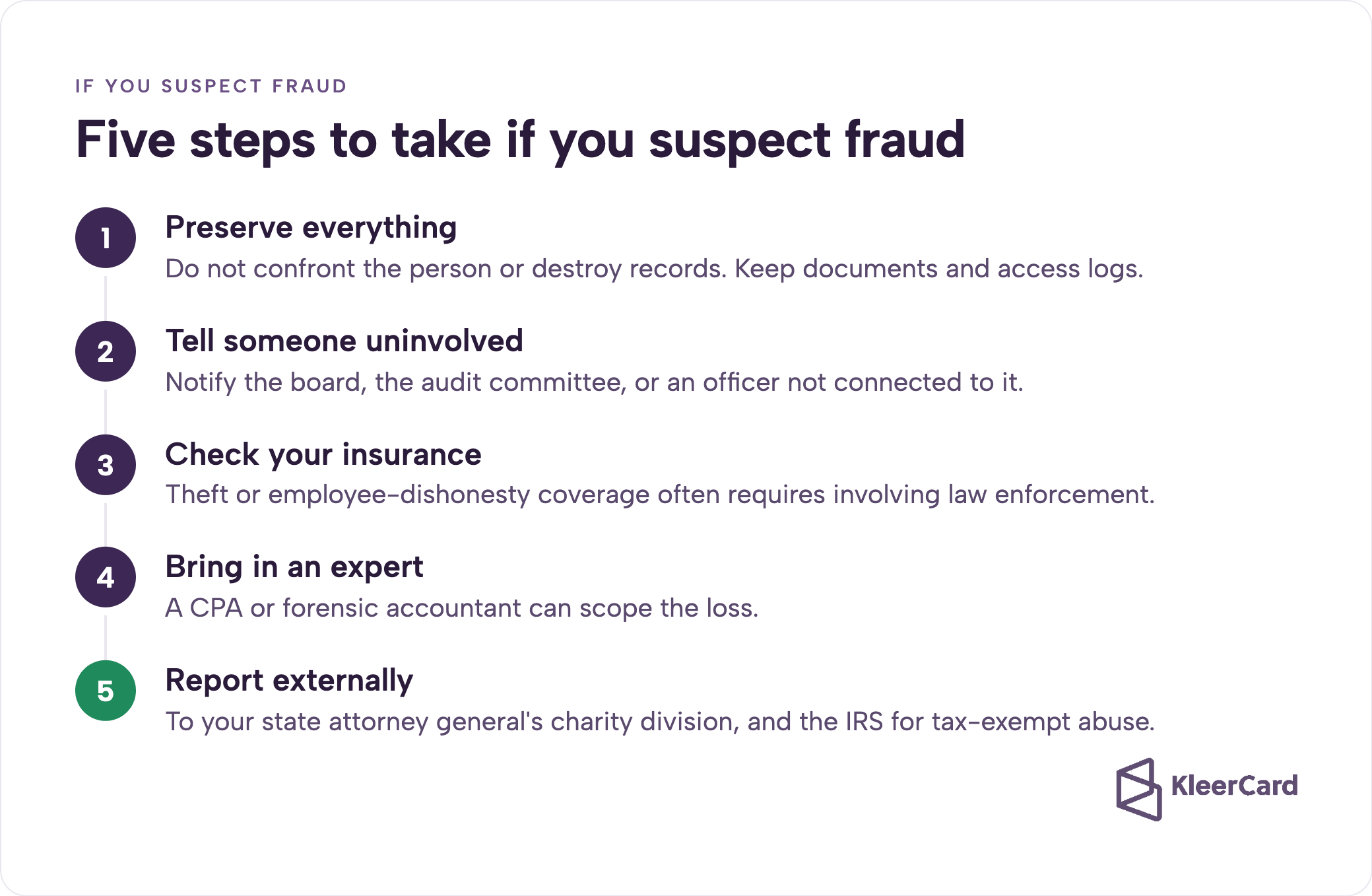

What to Do If You Suspect Fraud

Stay calm and follow these steps:

- Do not confront the person or destroy any records. Preserve documents and access logs.

- Tell the board, the audit committee, or an officer who is not involved.

- Check your insurance. Coverage for theft or employee dishonesty often requires you to involve law enforcement.

- Bring in a CPA or forensic accountant to scope the loss.

- Report externally where appropriate.

Oversight of nonprofits falls mostly to state attorneys general, and many states take complaints about charities through the AG's office. The IRS handles tax-exempt status abuse, and federal authorities step in for larger schemes such as grant or program fraud. See IRS resources on tax-exempt organizations and your state attorney general’s charity division.

Frequently Asked Questions

What is considered fraud in a nonprofit organization?

Fraud in a nonprofit is the misuse of its money, assets, or financial reporting by an insider or someone connected to it. It includes embezzlement, skimming, fake vendor billing, payroll and reimbursement schemes, card misuse, and misstating the books.

What are the most common types of nonprofit fraud?

Asset misappropriation is the most common category, covering embezzlement, skimming, billing schemes, check tampering, and expense fraud. Corruption, such as kickbacks and conflicts of interest, is the next most frequent. Financial statement fraud is rarer but the costliest per case.

How is fraud usually detected in nonprofits?

Most fraud is found through a tip, not an audit. Tips account for 43% of detections in the ACFE study, more than three times any other method. Internal audits, management reviews, and real-time transaction monitoring catch the rest.

Who investigates nonprofit fraud?

State attorneys general hold primary oversight of nonprofits, and most states take charity complaints through that office. The IRS addresses misuse of tax-exempt status, and federal agencies investigate larger cases involving grants or federal program funds.

Is nonprofit fraud a felony?

It can be. Embezzlement, wire fraud, and theft above state dollar thresholds are commonly charged as felonies. Penalties depend on the amount taken, the method, and the jurisdiction, and they can include prison time and restitution.

How do you report fraud at a nonprofit?

Start with the board, audit committee, or an officer not involved in the activity. Use the organization's whistleblower channel if one exists. For external reporting, contact your state attorney general's charity division, and the IRS for tax-exempt abuse.

Closing

Fraud needs opportunity, and most nonprofit opportunity comes from a single person spending unseen money on a manual process. The practical fix for a lean team is not a corporate control stack. It is right-sized spending authority, real-time visibility, and a channel for people to speak up.

If your organization wants spending controls and real-time visibility built for nonprofits rather than enterprises, that is the problem KleerCard was made to solve. Visit our nonprofit solutions page to see how it works in practice, check pricing, or explore expense management and approvals for teams like yours.

About the Author

Owen Hill is Co-founder of KleerCard and has over 20 years of experience in nonprofit finance and operations. He has worked with churches, schools, and mission-driven organizations on financial controls, spend management, and practical stewardship solutions.

Sources

- Association of Certified Fraud Examiners, Occupational Fraud 2024: A Report to the Nations (and 2026 update). Read the full report

- IRS guidance on charitable organizations and misuse of assets.

- First-party observations from KleerCard customer implementations.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)