%202.svg)

An accountable plan lets nonprofits, churches, and schools reimburse staff and volunteers tax-free. Learn the three IRS rules and how to set yours up.

Across the nonprofits, churches, and schools I have worked with, reimbursing people for out-of-pocket costs is routine. A volunteer fronts the gas for a trip, or a teacher buys her own classroom supplies. Whether you pay that money back tax-free or turn it into taxable wages depends on whether you run an accountable plan.

Most organizations reimburse without a written plan and assume the money is automatically tax-free. The IRS does not see it that way.

An accountable plan keeps those repayments tax-free. It runs on three rules and a few deadlines, and any organization can set one up for both staff and volunteers.

An accountable plan is a written reimbursement arrangement that meets IRS rules. Money you pay back to staff and volunteers under the plan is not taxable income. Reimbursements stay off the W-2 and carry no payroll tax. The rules come from Treasury Regulation 1.62-2 and IRS Publication 463.

Any organization can adopt one, including tax-exempt organizations. The plan can be a single policy your board approves and dates.

Without an accountable plan, the IRS treats your reimbursements as wages. The amount lands on the worker's W-2. You withhold and pay payroll tax on it. The worker owes income tax on money that only paid back a business cost.

Tax-exempt status does not change this. Exemption applies to your organization's income. Your payroll obligations for the people you pay are separate. Reimburse a pastor's mileage outside an accountable plan, and that payment becomes taxable wages.

As a budget director and later as a fractional CFO for nonprofits, I watched reimbursements get tangled in payroll. Running them through payroll forces an extra split at bank reconciliation. It also breaks the reconciliation checks you rely on, because these payments carry no payroll tax.

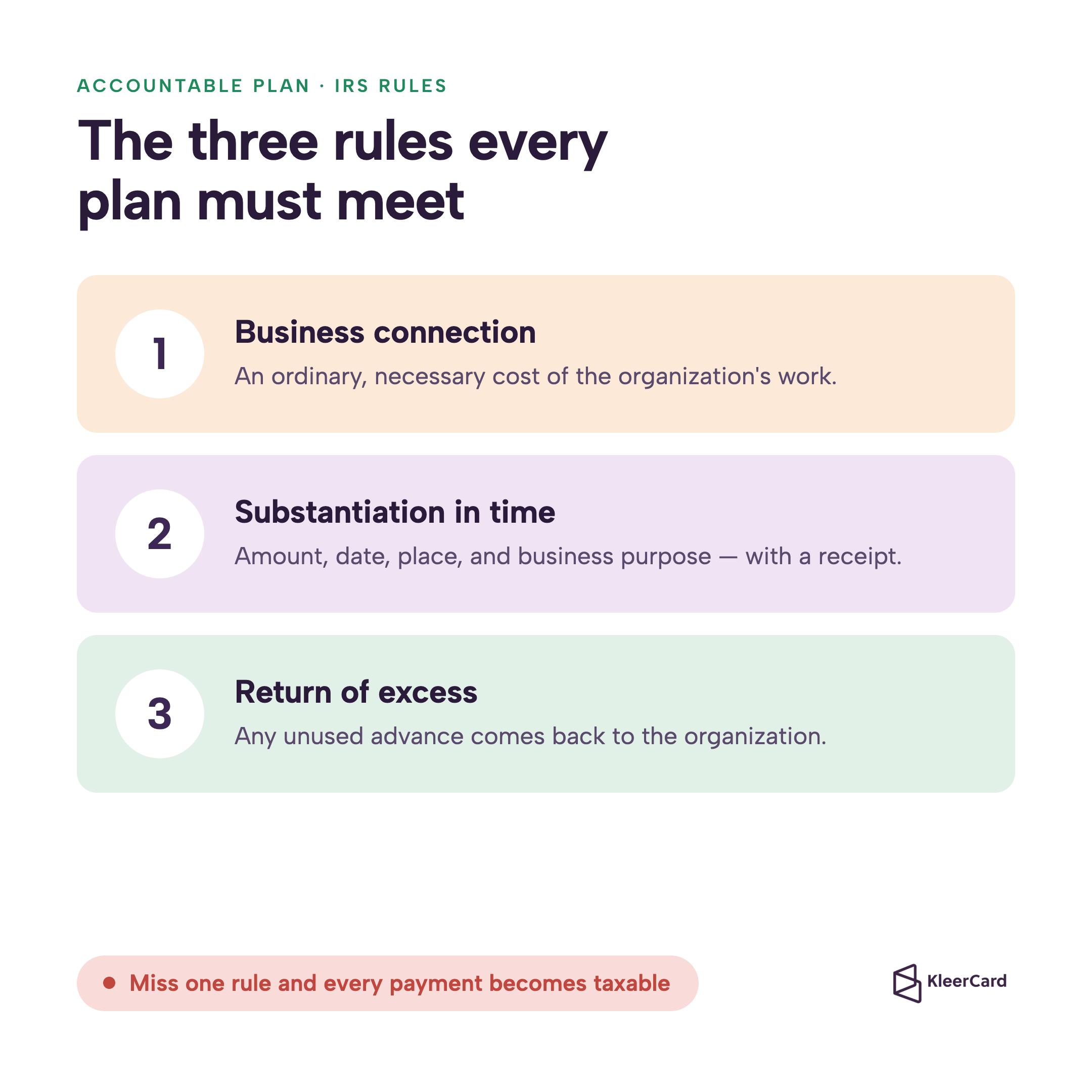

An accountable plan has to meet all three of these requirements. Miss one, and the whole arrangement becomes non-accountable, which makes every payment under it taxable.

The expense has to be an ordinary and necessary cost of your organization's work, paid while the person performs their role. A teacher's classroom supplies qualify. A pastor's personal grocery run does not.

The person has to document each expense with the amount, date, place, and business purpose. Receipts, canceled checks, or invoices back it up. A receipt with no stated purpose is not enough.

If you advance money and the actual cost comes in lower, the person has to return the difference. If nobody reconciles the advance, the IRS treats the unspent portion as taxable income.

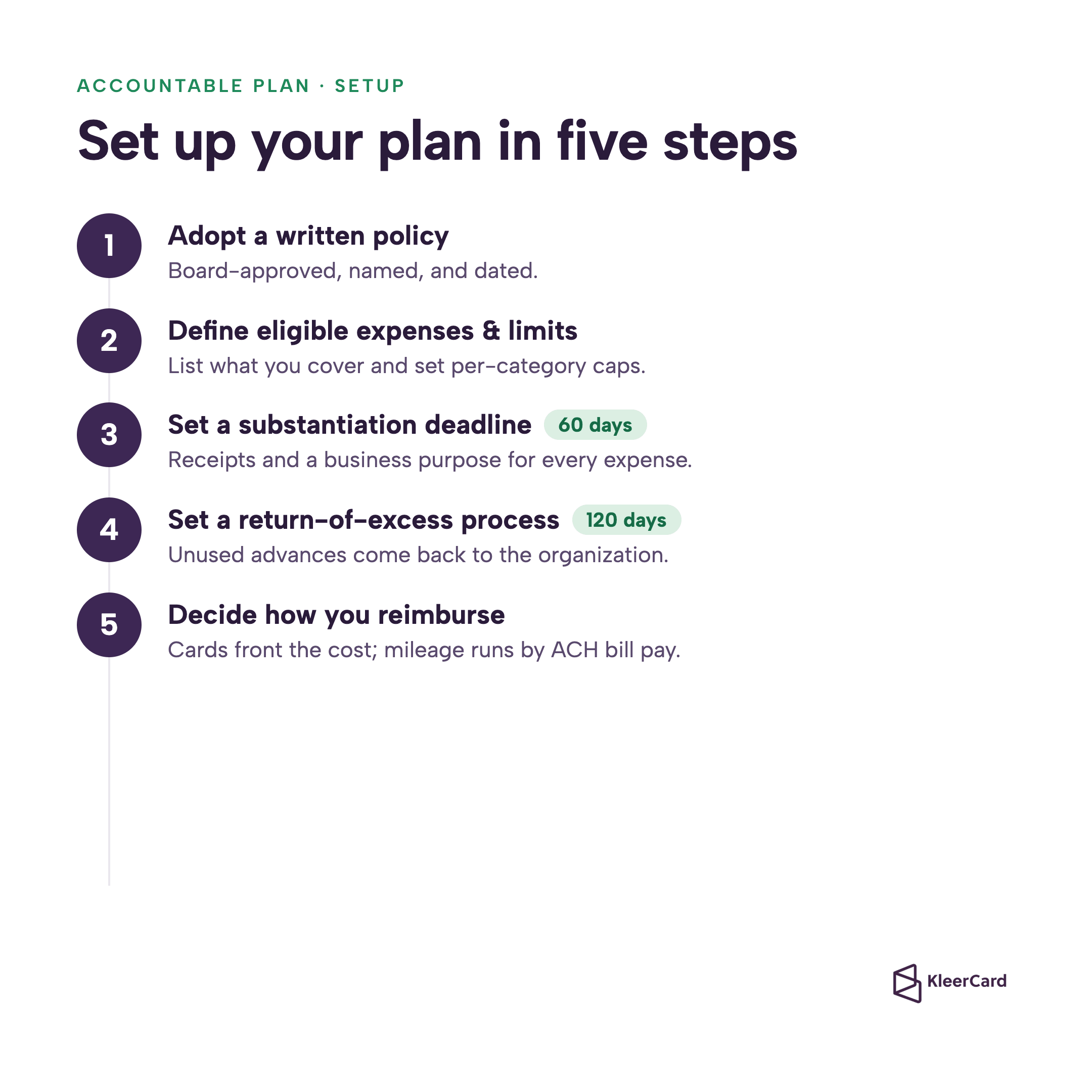

The regulations do not fix a single deadline. Instead, the IRS gives safe harbors that most policies adopt as their own standard:

Writing these windows into your policy is the cleanest way to show an accountable plan exists if the IRS asks.

The same $500 reimbursement is a clean repayment under an accountable plan. Under a non-accountable plan, it becomes a taxed wage.

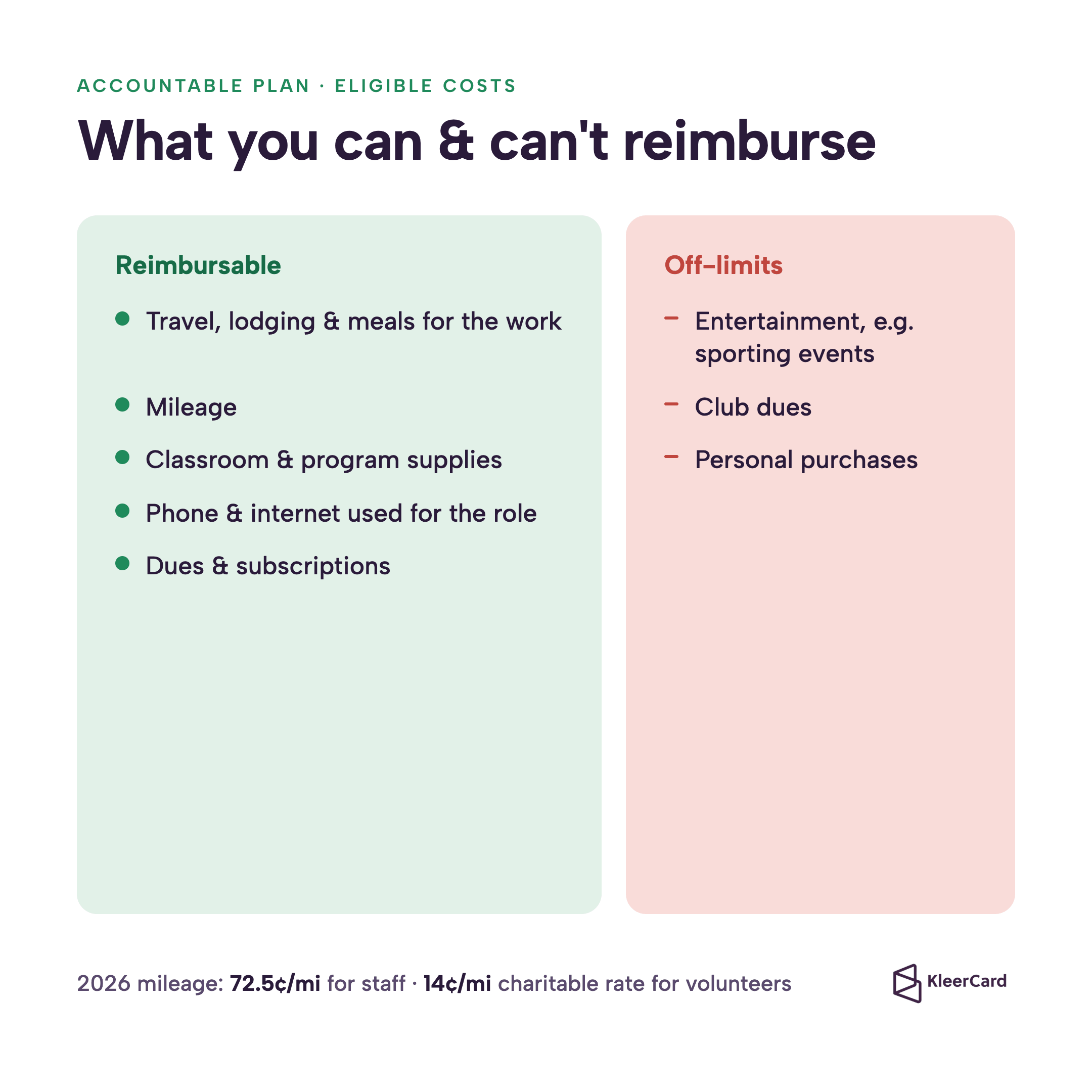

Most costs tied to your mission qualify. Common reimbursable expenses include:

Entertainment costs, such as sporting events or club dues, cannot run through an accountable plan.

Mileage carries a rule worth getting right. For employees, the 2026 business standard mileage rate is 72.5 cents per mile. Reimbursing at that rate stays tax-free under an accountable plan. For volunteers driving on behalf of your organization, the charitable rate is 14 cents per mile, set by statute. Reimbursing a volunteer above their documented cost can create taxable income, so most organizations reimburse actual expenses or apply the charitable rate.

A church reimbursement done right keeps a pastor's business expenses off their taxable income. A church accountable reimbursement plan covers ministry travel, books, and conference fees. The same three rules apply, and the reimbursements stay tax-free.

This is separate from a housing allowance, which follows its own rules. Ministers also have a distinct tax status that affects how they file. A church setting up a plan benefits from a quick review of how taxes work for ministers, ideally with a tax advisor. A documented plan stops legitimate ministry costs from being taxed as pay.

You can reimburse volunteers for documented out-of-pocket costs without the money counting as income, as long as your plan's rules are met. Mileage is the expense a card cannot replace, since volunteers drive their own vehicles.

I work with a nonprofit in North Carolina that does a lot of travel, and even its volunteers rack up mileage. We set each volunteer up as a vendor, so they enter their own bank details and get paid by ACH overnight. A volunteer who submits a form today sees the deposit a day or two later. Fast, documented reimbursement builds volunteer confidence, and it keeps the payment out of payroll.

A plan works best alongside a clear expense-reporting process. It also pairs with the financial controls a treasurer already maintains.

A card can remove a reimbursement before it ever happens. When a teacher or volunteer carries a card with a set limit, they buy what they need without fronting money or filing a form. They capture the receipt at checkout.

We built KleerCard for nonprofits, churches, and schools. A card program changes how many reimbursements a finance team handles, because people stop floating costs and waiting weeks to be paid back.

Before, finance often could not tell which budget a reimbursed purchase belonged to. Cards show the budget at the moment of purchase, which is what expense management built for nonprofits is for.

The reimbursements that remain, like mileage, run through bill pay and reimbursements by ACH, kept off payroll and easy to track per person.

No. An accountable plan is optional. Without one, though, the IRS treats reimbursements as taxable wages, so most organizations adopt a plan to keep repayments tax-free.

No. When you meet the three requirements, reimbursements are not income to the worker. They stay off the W-2 and carry no payroll tax.

A church is not required to have one. Without it, though, reimbursements to pastors and staff become taxable wages. A written plan keeps ministry expense reimbursements tax-free.

The unsubstantiated amount becomes wages. It lands on the W-2, picks up payroll tax, and the worker owes income tax on it.

Yes. You can reimburse volunteers for documented out-of-pocket costs without it counting as income. Volunteer mileage is commonly reimbursed at the 14-cent charitable rate or at documented actual cost.

Not under an accountable plan. Reimbursements that meet the rules are not wages, so no payroll tax applies. Mishandled reimbursements become wages and do trigger payroll tax.

An accountable plan is a short, written policy that keeps reimbursements tax-free and off the W-2. Build it on the three rules: business connection, substantiation, and return of excess. The 60-day and 120-day deadlines make the plan easy to prove. A tax advisor can confirm the details for your situation.

A card program cuts how often you reimburse at all. If your nonprofit, church, or school still runs on personal cards and expense forms, the next step is practical. Move spend onto cards, and route the reimbursements you still need through one platform built for nonprofits, churches, and schools.

Speak to a member of our team and we can have you up and running in minutes, not weeks.