%202.svg)

The short answer

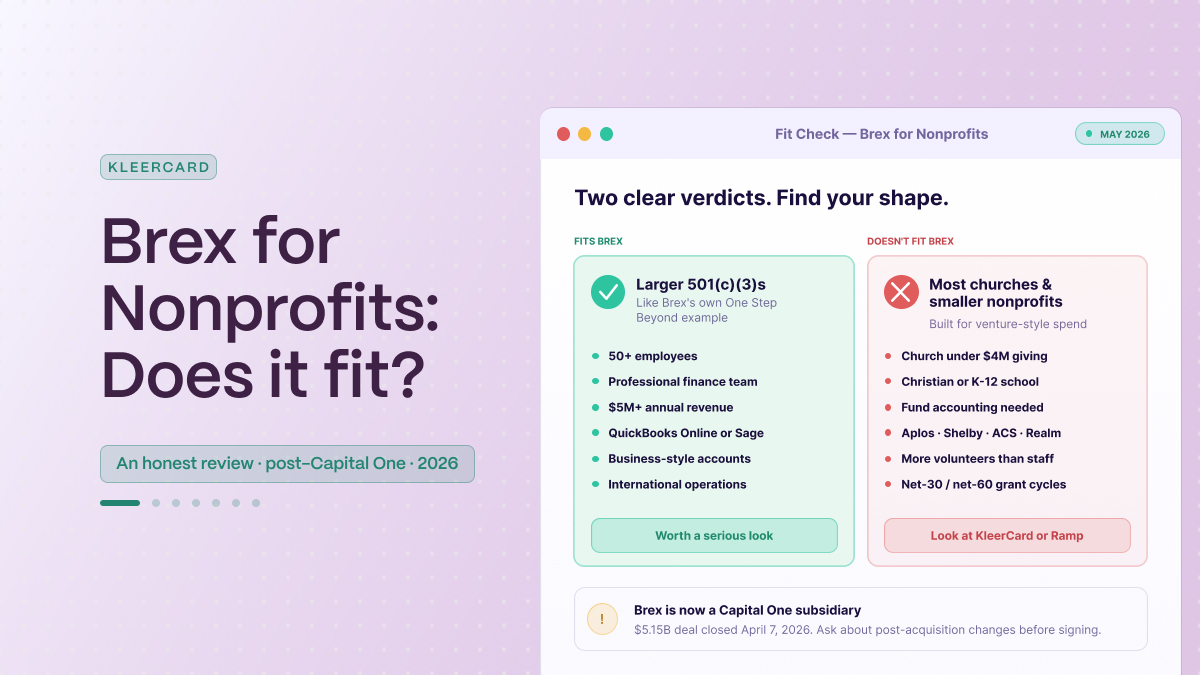

Brex works with nonprofits on a case-by-case basis, per its own published policy. The 501(c)(3)s Brex tends to approve look a lot like the for-profit companies Brex approves: significant cash reserves, a professional finance team, a business-style chart of accounts, and 50 or more employees.

The example Brex itself publishes is One Step Beyond, an Arizona nonprofit with about 300 employees and 80 cardholders.

If your nonprofit fits that profile, Brex is worth a serious look.

If you're a church under $4M in annual giving, a Christian or independent K-12 school, a small-to-mid nonprofit running fund accounting on Aplos, ACS, Shelby, ParishSoft, Realm, or Blackbaud, or any organization with more volunteer cardholders than paid staff, Brex's eligibility floor, per-user pricing, and accounting integrations are not as good of a fit.

Capital One closed its $5.15 billion acquisition of Brex on April 7, 2026. If you're choosing a card platform for a multi-year relationship, the acquisition belongs on the list of things to think about as it’s likely that some things will change.

Quick comparison: Brex vs. Ramp vs. KleerCard

I'm a co-founder of KleerCard, so I want to be upfront about that. I've included KleerCard in this comparison because it's a real option for the audience this article is for (nonprofits, churches, and schools), and I've tried to write about Brex the way I'd write about any other competitor.

Where Brex is the better choice, I'll say so. Before KleerCard, I spent a few years as Budget Director at Compassion International and ran Switch Consulting, a fractional CFO practice for nonprofits, so I know what these decisions look like from the buyer's side of the table.

What Brex is

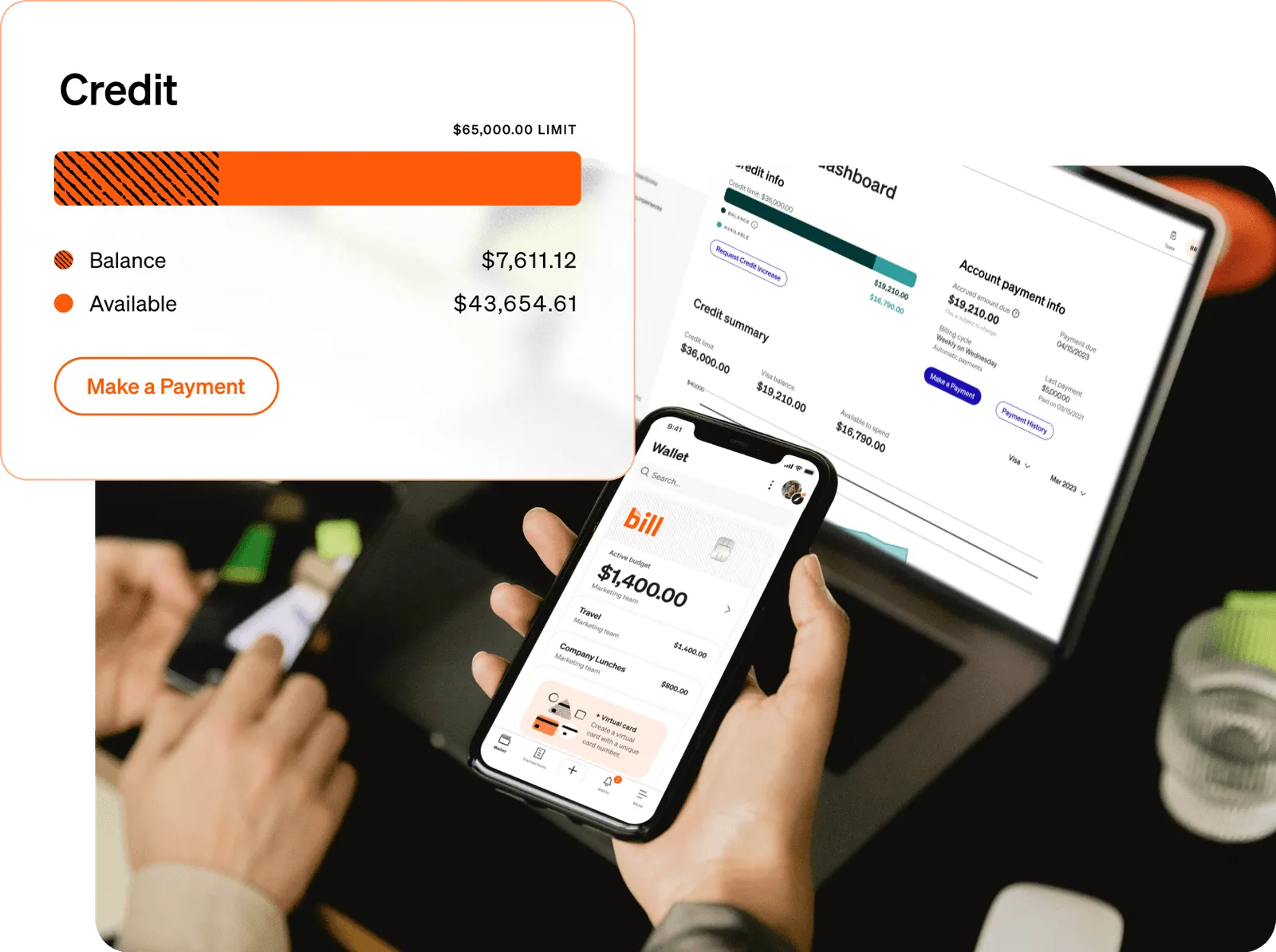

Brex is a corporate charge card and spend management platform. The product combines card issuance, real-time policy enforcement, AI-driven receipt matching and GL coding, bill pay, reimbursements, and a business banking account in a single dashboard.

Brex was founded in 2017, served about 35,000 clients at the time of the Capital One acquisition close per American Banker, and now operates as a wholly owned subsidiary of Capital One, N.A.

Brex does not require a personal guarantee. Credit limits sit on the organization's cash balance, revenue, and funding profile, not on the personal credit of a board member or executive director.

The rest of the product carries assumptions from venture-backed software companies. Departmental budgets and cost centers, global card issuance across 50+ countries, ERP integrations with NetSuite and Sage Intacct, AI agents that automate finance work. Brex describes itself as an "AI-native software platform," and that orientation runs through the entire experience.

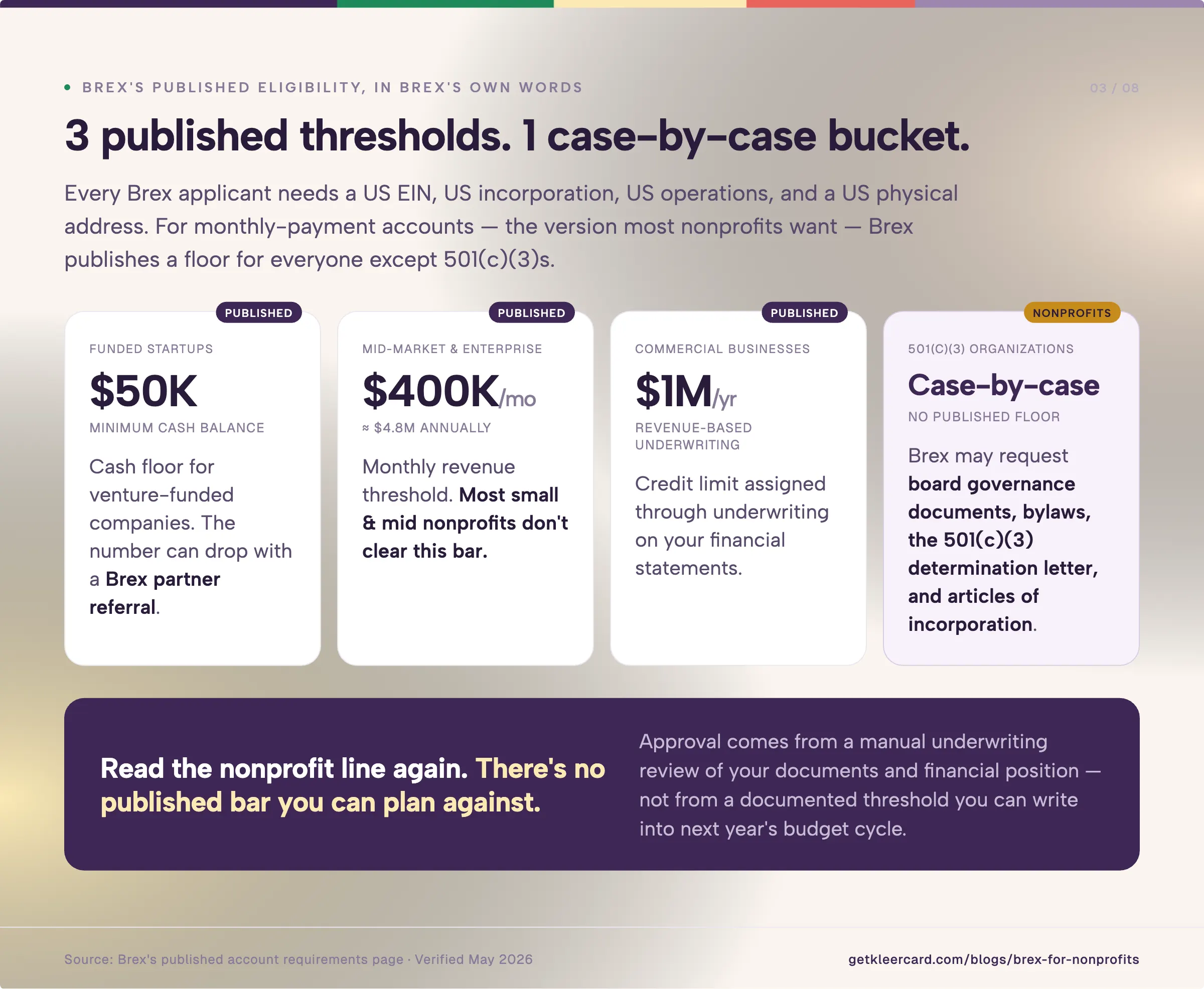

Brex's published eligibility, in Brex's own words

Brex's account requirements page lays out the thresholds. Every applicant needs a US EIN, a valid US incorporation, US operations, and a US physical address. From there, the thresholds for monthly-payment accounts (the version most nonprofits want, because credit limits flex with cash position rather than reset every day) are:

- Funded startups: $50,000 minimum cash balance if you've raised funding. The number can drop with a Brex partner referral.

- Mid-market and enterprise: more than $400,000 per month in revenue, which is about $4.8 million annually.

- Commercial businesses: more than $1 million in annual revenue, with credit limit assigned through revenue-based underwriting on your financial statements.

- Nonprofits: "We work with nonprofits on a case-by-case basis." Brex may request board governance documents, bylaws, your 501(c)(3) determination letter, and articles of incorporation as part of the application.

Read the nonprofit line again. There's no published cash balance or revenue floor for nonprofits. Approval comes from a manual underwriting review of your documents and financial position, not from a documented threshold you can plan against twelve months in advance.

A church with $1M in annual giving has the cash. A school district has the budget. A national 501(c)(3) running grant programs has the revenue. Timing is harder to plan for. Donor cycles, government grant disbursements, and tuition collections don't generate the daily revenue patterns Brex's underwriting model was built around.

Where Brex fits a nonprofit

The example Brex publishes is One Step Beyond, an Arizona-based 501(c)(3) supporting adults with disabilities. Per Brex's case study, One Step Beyond runs about 300 employees and 80 active cardholders. Their finance team was spending more than 100 hours a month processing expenses on Wells Fargo cards before the switch. After moving to Brex, that came down to 30 to 40 hours, and they added 40% more cardholders in the same window. CEO Madison Blanton describes the change as a productivity gain across the whole organization.

The profile to look for if you're a nonprofit considering Brex:

- Headcount around 50 and up, often well above. Brex's per-user pricing and product depth start to pay back at the scale where a controller is managing dozens of cardholders across programs.

- A professional finance team. Brex assumes a controller, a finance manager, or a fractional CFO who can run the platform. Implementation runs through self-serve documentation; white-glove onboarding is reserved for the largest enterprise accounts.

- A business-style chart of accounts. Departmental budgets and cost centers map to Brex's controls. Fund accounting structures (restricted funds, program-level reporting, grant tracking, donor designations) do not, and bridging them takes manual work or custom mapping.

- QuickBooks Online, NetSuite, or Sage Intacct on the accounting side. Brex's native accounting integrations were built for the general ledgers commercial businesses use.

- Cash reserves and a clean financial profile. Brex underwrites against your balance sheet. Nonprofits with strong reserves and predictable revenue tend to clear underwriting; nonprofits operating month-to-month tend to land in a long case-by-case review.

If your nonprofit looks like One Step Beyond, Brex works. The AI-driven receipt matching, GL coding, and policy enforcement are well-built, the no-personal-guarantee structure removes a meaningful liability for board members, and the global card capability is hard to match elsewhere.

Where Brex doesn't fit most nonprofits

Most nonprofits don't look like One Step Beyond. The IRS recognized 1.54 million 501(c)(3) organizations in fiscal year 2024, and the bulk of them are small. Most churches and K-12 schools also run small paid staff alongside large volunteer rosters. For that audience, four things come up over and over on the demo calls I have with clients and prospects.

Fund accounting platforms don't connect to Brex. Brex integrates with QuickBooks Online, NetSuite, Sage Intacct, Xero, and a handful of similar commercial general ledgers. It doesn't ship native integrations with Aplos, ACS Technologies, Shelby, Realm, ParishSoft, ChurchTrac, PowerChurch, or Blackbaud Financial Edge NXT.

For organizations on those systems, every Brex transaction lands in a CSV that someone reformats by hand, often with offsetting double-entry rows to satisfy fund structure. Tricia G., a finance lead at a church we onboarded off Concur this spring, told us she was spending 4 to 6 hours a month on manual ACS data entry after her reconciliation work was done. Brex doesn't change that pattern for fund-accounting nonprofits.

The eligibility math screens out most small and mid nonprofits. A church with $1M in annual giving, a Christian school with a $3M operating budget, a community food bank with $500K in revenue. None of them clear the $4.8M mid-market revenue threshold. They land in the case-by-case bucket and have to make the case with documents and a manual review, without a published bar to plan against. Some get approved. Many don't, or end up in a multi-week underwriting conversation that's hard to plan a fiscal year around.

Per-user pricing breaks down for volunteer-heavy organizations. Brex Premium runs $12 per user per month. A small church with 2 paid staff and 15 volunteer cardholders (worship pastor, youth pastor, missions coordinator, hospitality lead, building manager, summer interns) pays about $2,000 a year on Premium. The same church on KleerCard's $29 / month Standard plan pays $348 a year. The numbers are similar for schools issuing cards to department heads, athletic directors, club advisors, and field-trip teachers.

Organizational email requirements add friction with volunteers. Brex assumes each cardholder has an email on the organization's domain. Volunteer treasurers, mission trip leaders, and fall festival coordinators on personal Gmail have to be set up with custom organizational emails before they can be added as users. For organizations where a meaningful share of cardholders are volunteers, that's recurring administrative work that’s not needed on platforms that are specifically built for nonprofits.

What the Capital One acquisition changes

Capital One announced the Brex acquisition on January 22, 2026, and closed it on April 7, 2026, in a stock-and-cash transaction valued at $5.15 billion. Brex CEO Pedro Franceschi is staying on. Day-to-day operations are continuing. Brex's support pages now identify the company as a wholly owned subsidiary of Capital One, N.A.

What changes over the next two to three years is hard to forecast. Capital One is the sixth-largest US bank by assets and has committed nearly $1 billion to integration and retention over three years. Brex's roadmap, pricing, and underwriting decisions now sit inside a bank-led organization with different strategic priorities than the independent fintech that built the original product.

For a nonprofit, vendor stability matters. Annual budgets get set twelve months ahead. A mid-year pricing change from a card vendor can mean an emergency board conversation and a hole in the budget that has to come from somewhere.

Brex hasn't announced changes to pricing, eligibility, or the case-by-case nonprofit treatment as of May 2026. If you're signing for a multi-year relationship, this is worth a few minutes with your Brex onboarding rep before you sign anything.

What Brex costs

Brex's three published tiers, from its pricing page:

- Essentials: $0 per user per month. Card issuance, AI-powered policy rules, accounting integrations, real-time reporting, bill pay, reimbursements, and travel booking. Limited to one local card program and up to two entities.

- Premium: $12 per user per month. Adds customizable expense policies, dynamic approval chains, AI compliance audit detection, and advanced spend limit approvals.

- Enterprise: Custom. Multi-entity controls, advanced reporting, dedicated support.

For most nonprofits, Premium is the realistic tier if Brex is going to do more than basic card issuance. Essentials is positioned for early-stage startups; the deeper controls a nonprofit finance team uses (multiple expense policies, role-based exceptions, audit detection) sit behind Premium.

Brex also runs a separate Brex Business Account with daily payments for organizations that don't qualify for monthly billing. Daily payment removes the cash threshold but constrains the experience. Credit limits flex with the available cash balance every day, instead of functioning as a stable corporate card.

What Brex does well

AI-driven expense automation. Brex's receipt matching, GL coding, and policy enforcement work. The platform learns from your coding decisions and takes a lot of the manual chase off the finance team. For nonprofits with the transaction volume to feed it, the automation pays back.

No personal guarantee. Brex underwrites against the organization, not an individual. If your board treasurer or executive director has been personally backing the card program, that's a meaningful liability removal.

Global card capabilities. Brex issues cards in 50+ countries and supports 20+ currencies. For relief organizations, mission agencies, and international education programs, the global stack is hard to match.

Better fits for the nonprofits Brex doesn't serve well

If your nonprofit doesn't clear Brex's eligibility floor, runs fund accounting, has more volunteer cardholders than paid staff, or wants pricing predictability in a post-acquisition environment, three options are worth comparing.

KleerCard. We built KleerCard for 501(c)(3) nonprofits, churches, and K-12 schools specifically. No cash balance requirement. No personal guarantee. No per-user pricing. Native integrations with Aplos, ACS Technologies, Shelby, Realm, ParishSoft, ChurchTrac, PowerChurch, Blackbaud, plus QuickBooks Online, QuickBooks Desktop, and NetSuite.

Pricing is based on the number of users you have. All tiers get access to all features.

- Up to 5 users: free.

- 6-15 users: $29/month

- 16-30 users: $49/month

- 31+ users: custom pricing

KleerCard runs on a weekly billing cycle (net-7), which works for nonprofits that don't need to float receivables against net-30 or net-60 grant contracts. If your operation depends on that float, KleerCard isn't a fit. Commercial banking and an SBA line of credit are.

Ramp. Funded startups and mid-market businesses with stable cash flow. $25,000 minimum balance in a U.S. business checking account, lower than Brex's startup floor. Free base tier, with platform fees showing up at renewal for some customers. Ramp's independence is also a point in its favor now that Brex sits inside Capital One. For a nonprofit, the harder fit issues are the absence of native fund accounting integrations and the per-user math when card programs scale. See our Ramp Card review for the full walkthrough.

Charity Charge. Charity Charge has two products: the Nonprofit Business Card issued through Commerce Bank, and the Nonprofit Corporate Card issued through Fifth Third Bank via Corpay. Both are for 501(c)(3)s and both pay cashback to the nonprofit's mission. A reasonable fit if you want a nonprofit-branded card with cashback, books on QuickBooks Online, and no need for fund accounting integrations. Of the two products, the Nonprofit Corporate Card has more spend controls than the Nonprofit Business Card.

A wider comparison sits in our guide to credit cards for nonprofits with no personal guarantee.

So, is Brex right for your nonprofit?

If your nonprofit looks like One Step Beyond (300 employees, a professional finance team, a business-style chart of accounts, $5M+ in annual revenue, QuickBooks Online or Sage Intacct on the back end), Brex is worth a serious look. The product works, the no-personal-guarantee structure removes a real pain point, and Brex's own case study is honest about what the change felt like inside the organization.

If your nonprofit looks more like a church with $1M in annual giving, a school with a small business office, or a community 501(c)(3) running fund accounting on platforms Brex doesn't connect to then it’s not a great fit. KleerCard was custom-built for organizations like yours. You can open an account or see our pricing. If you’d prefer to go with another card on the list above, I hope this review helps you figure that out.

Frequently asked questions

Can a nonprofit get a Brex card?

Yes, on a case-by-case basis. Per Brex's published account requirements, a 501(c)(3) can apply and may be approved after submitting board governance documents, the 501(c)(3) determination letter, articles of incorporation, and bylaws. Approval rests on a manual underwriting review of those documents and the organization's financial position. Brex doesn't publish a nonprofit-specific cash balance or revenue threshold.

Does Brex require a personal guarantee for nonprofit applicants?

No. Brex underwrites against the organization's cash balance, revenue, and funding profile, not the personal credit of a board member or executive. The same rule applies to nonprofit and for-profit applicants alike.

How does the Capital One acquisition affect Brex's nonprofit customers?

Capital One closed the acquisition on April 7, 2026 and has committed nearly $1 billion to integration and retention over three years per American Banker. Brex CEO Pedro Franceschi is staying on, and Brex continues to operate under the Brex name. As of May 2026, Capital One hasn't announced changes to Brex's pricing, eligibility, or case-by-case nonprofit treatment. If you're signing on for a multi-year card decision, ask the Brex onboarding team about expected post-acquisition changes and any commitments around grandfathering existing terms before you sign.

Does Brex integrate with fund accounting platforms like Aplos, Shelby, or ACS?

No native integrations. Brex's accounting integrations cover QuickBooks Online, NetSuite, Sage Intacct, Xero, and similar commercial-side general ledgers. Nonprofits running fund accounting on Aplos, ACS Technologies, Shelby, Realm, ParishSoft, ChurchTrac, PowerChurch, or Blackbaud Financial Edge NXT have to export CSVs and handle custom formatting by hand, often with offsetting double-entry rows for fund structure.

What does Brex cost for a small nonprofit?

Brex Essentials is $0 per user per month and covers card issuance, accounting integrations, bill pay, and reimbursements. Brex Premium is $12 per user per month and adds customizable expense policies, dynamic approvals, and AI compliance audit detection. A nonprofit with 10 cardholders on Premium pays $1,440 a year. KleerCard's Standard tier covers up to 15 cardholders for $348 a year flat.

Is Brex a good fit for churches and Christian schools?

For most, no. Brex's per-user pricing assumes a stable corporate headcount, and its accounting integrations were built for commercial general ledgers. Most churches run small paid staffs with many volunteer cardholders, keep their books in Shelby, ACS, ParishSoft, Realm, ChurchTrac, PowerChurch, or Aplos, and need restricted-fund reporting that doesn't map onto Brex's commercial structure. A Christian or independent school with a $4.8M+ operating budget, a dedicated finance team, and QuickBooks Online or Sage Intacct on the back end can make Brex work. Most churches and smaller schools land elsewhere.

What documents does Brex ask nonprofit applicants to provide?

Per Brex's published guidance, nonprofit applicants may be asked for board of directors and governance documents, bylaws, the 501(c)(3) determination letter, and articles of incorporation. That's in addition to the standard Brex requirements: US EIN, US incorporation, US operations, and a verifiable US physical address.

How long does Brex's nonprofit approval take?

Brex doesn't publish a nonprofit-specific timeline. Standard Brex applications can clear in days when the financial profile fits the published thresholds. The case-by-case nonprofit review involves manual document review and can take longer. If you're on a tight migration timeline, ask Brex's onboarding team for a timeline commitment before you start the process.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)