%202.svg)

The average nonprofit finance team spends 15 to 20 hours every week on administrative tasks that could be automated. For most organizations, the biggest drain on that time is expense reporting. Chasing receipts, manually coding transactions, reclassifying expenses before audit, and preparing Form 990 narratives from scratch each year add up to hundreds of hours annually that could go toward mission work instead.

If your nonprofit's expense reporting process feels like a burden, it is probably not set up correctly. The good news is that the fundamentals are not complicated. What makes nonprofit expense reporting different from standard business accounting is the stewardship standard: you are not just tracking what was spent, you are demonstrating to donors, grantors, auditors, and the IRS that every dollar served your mission.

This guide covers the core best practices for nonprofit expense reporting in 2026, including IRS compliance requirements, functional expense classification, reimbursement policies, automation tools, and Form 990 preparation. Use it as a reference for building or improving your organization's finance process this year.

Why Nonprofit Expense Reporting Carries a Different Standard

For-profit companies report expenses primarily for tax and investor purposes. Nonprofits report expenses to demonstrate stewardship. Functional expense reporting segments costs into program services, management and general activities, and fundraising efforts, allowing donors to see exactly what percentage of their contribution funds programs versus overhead. That distinction matters enormously when donors decide where to give and when grantors evaluate who to fund.

A nonprofit that can showcase a high percentage of its expenses flowing directly into its programs is often more appealing to donors. Charity watchdog organizations analyze these ratios closely, and they are visible to anyone who looks up your Form 990 on the IRS's public database.

Your expense reports are not internal documents. They shape how the outside world perceives your organization, and getting them right is foundational to long-term credibility.

The Three Functional Expense Categories Every Nonprofit Must Know

The foundation of nonprofit expense reporting starts with correctly classifying all costs into the three categories required by GAAP and IRS Form 990. Getting these categories right is not optional: proper expense categorization helps demonstrate that your nonprofit is focused on its mission, a key factor the IRS considers when evaluating tax-exempt organizations.

Program Services Expenses

Program services expenses directly relate to your exempt purpose. These are costs tied to mission delivery, such as program staff, program supplies, and direct service delivery. If you operate a food pantry, the food and the staff serving it belong here. If you run youth mentorship sessions, the direct costs of those sessions are program expenses.

Salaries require careful allocation. If an employee spends 50% of their time directly supervising a program and 50% on general management, you would allocate 50% of that employee's salary to program services and 50% to management and general expenses. Time studies and activity logs are the most defensible way to document these splits. For a deeper look at how this works in practice, see our guide to fund accounting for churches.

Management and General Expenses

Management and general expenses cover administrative costs such as finance, HR, IT, legal, and governance that support the whole organization. These are your overhead costs. They are necessary, legitimate, and sometimes misunderstood by donors who equate lower overhead with greater effectiveness.

Fundraising Expenses

Fundraising expenses cover the costs of raising charitable contributions, including development staff, campaigns, special events, and fundraising consultants.

Together, management and general plus fundraising make up what is typically called "overhead." The IRS does not mandate any specific spending ratio across these categories, but charity evaluators and many major donors watch these numbers closely.

The Four Financial Statements That Support Expense Reporting

Expense reporting does not exist in isolation. It feeds into a complete set of financial statements that your organization should prepare every year.

Nonprofits should compile four financial statements annually: the Statement of Activities, the Statement of Financial Position, the Statement of Cash Flows, and the Statement of Functional Expenses. While the first three have direct for-profit parallels, the Statement of Functional Expenses is unique to nonprofits because it specifically focuses on how your finances further your mission.

The Statement of Functional Expenses is a matrix-style report that shows both what you spent money on (salaries, supplies, rent) and the purpose behind each expenditure (program, admin, fundraising). This dual-dimension view gives your board and your donors a clearer picture than any single-column expense list can provide.

Accountable vs. Non-Accountable Plans at a Glance

FeatureAccountable PlanNon-Accountable PlanReimbursements taxable?NoYes, treated as wagesReported on Form W-2?NoYesPayroll taxes due?NoYesDocumentation required?Yes, within 60 daysNot requiredExcess must be returned?Yes, within 120 daysNo

Aligning Your Chart of Accounts With Form 990

One of the most time-consuming problems nonprofits face at year-end is the mismatch between how expenses are recorded in their accounting software and how they need to appear on Form 990. This disconnect forces manual reclassification that can take days and introduces errors.

Starting with a chart of accounts aligned with Form 990 and FASB ASC 958 requirements is a critical first step. This means mapping natural expense categories such as salaries, benefits, rent, utilities, supplies, and professional services, then linking each department or project to a functional category: program, management and general, or fundraising. Using segment codes or classes in accounting platforms to capture both natural and functional dimensions reduces year-end manual recoding and enables meaningful, timely church expense tracking.

The best practice for greatest accuracy is to name line items clearly with commonly understood word meanings rather than jargon or vague names subject to interpretation. When your finance staff and program staff use different terminology for the same expense, budget comparisons become unreliable and audit preparation becomes painful.

Writing a Cost Allocation Policy That Holds Up to Scrutiny

Shared costs are one of the trickiest areas of nonprofit expense reporting. Rent, utilities, the executive director's salary, and general IT tools often benefit more than one functional category. How you allocate those costs matters for accuracy, for GAAP compliance, and for the credibility of your Form 990.

Many organizations struggle to apply consistent, supportable allocation methods, leading to inaccurate functional expense statements or auditor concerns.

A written cost allocation policy solves this. It should include documented written allocation methodologies approved by management or the audit committee, using time studies or activity logs to allocate personnel costs accurately, and applying reasonable bases such as square footage for occupancy or FTE count for shared services. Review and update allocations annually to reflect operational changes.

To see how this works in practice: if your executive director earns $120,000 and spends approximately 60% of their time on program oversight and 40% on administration, $72,000 flows to program expenses and $48,000 flows to management and general. Document that split in writing, apply it consistently, and review it each year as responsibilities evolve.

An allocation methodology that was accurate two years ago may no longer reflect how your organization actually operates. Annual review is not a formality. It is how you keep your financial statements honest.

Restricted fund tracking is especially critical in any cost allocation policy. Grants and donor-restricted gifts each come with specific usage requirements that must be reflected in how you classify expenses. For organizations managing multiple funding streams, KleerCard's restricted funds tracking tools make this significantly easier.

Building an IRS-Compliant Accountable Plan for Reimbursements

Any time a staff member, volunteer, or board member spends personal money on behalf of your organization, you need a formal reimbursement process. Without one, those payments become taxable income.

Any undocumented expenses are classified as employee compensation and are subject to federal business and employment taxes. If this unrelated business income exceeds $1,000, your nonprofit must file Form 990-T.

The IRS requires accountable plans to meet three specific criteria: employees must prove a business connection, offer adequate documentation, and return any unsubstantiated reimbursements.

Here is what each requirement means in practice:

Business Connection: The expense must be directly related to the nonprofit's mission and activities. Personal expenses cannot be reimbursed, even if they occur during a business trip.

Timely Documentation: Employees and volunteers must submit their expense claims within a reasonable period, typically 60 days after the expense is incurred. Receipts must show the date, vendor, amount, and purpose of the purchase.

Return of Excess Advances: Any unspent cash advances must be returned to the organization within 120 days.

For mileage reimbursements, use the correct IRS rate for 2026. According to the 2026 IRS standard mileage rates, the rate is 72.5 cents per mile for business use and 14 cents per mile for charitable use. The charitable rate is set by statute and has not changed since 1998. Reimburse employees at the business rate and volunteers at the charitable rate. Reimbursing volunteers above 14 cents per mile may create taxable income for the volunteer unless handled correctly.

Although the IRS does not require accountable plans to be written or submitted, it is highly recommended that the plan be documented and made available to all employees and volunteers of the nonprofit. A written policy removes ambiguity, sets expectations, and gives you a defensible record if your practices are ever questioned during an audit. For complete IRS guidance on accountable plans, see IRS Publication 463. To manage reimbursements alongside bill pay in a single platform, see how KleerCard handles bill pay and reimbursements.

Month-End Close: Why Consistency Prevents Year-End Chaos

Many nonprofits focus nearly all their financial energy on annual audits and Form 990 preparation, treating monthly statements as informal management tools. That approach creates serious problems.

This creates problems when year-end arrives and accounting teams discover unreconciled accounts, missing documentation, or classification errors that require extensive cleanup.

A disciplined monthly close prevents that scramble. Closing the books by a specific date each month, typically within 10 business days of month-end, means reconciling all bank accounts, credit cards, and loan balances, reviewing accounts receivable aging, and classifying expenses by both natural and functional categories as you record them, not retroactively during audit prep.

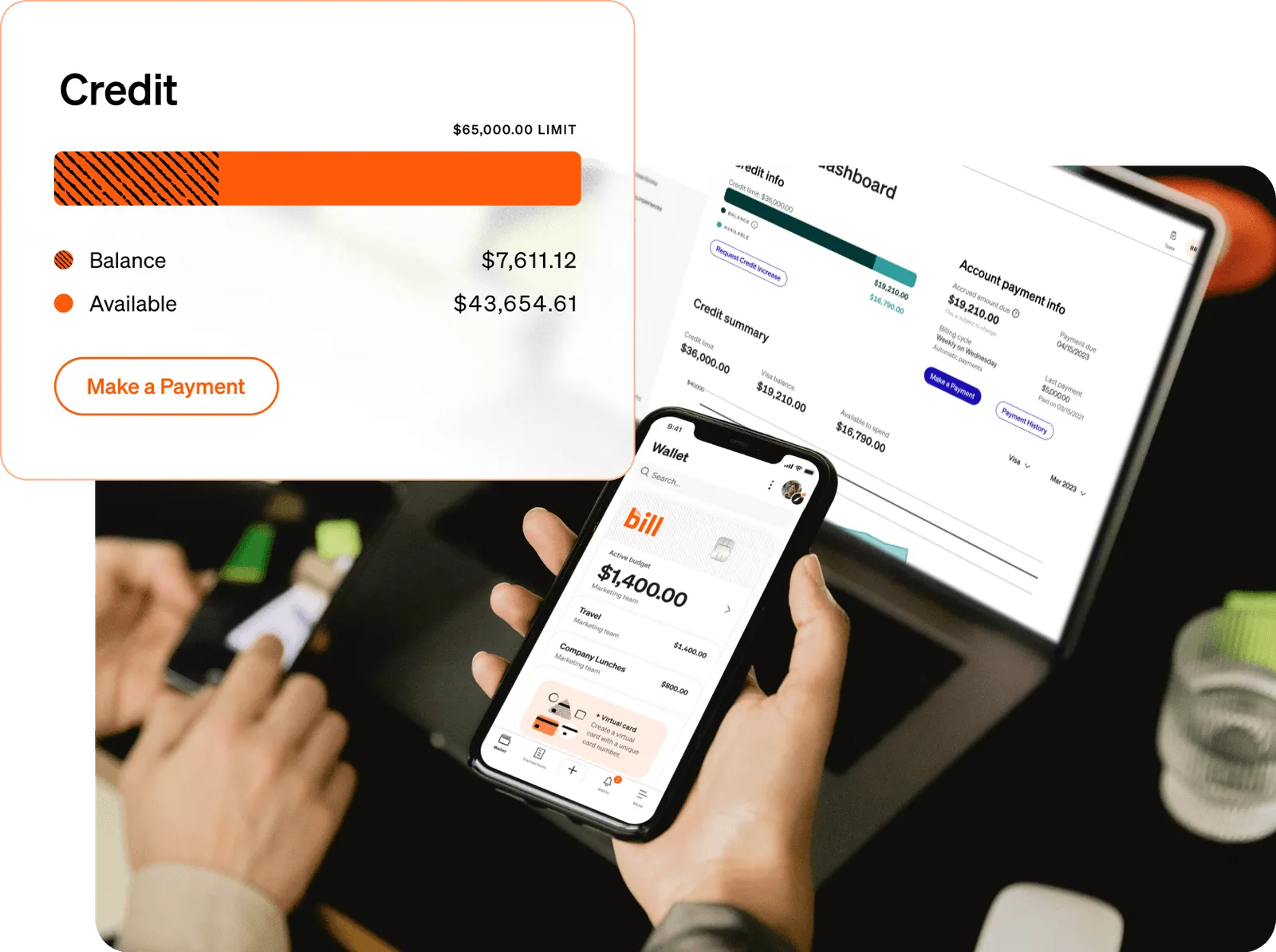

Organizations using KleerCard have reduced their month-end close from 40 hours to just one. That transformation happens because expenses are coded in real time, receipts are captured automatically, and nothing gets left for the end of the month to sort out.

When you build these habits into a monthly rhythm, year-end becomes a review rather than a rescue operation.

Want to see how KleerCard can cut your close time? Schedule a free demo.

Spend Controls: Managing Nonprofit Expenses Before They Happen

The most effective nonprofit expense management happens before a transaction occurs. Expense reporting after the fact is important. Preventing unauthorized or misclassified spending in the first place is better.

A clear and thorough expense policy, reimbursement policy, and credit card policy can go a long way in helping your employees and stakeholders understand the difference between necessary and inappropriate spending.

Approval workflows ensure that purchases above a set threshold get reviewed before funds are committed. Virtual and physical cards with pre-configured spending limits prevent budget overruns before they happen. For a deeper look at how churches and nonprofits structure these controls, see our guide to church spending controls.

For church and faith-based nonprofits in particular, stewardship is not just a financial principle. It is a core organizational value. The systems you put in place either reflect that value or undermine it.

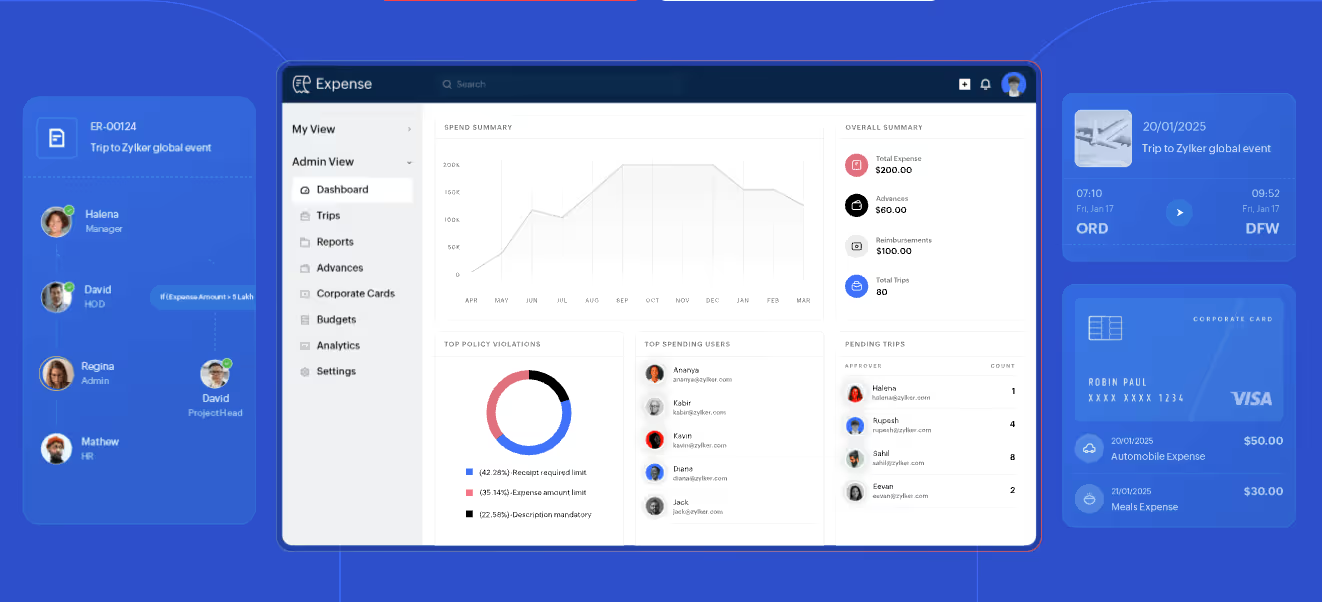

Nonprofit Expense Reporting Automation: What's Actually Working in 2026

Manual expense reporting has always been time-consuming. In 2026, there is no reason most nonprofit finance teams should still rely on paper receipts and spreadsheet-based processes.

Tools using OCR and AI can pull data straight from receipts and invoices, eliminating the need for manual data entry. Digital approval workflows replace the cumbersome back-and-forth of paper processes. Integrating expense systems with accounting software removes the hassle of manual data transfers.

The results organizations are seeing are significant. After adopting an automated expense platform in June 2025, one finance team saved 40 hours each month, cut reconciliation time by half a day, reduced processing costs by $30,000, and saved an extra $5,000 annually on storage.

AI and machine learning are becoming increasingly important for nonprofit financial management. Practical applications include smart grant compliance checks that monitor spending against approved budgets, expense anomaly detection that identifies unusual spending activity or incorrect fund allocations, and natural language financial queries that allow staff to ask questions like "How much of our restricted funding remains for the education program?" and receive immediate answers without digging through reports.

On average, AI-driven automation is saving nonprofits an estimated 15 to 20 hours per week in administrative time. For lean finance teams already spread across multiple responsibilities, that time goes directly back to mission-critical work.

That said, automation works best when it addresses a specific problem. The nonprofits seeing real value from AI are using it to automate the mundane work that eats up staff time: invoice processing, data entry, and back-office operations. Start with the most repetitive steps in your expense workflow and build from there, rather than investing in broad platforms you will only partially use.

When evaluating nonprofit expense reporting software, look for these core capabilities:

- Real-time receipt capture via mobile app or email forwarding — see how KleerCard's receipt tracking works

- AI-powered expense coding that maps to your chart of accounts automatically

- Approval workflows with configurable rules by amount, category, or department

- Fund and grant tracking that separates restricted and unrestricted spending

- Direct integration via KleerCard's accounting sync with your existing accounting platform (QuickBooks, Sage Intacct, etc.)

- Digital audit trails with timestamped records of every transaction and approval

Form 990 Expense Reporting: How to Prepare Year-Round

IRS Form 990 is one of the most public documents your nonprofit produces. Donors review it. Charity watchdog organizations analyze it. Grantors consult it before making funding decisions. The way your expenses appear on this form, guided by the IRS Form 990 instructions, tells your organization's story in numbers.

Form 990 preparation starts in January, not March. Capturing required information throughout the year reduces errors, enables meaningful board review, and ensures your public filing accurately tells your organization's story. Narrative descriptions of programs should clearly articulate mission impact, expense allocations should demonstrate reasonable program spending percentages, and compensation should align with comparable organizations.

Restricted fund tracking is especially critical here. Restricted funds require systems that monitor spending against approved budgets, track expiration dates, and maintain compliance files with original agreements and expenditure documentation. A grant report showing funds spent outside approved categories is not just an accounting error. It can damage funder relationships and trigger claw-back requirements.

Schedule O of Form 990 provides space to explain your organization's programs, governance policies, and financial practices in plain language. Many nonprofits treat this section as a compliance obligation and write as little as possible. Organizations that use it well treat it as a narrative opportunity: an explanation of impact that donors and funders will actually read.

Year-round Form 990 preparation also means capturing executive compensation data, conflict-of-interest policy documentation, and whistleblower policy confirmation throughout the year rather than scrambling for it in March.

Board Financial Reporting That Enables Real Oversight

Your board has a fiduciary responsibility to your organization. They cannot fulfill that responsibility without financial information that is clear, timely, and actionable.

Many nonprofits provide board members with full financial statements that accountants understand but leave board members uncertain about organizational financial health. A 40-page audit report sent the day before a board meeting is not useful governance. A concise financial package with the right metrics and a plain-language narrative is.

An effective board financial package typically includes budget versus actual comparisons broken down by program, key metrics like cash position and net assets, restricted fund balances, and a brief narrative explaining significant variances. For nonprofits that want to give their board clearer visibility into how spending breaks down by function, KleerCard's program vs. admin spend reporting tool makes this straightforward.

Good internal distribution means providing monthly financials to the Executive Director, quarterly financials to the board, and annual audited statements to the full board, with grant reports shared with program staff as needed.

When board members understand the numbers, they can ask better questions, spot early warning signs, and make more informed decisions about resource allocation and program investment.

How Expense Reporting Connects to Donor Trust

Every donor who gives to your organization is trusting you to use their gift wisely. Transparent, accurate expense reporting is how you honor that trust in concrete terms.

Transparent expense tracking builds credibility with donors, board members, and grantmakers. Well-documented and reported expenses show that your nonprofit is responsible and mission-focused.

This is especially true for church-based and faith-driven organizations, where the expectation of stewardship runs through everything the ministry does. Jared, an Executive Pastor at Plum Creek Christian Church who uses KleerCard, described the impact directly: "We went from month-end close taking 40 hours to collect receipts and code expenses, to our first month with KleerCard only needing 1 hour. Best decision we could have made."

That kind of improvement does not just save time. It frees leadership to focus on the work that actually matters.

A 2026 Nonprofit Expense Reporting Checklist

Use this as a starting point for assessing where your organization stands today:

Chart of AccountsAlign account codes with Form 990 categories and FASB ASC 958 requirements. Use segment codes to capture both natural and functional expense dimensions simultaneously.

Cost Allocation PolicyDocument a written methodology approved by your audit committee or leadership. Apply it consistently and review it every year.

Accountable PlanPut your reimbursement policy in writing. Distribute it to all staff and volunteers. Train your team on the 60-day documentation requirement and 120-day excess return rule. Update mileage rates to 72.5 cents per mile (employees) and 14 cents per mile (volunteers) for 2026.

Monthly CloseSet a firm close date within 10 business days of month-end. Build reconciliation and functional expense classification into the monthly routine, not year-end cleanup.

Spend ControlsEstablish card limits, approval workflows, and written spending policies before expenses occur. Separate virtual and physical card issuance by role and department.

AutomationIdentify the biggest manual bottlenecks in your expense process (receipt collection, coding, approvals) and find a tool that addresses them directly. Prioritize integration with your existing accounting software.

Form 990 PreparationStart capturing program narratives, restricted fund documentation, compensation data, and governance policy confirmations in January, not at year-end.

Board ReportingRedesign your board financial package to lead with key metrics and plain-language explanations, with supporting detail available on request.

How KleerCard Supports Nonprofit Expense Reporting

KleerCard was built specifically for nonprofits and church finance teams that need expense management software designed around how mission-driven organizations actually work.

Physical and virtual cards with configurable spending limits give your team the freedom to spend on mission while protecting against overspending. AI-driven fund classification automatically codes expenses to the right program or department, cutting the manual work at month-end. Bill pay and reimbursement management bring all outgoing expenses into a single platform, making reconciliation and reporting significantly faster.

Organizations like Plum Creek Christian Church have reduced their month-end close from 40 hours to just one hour after switching to KleerCard. Finance teams report that staff love the simplified process, and leadership gains complete visibility into spending without needing to chase receipts or re-code transactions.

If your current expense reporting process is taking more time than it should, or if you are heading into a year-end audit and feeling unprepared, KleerCard for nonprofits can help.

Schedule a demo today and see how KleerCard can help your nonprofit spend smarter and report with confidence.

Frequently Asked Questions About Nonprofit Expense Reporting

What are the three expense categories on IRS Form 990?

The IRS requires nonprofits to categorize expenses into three main areas: program expenses that tie directly to mission-related activities, management and general expenses that relate to running the organization as a whole, and fundraising expenses that cover the process of soliciting donations and managing donor relationships.

What is an accountable plan for nonprofits?

An accountable plan is a reimbursement structure that meets IRS requirements under Treasury Regulation 1.62-2, allowing nonprofits to reimburse employees, volunteers, and board members for business expenses without those payments being classified as taxable wages. To qualify, expenses must have a clear business connection, be documented within 60 days of being incurred, and any excess advances must be returned within 120 days.

What are the 2026 IRS mileage reimbursement rates for nonprofits?

According to the 2026 IRS standard mileage rates, the rate is 72.5 cents per mile for business use and 14 cents per mile for charitable use. The charitable rate is set by statute and has not changed since 1998. Reimburse employees at the business rate and volunteers at the charitable rate when operating under an accountable plan.

How often should nonprofits reconcile expenses?

Monthly reconciliation is best practice. Closing the books within 10 business days of month-end and classifying expenses by both natural and functional categories as you record them prevents the year-end scramble that plagues many organizations.

What documentation is required for nonprofit expense reimbursements?

At minimum, documentation should include a receipt showing the date, vendor, amount, and items purchased, along with a brief description of the business purpose. For mileage, a contemporaneous log with dates, destinations, and purposes is required. For travel advances, any unspent amount must be returned within 120 days.

How can automation improve nonprofit expense reporting?

Automation tools using OCR and AI can pull data straight from receipts and invoices, digital approval workflows replace paper-based processes, and integration with accounting software removes the need for manual data transfers. Expense costs drop as automated systems create transparent digital records that auditors can quickly review. For most finance teams, automation can cut the monthly close process by up to 90% and free 15 to 20 hours of staff time per week.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)