%202.svg)

By Owen Hill, co-founder of KleerCard. Former Budget Director at Compassion International. Founded Switch Consulting, a fractional CFO practice for nonprofits.

The short answer

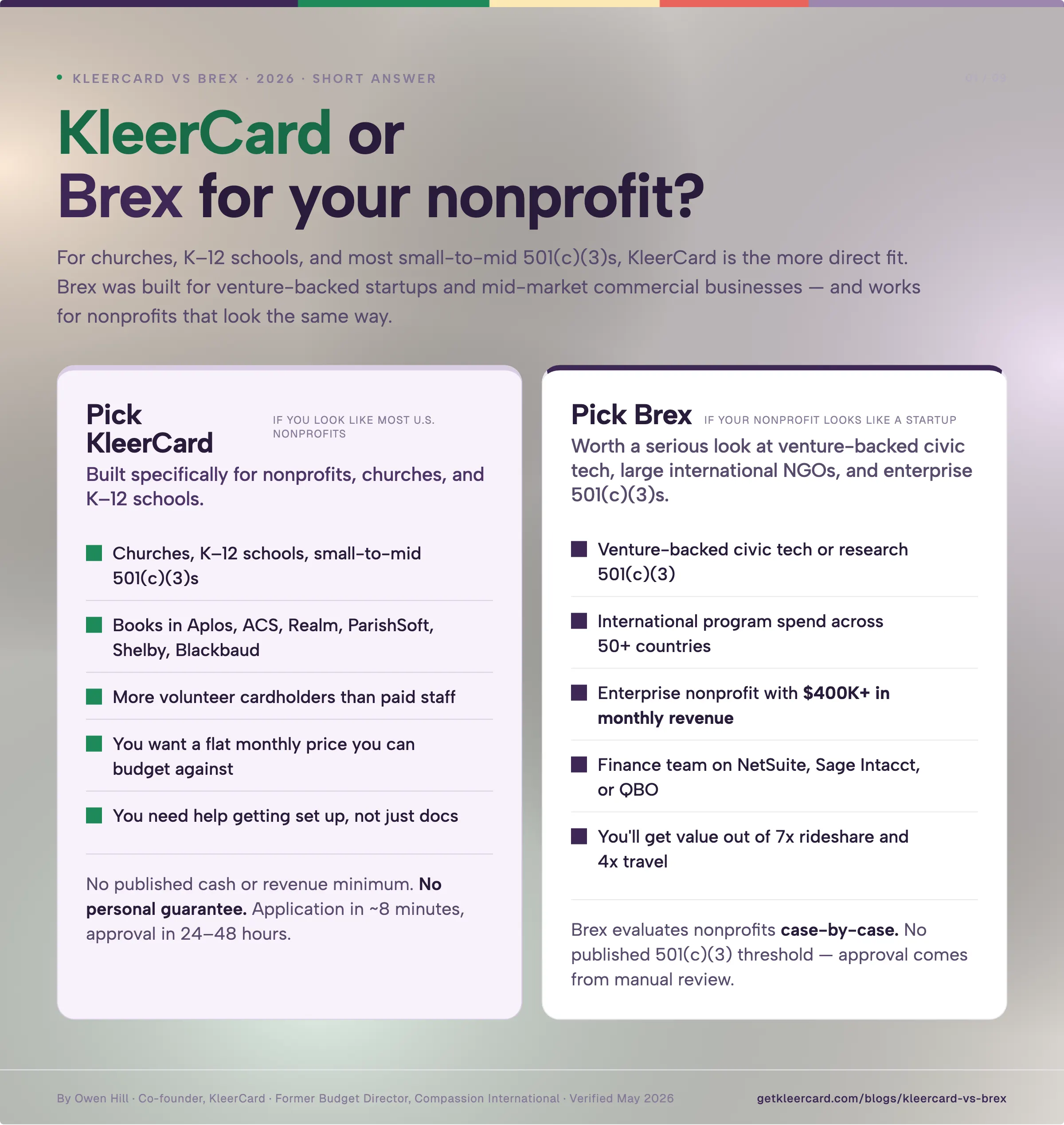

For churches, K-12 schools, and most small-to-mid 501(c)(3) nonprofits, KleerCard is the more direct fit. Brex was built for venture-backed startups and mid-market commercial businesses.

Brex's own help center says they evaluate nonprofits on a case-by-case basis. Most readers of this comparison will not clear Brex's published thresholds, and the workflows after approval were designed around SaaS revenue patterns rather than donor or grant cycles.

For venture-backed civic-tech 501(c)(3)s, large foundations with international program spend, or enterprise nonprofits with $400,000+ in monthly revenue, Brex is worth a serious look. The credit limits are higher, the travel and rideshare rewards are real, and the global card issuance covers 50+ countries.

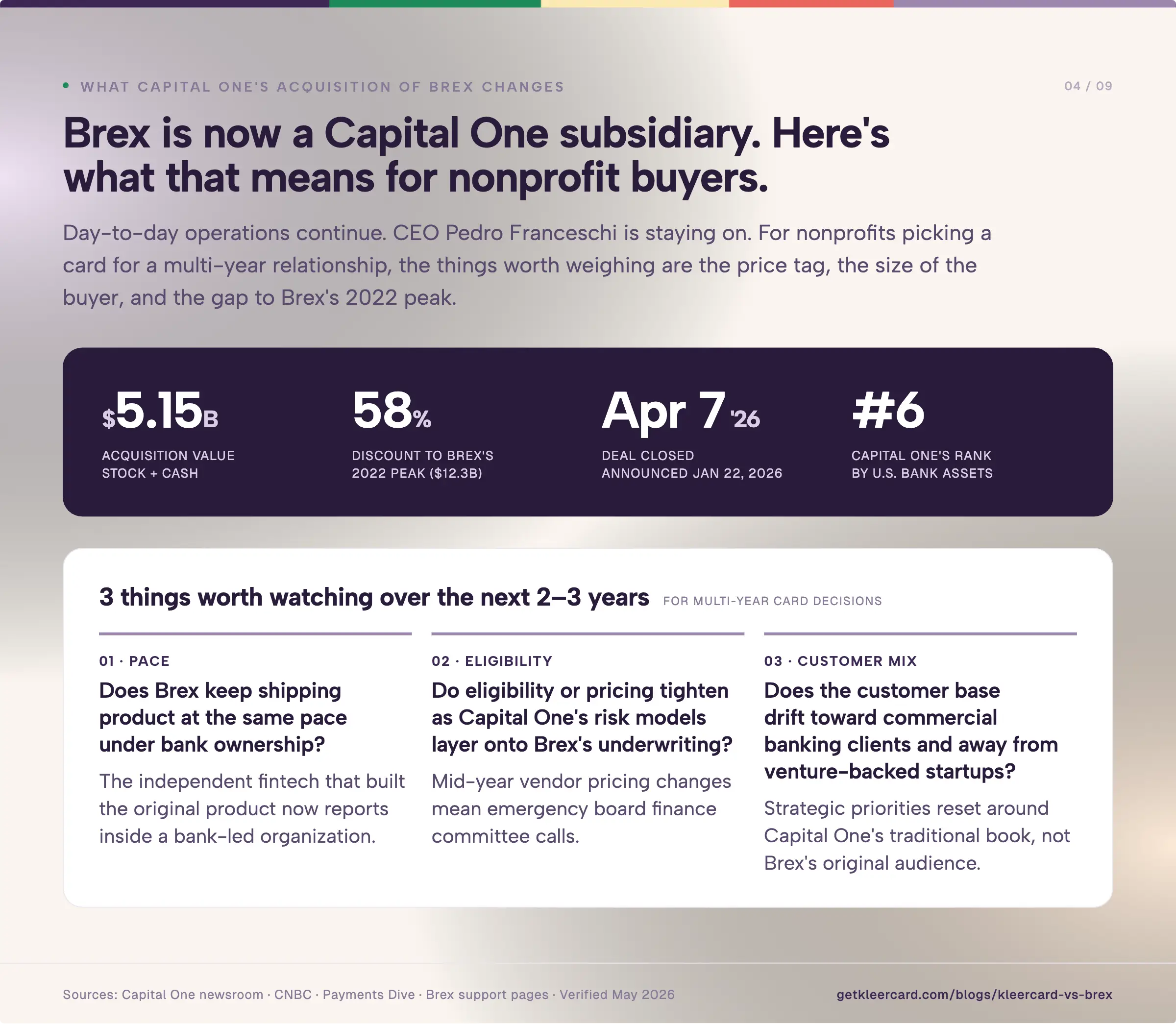

Capital One closed its $5.15 billion acquisition of Brex on April 7, 2026. For nonprofits picking a corporate card for a multi-year relationship, that's worth weighing, and the section below covers what to look at.

A disclosure up front: I co-founded KleerCard after running Switch Consulting (a fractional CFO practice for nonprofits) and serving as Budget Director at Compassion International. KleerCard now supports more than 1,000 organizations. I've written this comparison to be useful for people running nonprofits, including the situations where Brex is the better choice. Pricing and eligibility data reflect each vendor's published material as of May 2026 and change often. Please verify before applying.

KleerCard vs Brex at a glance

Why Brex usually doesn't approve smaller nonprofits

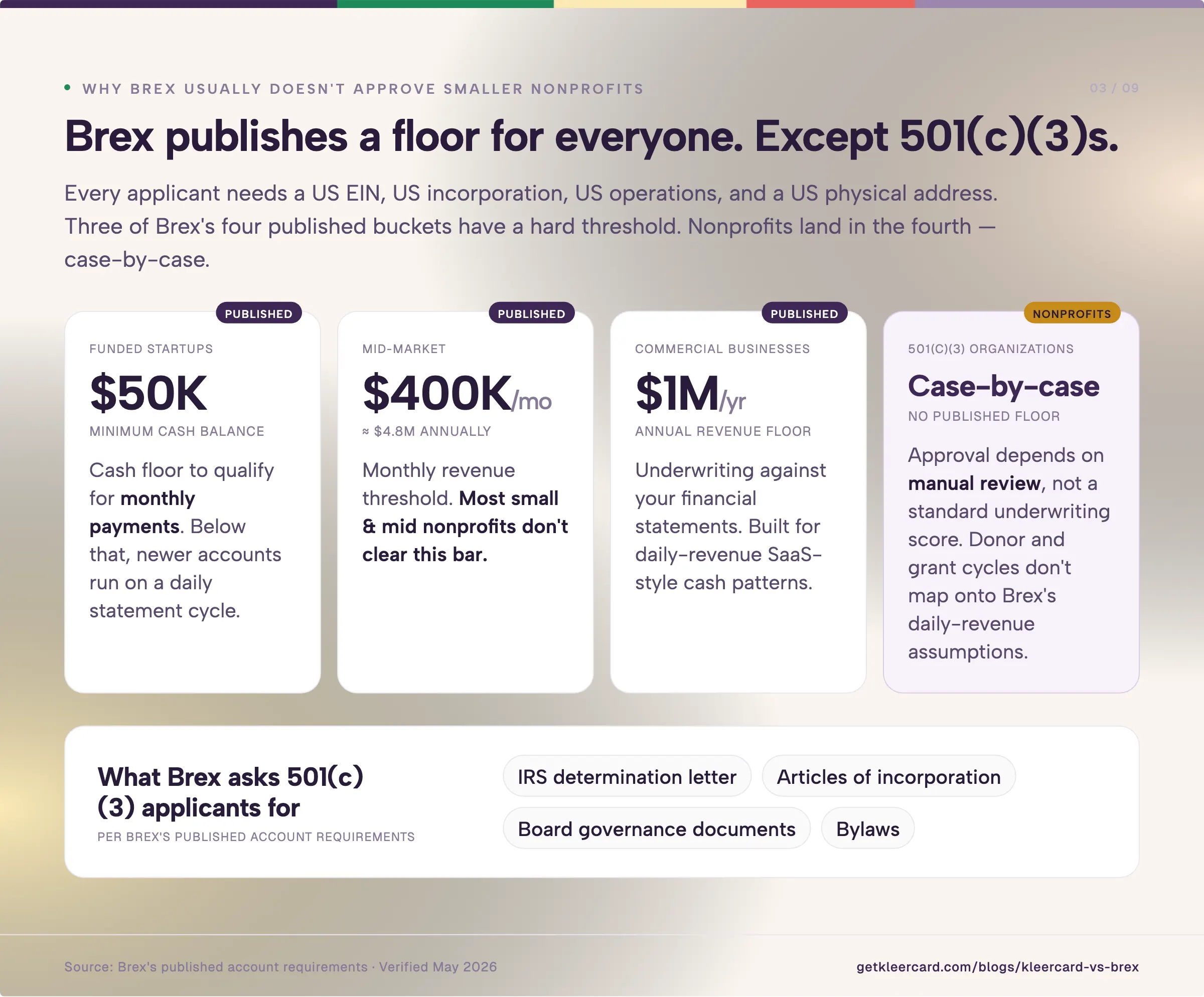

Brex requires every applicant to be a US-incorporated entity with an EIN, US operations, and a US physical address. Beyond that, Brex's published thresholds come into play:

- Funded startups: $50,000 minimum cash balance to qualify for monthly payments

- Mid-market companies: more than $400,000 in monthly revenue (about $4.8M annual)

- Commercial businesses: more than $1 million in annual revenue

- Nonprofits: "We work with nonprofits on a case-by-case basis"

If you apply as a 501(c)(3), Brex will ask for your determination letter, articles of incorporation, board governance documents, and bylaws. Approval depends on manual review, not a standard underwriting score.

Some nonprofits clear this without trouble. A church with $1M in annual giving has the cash on hand. A 24-campus school district has the budget. A national 501(c)(3) running grants has the revenue. For organizations at that size, eligibility is rarely the blocker.

Timing is harder. Donor and grant cycles operate monthly or quarterly. Brex's underwriting model was built around the daily revenue patterns of SaaS businesses, where credit limits adjust with cash balances and payments run on a daily statement cycle until you graduate to monthly. For an organization whose biggest deposit each quarter is a single foundation check, that workflow creates friction.

What Capital One's acquisition of Brex changes for nonprofit buyers

Capital One announced the Brex deal on January 22, 2026 and closed it on April 7, 2026. The transaction was valued at $5.15 billion in stock and cash, a 58% discount to Brex's 2022 peak valuation of $12.3 billion. Brex CEO Pedro Franceschi is staying on, and day-to-day operations are continuing as before. Brex's support pages now identify the company as a wholly owned subsidiary of Capital One, N.A.

The longer-term direction is the open question. Capital One is the sixth-largest U.S. bank by assets, and Brex's roadmap, pricing, and underwriting decisions now sit inside a bank-led organization with different priorities than the independent fintech that built the original product. Three things are worth watching:

- Whether Brex keeps shipping product at the same pace under bank ownership

- Whether eligibility or pricing tightens as Capital One's risk models layer onto Brex's underwriting

- Whether the customer base drifts toward Capital One's traditional commercial banking clients and away from venture-backed startups

For an organization picking a corporate card for a multi-year relationship, this is worth a few minutes of thought. Nonprofit boards set budgets twelve months out, and a mid-year vendor pricing change can mean an emergency board finance committee call to figure out where the money comes from.

When Brex is the right choice

Three nonprofit profiles where Brex makes sense.

The venture-backed civic tech or research 501(c)(3). Foundations have started funding nonprofit organizations that look operationally like SaaS companies: civic tech tools, open-source research initiatives, climate data platforms. These groups have institutional funding rounds, technical founders, software-heavy spending, and finance teams comfortable with QuickBooks Online or Sage Intacct. Brex's underwriting was built for them. The free Essentials tier handles the basics, and the 7x rideshare and 4x travel multipliers add up for a team that travels for conferences and meetings with funders.

The large international 501(c)(3) with global program spend. Brex issues local-currency cards in 50+ countries, with no foreign transaction fees. For an international relief organization running field offices across continents, that infrastructure matters more than fund accounting depth on the U.S. ledger. Most large international NGOs run NetSuite or Sage Intacct as their general ledger anyway, and Brex integrates with both.

The enterprise nonprofit with $400K+ in monthly revenue. Hospital foundations, research universities, and large national 501(c)(3)s with grants and earned-revenue lines clear Brex's published mid-market threshold. The case-by-case nonprofit review path opens up faster at this size. The product also offers tools that smaller cards, KleerCard included, don't ship: deeper treasury features, higher credit limits, integrated global payments, and a procurement-grade approval engine.

When KleerCard is the right choice

Three profiles where KleerCard is the more direct fit.

The church running fund accounting. If your books live in Aplos, ACS Technologies, Realm, ParishSoft, ChurchTrac, Shelby, PowerChurch, or Blackbaud, KleerCard is the only corporate card platform I'm aware of that integrates natively with those systems.

Transactions tag to the right fund (general, missions, building, benevolence, designated giving, capital campaign) at the point of purchase, not at month-end. A youth pastor swiping a card at Walmart for VBS supplies has the transaction code to the VBS line item the same minute it clears the swipe. Nobody in the finance office is recoding it later.

The full set of integrations is on the KleerCard integrations page, and our guide to the best accounting software for churches walks through how the underlying fund structure in each platform shapes the card workflow.

The K-12 school or multi-campus district. Schools share the fund-accounting and volunteer-card needs churches have, plus seasonal staffing spikes: summer interns, six-week class instructors, field trip leaders, athletic coaches managing tournament travel.

On Brex's per-user-priced Premium tier, that turns into a budget surprise every August. KleerCard's flat $29 or $49 monthly price is based on ranges of users, so the price doesn't change when you add a couple cardholders for a season.

One KleerCard customer consolidated AP across 24 campuses onto one platform, and we have a use-case breakdown of how multi-campus church expense management works if your structure looks similar.

The small-to-mid 501(c)(3) with volunteer cardholders. Brex requires cadholders to have organizational email addresses. So if you have volunteers using their personal Gmail accounts, you’ll have to create emails for them.

KleerCard does not have that requirement. You can add your volunteers with their personal email addresses.

KleerCard runs onboarding through 2 to 3 thirty-minute Zoom calls with a dedicated implementation lead; Brex's onboarding is largely self-serve.

Two customer numbers, both public on the KleerCard site. Emily, an HR & Finance Director at a nonprofit, moved from 40 hours per month of receipt collection and expense coding to 1 hour in her first month on KleerCard. Jared, an Executive Pastor, reports month-end close dropped from 3 days to 7 minutes after switching.

KleerCard isn't a corporate card for venture-backed SaaS companies, international foundations running treasury in 20 currencies, or enterprise nonprofits that need a procure-to-pay automation engine. Brex or Ramp covers that work better than we do.

Feature-by-feature comparison

Eligibility and approval

Brex publishes specific thresholds and reviews nonprofits case-by-case. A church with $1M in annual giving may qualify after a manual review that requires articles of incorporation, board governance documents, IRS determination, and bylaws. A human at Brex makes the decision, on a timeline that depends on the queue. Brex does not perform a personal credit check or require a personal guarantee; evaluation is based on the organization's financial profile, per NerdWallet's coverage.

KleerCard does not publish a cash or revenue minimum. The application takes about eight minutes online and asks for an EIN letter, bank information, and ID verification on one signer. Approval typically lands within 24 to 48 hours. No personal guarantee. The card is issued by The Bancorp Bank, N.A. on the Visa Commercial network, with SOC 2 and PCI DSS compliance.

Pricing and predictability

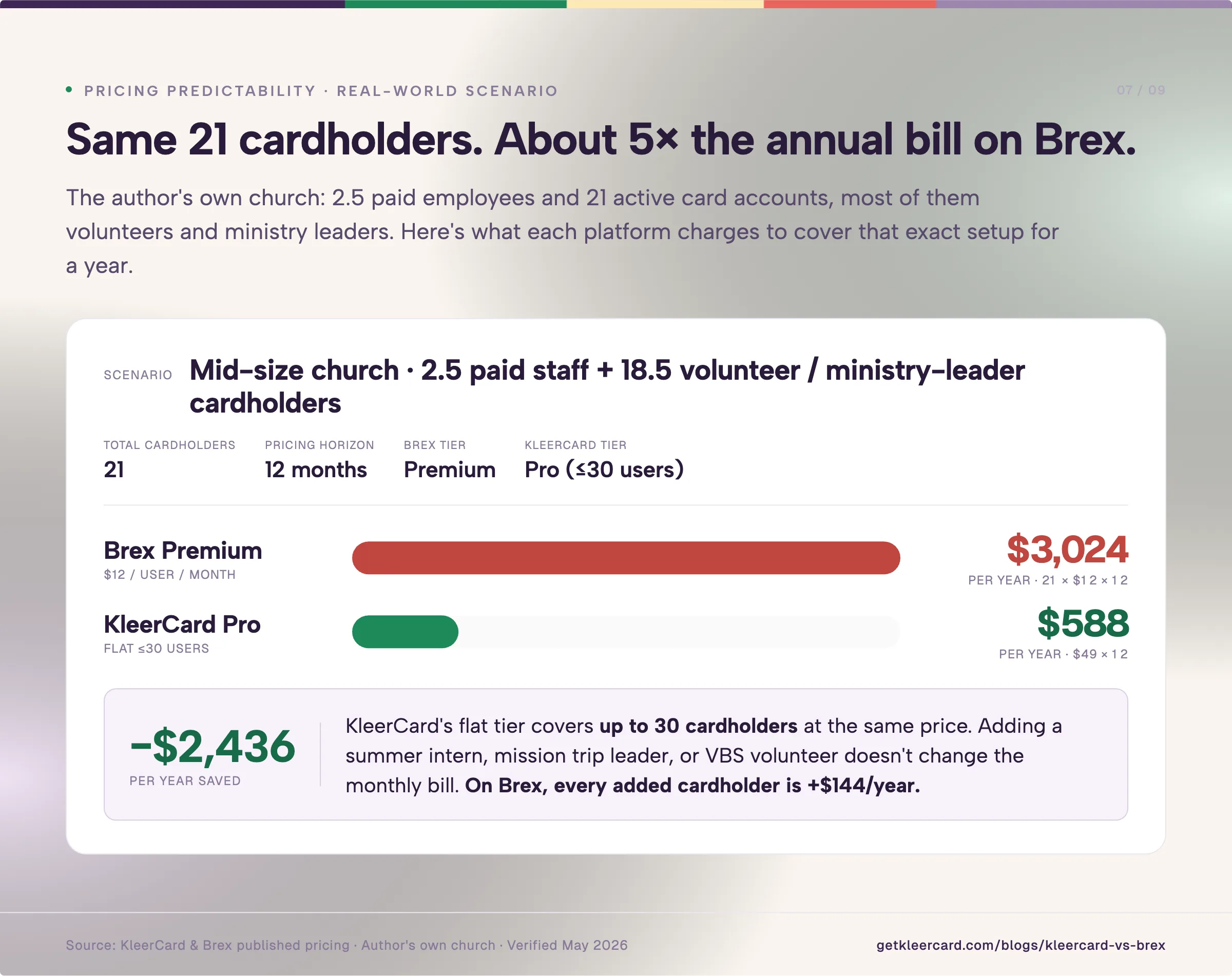

Brex's Essentials tier is free for qualifying companies. Premium runs $12 per user per month. Enterprise is custom. For a nonprofit with 20 active cardholders on Premium, that's $240 per month, or $2,880 per year. Add seasonal users (summer interns, mission trip leaders, VBS staff) and the per-user costs compound.

KleerCard charges flat tiered pricing on the KleerCard pricing page: $0 for up to 5 users, $29/month for up to 15, $49/month for up to 30. Above 30 users, pricing is custom. There's no per-seat scaling inside a tier. Adding a six-week class instructor or a summer camp volunteer doesn't change the monthly bill.

For a concrete example, my own church runs 2.5 paid employees and 21 active KleerCard accounts, most of them volunteers and ministry leaders. On Brex Premium at $12 per user per month, those 21 accounts would cost about $3,024 per year. KleerCard's Pro tier covers the same setup for $588 per year. For organizations with more volunteer cardholders than paid staff, the ratio gets wider.

Fund accounting and integrations

This is where the two products differ most. Brex syncs with QuickBooks Online, NetSuite, Sage Intacct, and Xero. For commercial businesses and tech-adjacent nonprofits running those systems, the integration depth is real.

For churches and nonprofits running fund-specific accounting, Brex doesn't ship native integrations with Aplos, ACS Technologies, Realm, ParishSoft, ChurchTrac, Shelby, PowerChurch, or Blackbaud Financial Edge NXT. The workaround is monthly CSV export and reformatting by hand, often with offsetting double-entry rows to satisfy fund accounting structures. That's usually the work people adopted a card platform to get away from.

Tricia G., a finance office lead at a church KleerCard onboarded this spring, described 4 to 6 hours per month of manual data entry into ACS Financials before she moved to KleerCard and was able to use the native integration. She described the total monthly impact across reconciliation, coding, and ACS entry as "days of her time each month."

Spend controls and card programs

Both products offer virtual cards, merchant category restrictions, and per-card spend limits. Brex's controls were designed for commercial spend categories: travel policies, software subscriptions, vendor agreements. KleerCard's were built around scenarios churches and schools run into:

- Single-use virtual cards for a one-day field trip

- Time restrictions

- Refilling stipend cards for teachers' classroom budgets that don't roll over

A KleerCard card capped at $250 will decline at $251. An auto-lock feature pulls a card offline if the receipt isn't uploaded within a set window, which moves the receipt-chasing work off the finance team's desk and back onto the user.

Rewards and cashback

Brex's rewards are weighted toward commercial spend categories: 7 points per dollar on rideshare, 4 points per dollar on travel booked through the Brex portal, 3 points per dollar on restaurants, 2 points per dollar on recurring software subscriptions, 1 point on everything else, per NerdWallet's review. For a startup with high rideshare and SaaS spend, those multipliers add up. Brex also offers partner discounts with AWS, WeWork, Google Ads, and Salesforce.

KleerCard does not offer cashback on standard plans. Organizations spending over $30,000 per month on cards can get custom pricing that includes cashback. For most churches and schools, the per-card spending limits and merchant category controls cover more ground than 1% back would.

Cashback is also harder for nonprofits than it sounds. The rebate can't legally benefit a single person at the organization, so a 501(c)(3) finance team has to decide whether the credit goes to the missions fund, the building fund, the general fund, or gets allocated across departments. For organizations spending $30K+ per month on cards where the rewards become meaningful, that allocation question is worth discussing with your bookkeeper before you sign up for either platform.

Payment terms and float

Brex is a corporate charge card. The balance is paid in full each cycle, with payments running daily for newer accounts and monthly for established ones. There's no interest, and you can't carry a balance.

KleerCard runs on a net-7 cycle, with payment due weekly.

For organizations whose grants pay 30 or 60 days after invoicing, neither product covers that float. An SBA loan, a commercial line of credit, or a traditional business credit card with revolving terms is the right tool there.

I had a version of this conversation last month with Raymond at the Beyond Educating Foundation. His organization needed to bridge net-30 and net-60 government and partnership contracts. KleerCard wasn't the right fit, and we said so. He's working with a commercial bank on it.

Real-world examples by organization profile

Small church on a fixed budget. A 250-person church with $400K in annual giving and 4 cardholders. KleerCard at $29/month is the easier match. Brex would route this into case-by-case review and might decline based on the cash threshold. Even if approved, integrating with the church's accounting software would be a manual CSV process.

Mid-size multi-ministry church. A 1,500-member church with multiple ministry departments, 12 to 20 cardholders, and a finance manager spending half a day a month on credit card reconciliation. The Aplos or Shelby integration is the deciding factor. KleerCard at $49/month covers up to 30 users with the integration built in. Brex would likely approve at this revenue level, but the church would still be hand-mapping transactions to funds at month-end.

Large national 501(c)(3) with international program spend. A national relief organization with $50M in revenue, NetSuite as the ledger, field offices in 6 countries, and a finance team of 8. Brex's global card issuance, NetSuite integration, and credit limit ceilings make it a real candidate. KleerCard's fund accounting depth matters less at this scale because NetSuite handles the fund structure natively. The Capital One acquisition is worth a board-level conversation before signing a multi-year agreement.

K-12 private school with seasonal staffing. A 300-student private school with 8 teachers, a part-time business manager, and 4 to 6 athletic coaches who run tournament travel during competition seasons. The seasonal user pattern decides it. Brex Premium's $12/user/month means $96 to $168/month during peak season. KleerCard's $49 Pro tier covers up to 30 users.

How to switch from Brex to KleerCard

Across the small-to-mid nonprofits and churches KleerCard has onboarded, a typical switch follows six steps:

- Application: about 8 minutes online. EIN letter, bank info, ID verification on one signer.

- Approval: 24 to 48 hours. No personal guarantee, and no personal credit check on cardholders.

- Onboarding meetings: two to three thirty-minute Zoom calls with a dedicated implementation lead for smaller organizations, three or four calls over three to four weeks for larger or multi-campus setups. More on what's included in KleerCard's white-glove setup.

- Physical card shipment: 5 to 8 days via USPS. Virtual cards available immediately on approval.

- Pilot rollout: one billing cycle with 2 to 5 cardholders, usually the people most comfortable testing a new tool. I recommend this cadence on most demos because it surfaces edge cases before the full team transition.

- Full team rollout: next billing cycle.

The Brex-to-KleerCard is mostly seamless with one wrinkle. Brex's daily/monthly statement payment cycle differs from KleerCard's weekly cycle, and the cash flow timing shifts when you switch. If your organization is on Brex's monthly cycle and you're moving to KleerCard's net-7, plan for one transition week where the books need to reflect both old and new payment timing. Your bookkeeper will need 20 minutes to map the differences.

FAQ

Does Brex accept nonprofits?

Yes, on a case-by-case basis. Per Brex's published documentation, 501(c)(3) applicants are asked for board governance documents, articles of incorporation, IRS determination letter, and bylaws. Approval depends on manual review rather than a standard underwriting score, and the underlying credit model favors organizations with cash balances and revenue patterns that resemble venture-backed startups or mid-market commercial businesses.

Does KleerCard accept nonprofits?

Yes. KleerCard was built for 501(c)(3) nonprofits, churches, and K-12 schools as the primary audience. There's no published cash balance or revenue minimum, and no personal guarantee. The application takes about 8 minutes and approval typically lands in 24 to 48 hours.

What does Capital One's acquisition of Brex mean for current Brex customers?

Capital One closed the $5.15 billion acquisition on April 7, 2026. Brex CEO Pedro Franceschi is staying on, and Capital One has said pricing, products, and support are unchanged for now. For nonprofits picking a corporate card for a multi-year relationship, the things worth watching are eligibility tightening, pricing changes at renewal, and shifts in customer focus toward Capital One's traditional commercial banking clients.

Why doesn't KleerCard offer the same cashback as Brex?

KleerCard does not offer cashback on standard plans. Organizations spending over $30,000 per month on cards can get custom pricing that includes cashback. For most churches and schools, the per-card spending limits and merchant category controls cover more ground than 1 to 1.5% back would. Cashback also creates a tax allocation question at 501(c)(3) organizations that can outweigh the dollar value.

Does Brex integrate with church accounting software?

No. Brex syncs with QuickBooks Online, NetSuite, Sage Intacct, and Xero. There are no native integrations with Aplos, ACS Technologies, Realm, ParishSoft, ChurchTrac, Shelby, PowerChurch, or Blackbaud Financial Edge NXT. Most church accounting platforms require custom CSV exports, sometimes with offsetting double-entry rows, which Brex does not ship by default. KleerCard built native integrations with each of those platforms because that workflow is the main reason churches consider switching cards.

Can a volunteer or board member with a personal email get a Brex card?

Brex's onboarding flow expects organizational email addresses. For nonprofits with volunteer cardholders, summer mission trip leaders, or board treasurers on personal Gmail or Outlook accounts, that's a workaround rather than a supported workflow. KleerCard supports personal-email cardholders without the extra setup, which matters for the roughly half of small church cardholders who don't have an organizational email.

Is KleerCard the right corporate card for venture-backed nonprofits or international NGOs?

Not usually. KleerCard was built for nonprofits, churches, and schools running fund accounting with U.S. operations. If your organization is venture-funded with SaaS-like revenue patterns, runs treasury operations in multiple currencies, or needs international card issuance across 50+ countries, Brex is a more direct fit. The same goes for nonprofits with $400,000+ in monthly revenue running NetSuite or Sage Intacct as the general ledger.

How does Brex compare to Ramp for nonprofits?

Both were built for commercial businesses, and both have nonprofit eligibility floors that screen out most small-to-mid 501(c)(3)s. Ramp's threshold is lower ($25,000 in a connected business bank account), and Ramp does not currently require case-by-case review for nonprofits. Brex's per-category rewards are higher, particularly for travel and rideshare. For a full head-to-head, see the Ramp vs Brex comparison.

How to decide

A short decision tree, based on the patterns above.

- Do you have less than $25,000 in a US business bank account? Neither Brex nor Ramp will approve you on standard terms. Look at KleerCard, Charity Charge, or a traditional small-business credit card.

- Are you a church, K-12 school, or small-to-mid nonprofit running fund accounting? KleerCard is built for that specific workflow. The signup takes about five minutes; you can start the application here.

- Are you a venture-backed civic tech 501(c)(3), large international NGO, or enterprise nonprofit with $400K+ in monthly revenue? Apply to Brex directly. Ask the onboarding team about current nonprofit underwriting and any commitments around grandfathering of existing terms.

- Still weighing options? The best credit cards for nonprofits guide covers seven options including both KleerCard and Brex. The Brex alternatives piece covers what to look at if Brex isn't the right answer for your organization. If a different card on either list is a better match, I hope this guide helped you figure that out.

Owen Hill is co-founder of KleerCard, a corporate card built for nonprofits, churches, and schools. Owen holds a degree in Economics and Operations Research from the United States Air Force Academy and a Ph.D. in Economics. He served as a Financial Analyst in the U.S. Air Force, then as Budget Director at Compassion International, where he managed program budgets across dozens of country offices. Before KleerCard, he founded Switch Consulting, a fractional CFO practice for nonprofits. KleerCard is reviewed alongside other corporate cards throughout this article.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)