%202.svg)

A corporate card is a credit card issued to the organization itself and underwritten on the organization's financials and operating history. It is not tied to any one person's personal credit.

Many organizations search for guidance using the term "how to choose a business credit card." For incorporated entities with an EIN, the mechanics are best understood through the corporate card lens.

Whether your team can get approved without putting an individual's credit on the line, whether the costs stay predictable when headcount or spending patterns shift, whether the controls actually prevent problems instead of just reporting them later, and whether the whole system closes cleanly into your accounting at month-end — those are the factors that actually matter.

Rewards sit well down the list for most mission-driven organizations.

I have worked with finance teams at churches, nonprofits, and schools for years, both in operational roles and in consulting. The same friction points show up again and again. This framework is the one I walk teams through when they are evaluating options. I will be direct about where different cards fit and where they do not, including KleerCard.

If another provider serves your situation better, use the same questions and choose it openly.

How to Choose a Business Credit Card for Churches, Nonprofits, and Schools

The brands and rewards offers change constantly. The underlying mechanics do not. Work through these seven questions in order. Most options drop out early.

- Does the card require a personal guarantee, and what happens when the person who signed leaves or the board rotates?

- Is the pricing model predictable when your team grows, shrinks, or adds seasonal help for summer programs and events?

- Do the spend controls match how your actual team spends, including volunteers and short-term event needs?

- Does the platform integrate directly with your fund accounting software without hours of manual CSV work every month?

- Do any rewards or cashback deliver real net value after fees and the challenge of allocating cashback across funds?

- Will the onboarding and support actually work for the volunteers and non-finance staff who will use the cards?

- Does the provider’s overall model fit how your mission-driven organization operates over multiple years?

Work through them in that sequence. Most of the market falls away before you reach rewards or brand names.

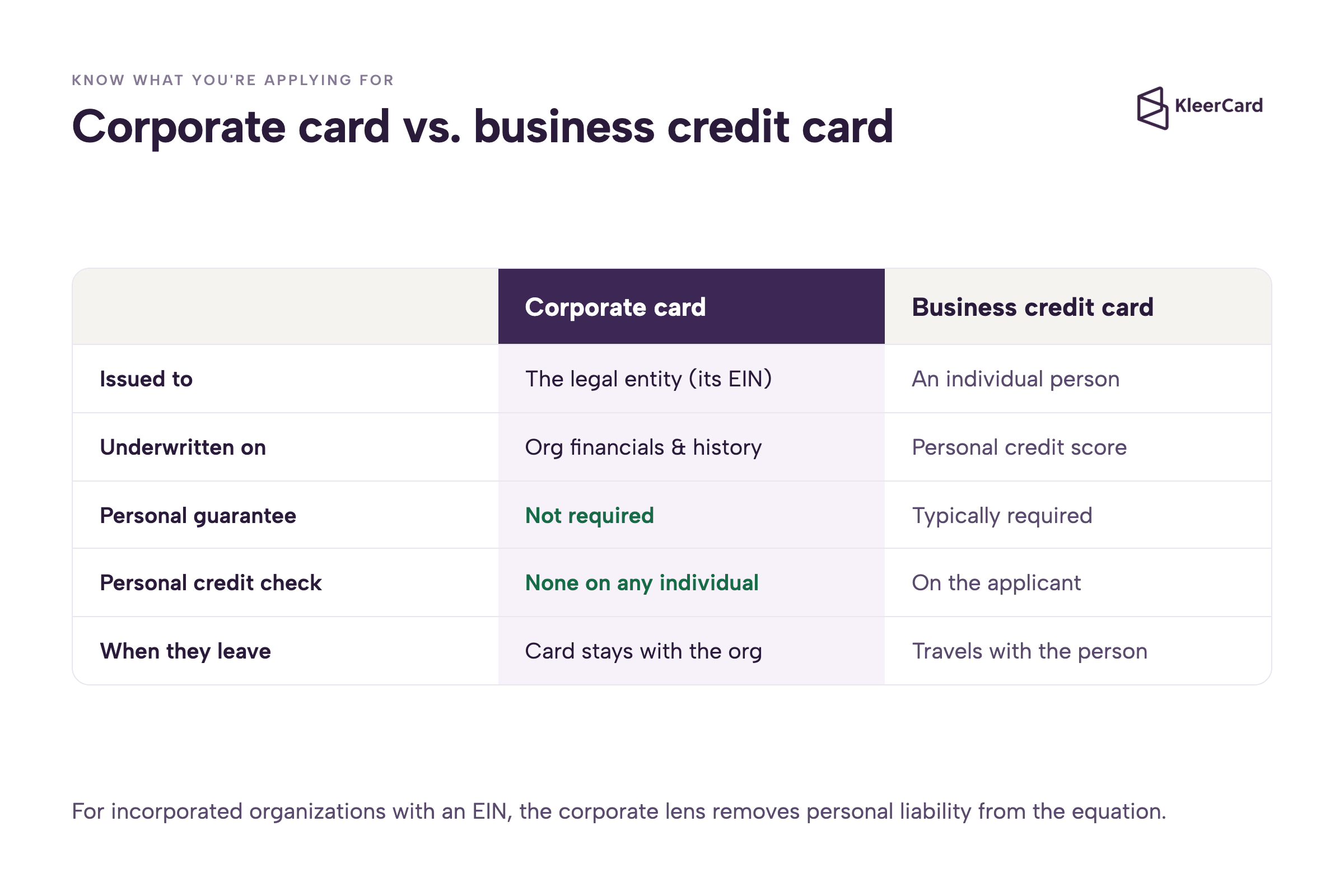

What a corporate card is, and how it differs from a business credit card

A corporate card is issued in the name of the legal entity. The organization applies with its EIN, bank account information, and financial history. Approval and the credit line rest on the organization's track record, not on any individual's personal credit score or willingness to sign a personal guarantee.

A business credit card is almost always tied to an individual. That person applies, their personal credit is checked, and they typically provide a personal guarantee. The card lives on their credit report and travels with them if they leave the organization.

Most incorporated organizations with an EIN and an established business bank account can access corporate card programs. Newer entities with little operating history may need to build some track record or start with a secured card before qualifying for an unsecured corporate line.

Eligibility: personal guarantee, credit checks, and who can get approved

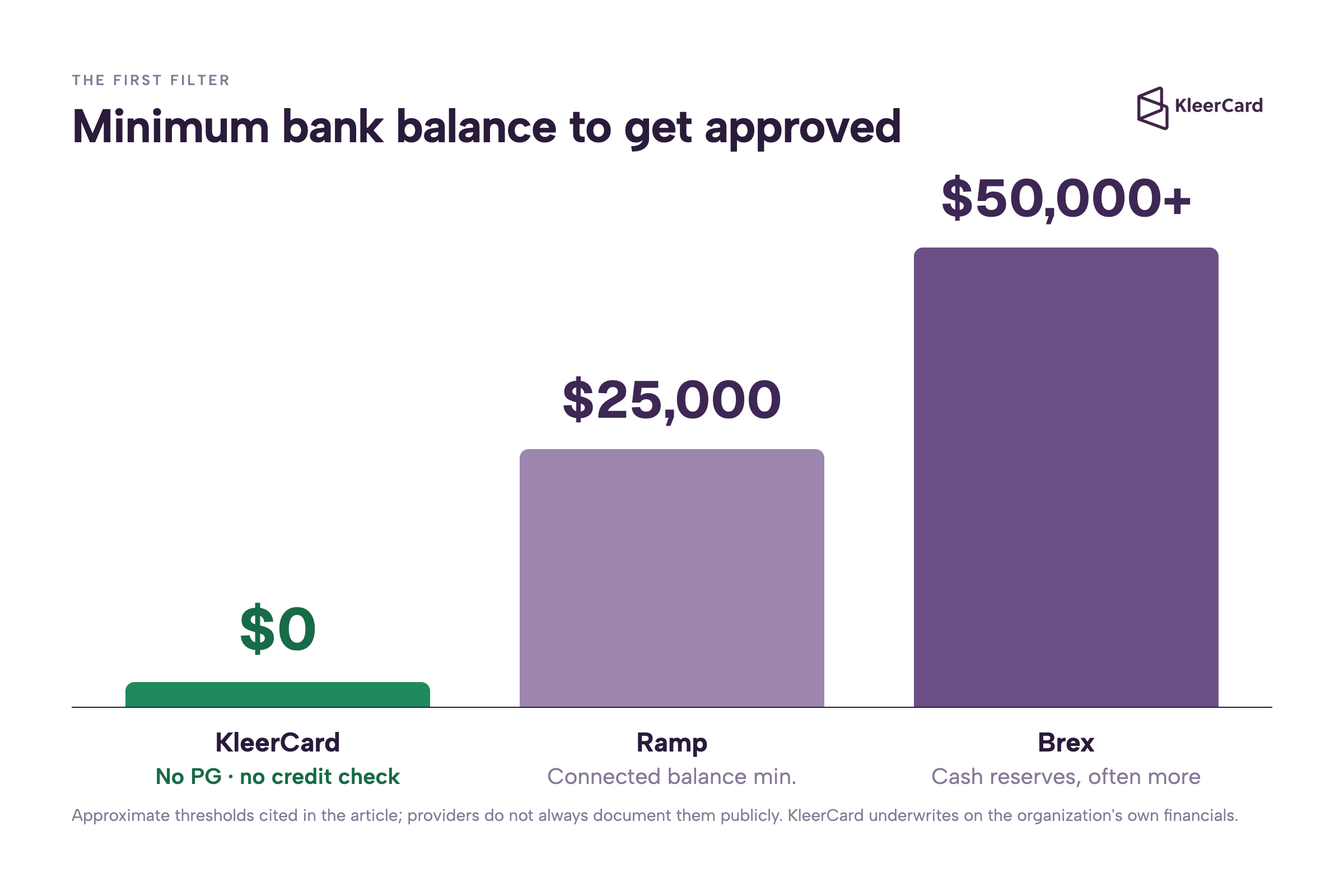

The first filter eliminates more options for churches, nonprofits, and schools than any other single factor.

Personal Guarantee Risks

A personal guarantee means an individual pledges their personal credit and assets if the organization cannot pay. When that person leaves, the organization often has to reapply or renegotiate the entire program. Cards tied to one person's credit also create awkward conversations when a new leader arrives and does not want to inherit someone else's personal liability.

KleerCard issues cards to the organization without a personal guarantee and without running a personal credit check on any individual at application. Approval rests on the organization's financial information and history.

Other programs set different gates. Ramp has published a requirement for a connected U.S. business bank account with a minimum balance, commonly cited around $25,000. For current details, see Ramp Card review. Brex has historically looked for substantial cash reserves in the connected accounts, often in the range of $50,000 or more depending on the applicant.

These thresholds are not always clearly documented on the provider's site, which adds friction when you are trying to evaluate options quickly. Brand-new organizations with no EIN history, no bank account track record, or very limited operating time may still need a secured card or a traditional business card with a personal guarantee to get started.

Once the entity has some history, the door to true corporate cards opens. For a deeper look at the personal guarantee issue specifically for nonprofits and churches, see credit cards for nonprofits with no personal guarantee.

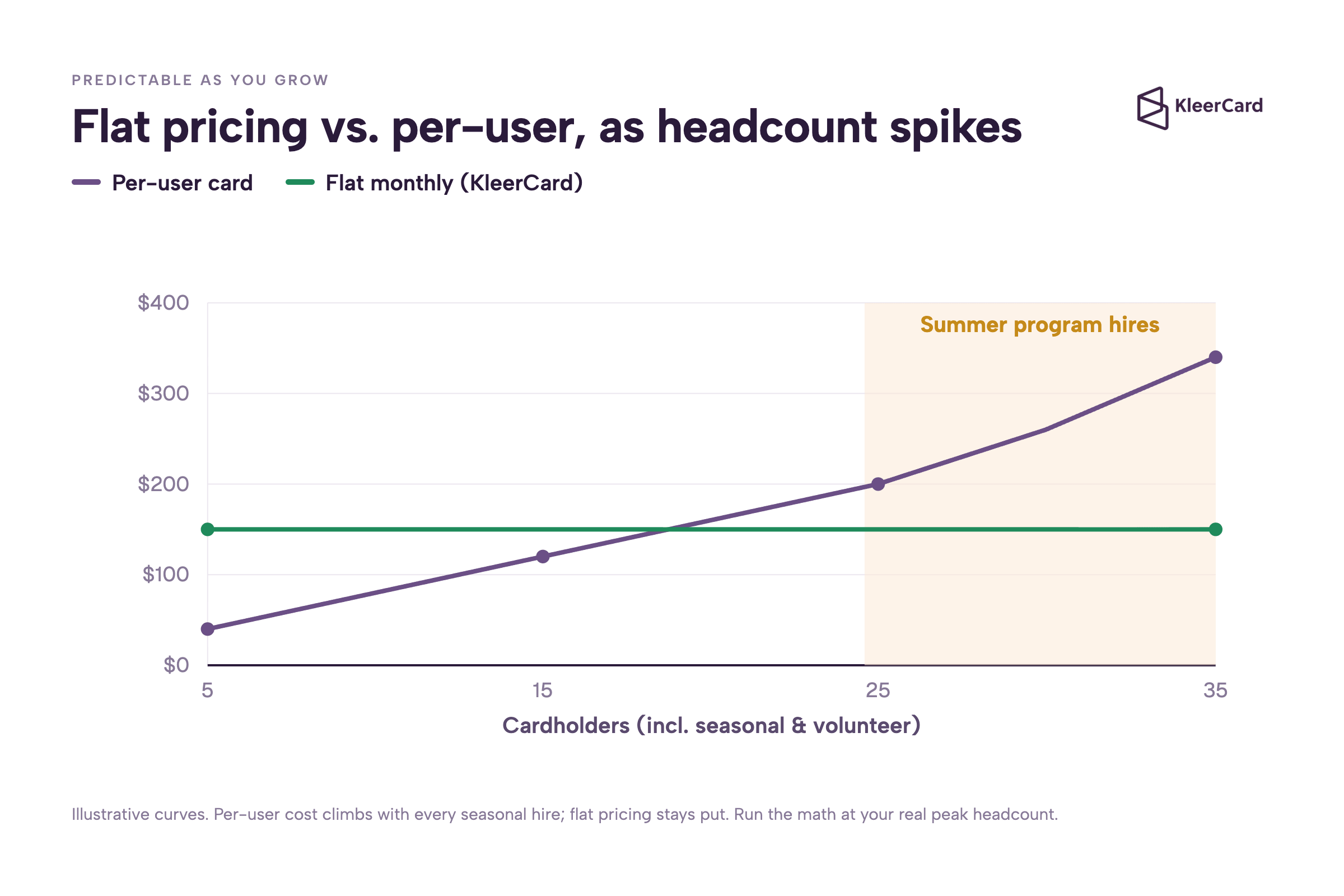

Pricing that stays predictable as you grow

Pricing models create different risks depending on how your headcount and spending actually behave.

The Seasonal User Problem

Some programs charge per user or per card. Others add platform fees that appear or increase at renewal. A few keep a flat monthly rate regardless of how many people hold cards or how spending fluctuates month to month.

The per-user model creates a specific problem for organizations with seasonal or volunteer-heavy patterns. A church or school may need cards for summer interns, VBS coordinators, missions trip leaders, or part-time teachers who only work a few weeks or months. Under a per-user structure those temporary users drive incremental cost exactly when the organization is already managing extra activity.

Flat pricing removes that variable. Platform fees that surface at renewal create a different budgeting risk. Some providers have added significant fees for smaller accounts at renewal time as they move upmarket. Nonprofits with fixed budgets cannot easily absorb a several-thousand-dollar surprise in the middle of a fiscal year.

KleerCard prices on a flat monthly basis rather than per user. Current plan details and any volume-based options live on our pricing page. For a large organization with steady year-round headcount and high spend in bonus categories, a per-user platform with strong rewards can still pencil out.

For most churches, schools, and smaller to mid-size nonprofits, the predictability of flat pricing matters more than chasing marginal rewards.

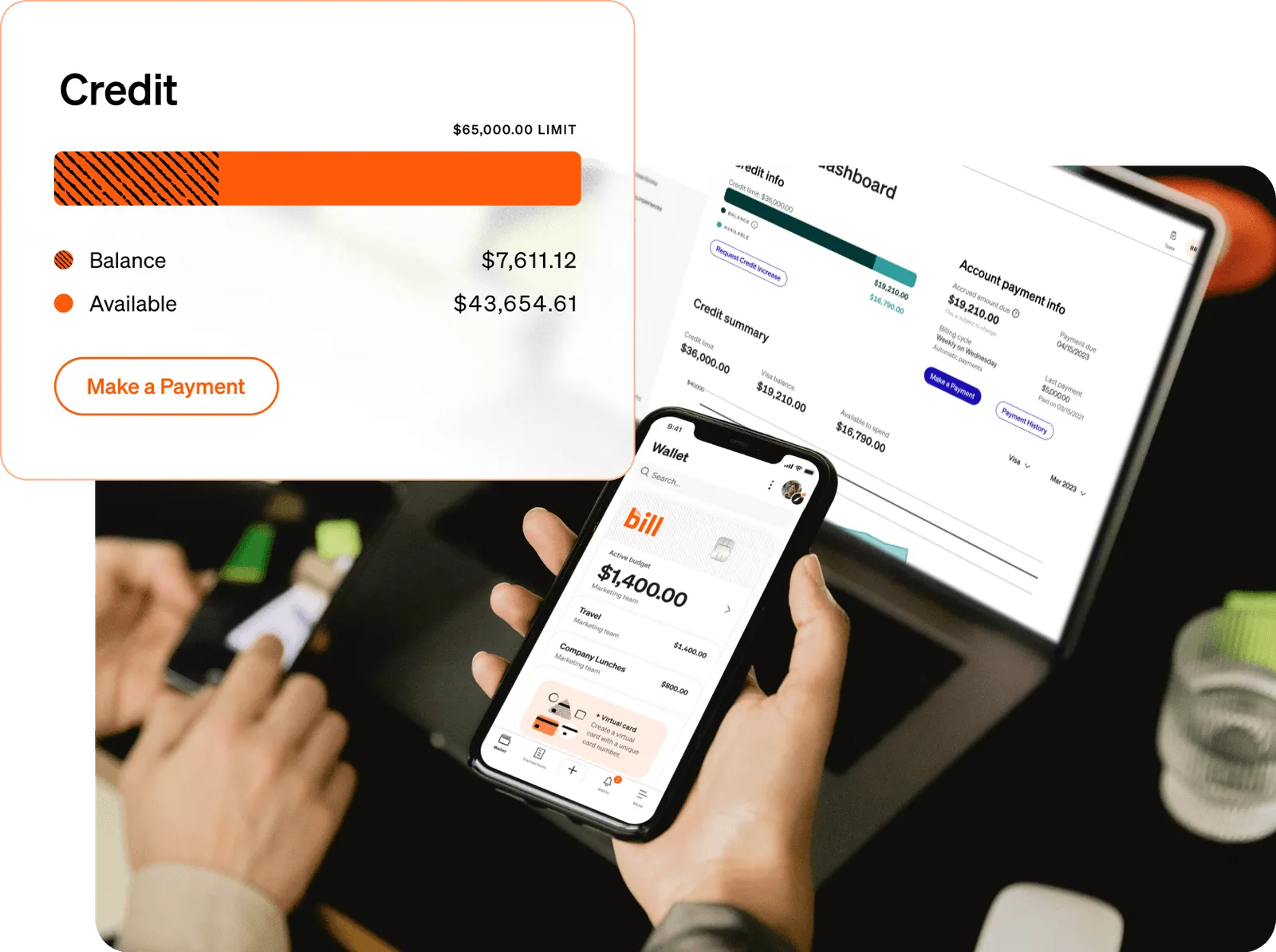

Spending controls that match how your team spends

The most useful controls prevent problems before they happen rather than surfacing them in a report thirty days later.

Volunteer and Event-Based Spending

Look for per-card spending limits that actually block transactions once the cap is reached. Category and merchant restrictions that keep a card from working at the wrong places. Single-use virtual cards that expire after one transaction or after a set date. Time or day windows that limit when a card can be used. Automatic locking when receipts are missing after a defined period.

The volunteer and event use case is where many programs reveal their limits. A fall-festival coordinator or a field-trip teacher needs a card with a tight, event-specific budget, the ability to upload a receipt from a phone, and no requirement for a permanent organizational email address.

The card should simply stop working once the event ends or the budget is exhausted. I have seen school districts run their entire operation on two shared cards. Teachers check one out, sign forms accepting personal liability, and sometimes end up fronting purchases anyway when the card is already checked out to someone else.

The reimbursement cycle can stretch to eight weeks even after the purchase is approved. At one district, maintenance staff had to locate whoever was currently holding the only available card before they could buy basic supplies like toilet parts. The constraint was never trust or available budget. It was physical access to a working card at the moment of need.

Programs that issue the right-sized budget authority to the person who actually spends remove that bottleneck. The control becomes whether the person has permission and budget, not whether they can locate a plastic card in someone else's desk.

KleerCard was built with these granular controls as a core priority because the organizations we serve consistently trade rewards for tighter day-to-day management.

For more on how single-use and event-specific virtual cards work in practice, see what is a virtual card.

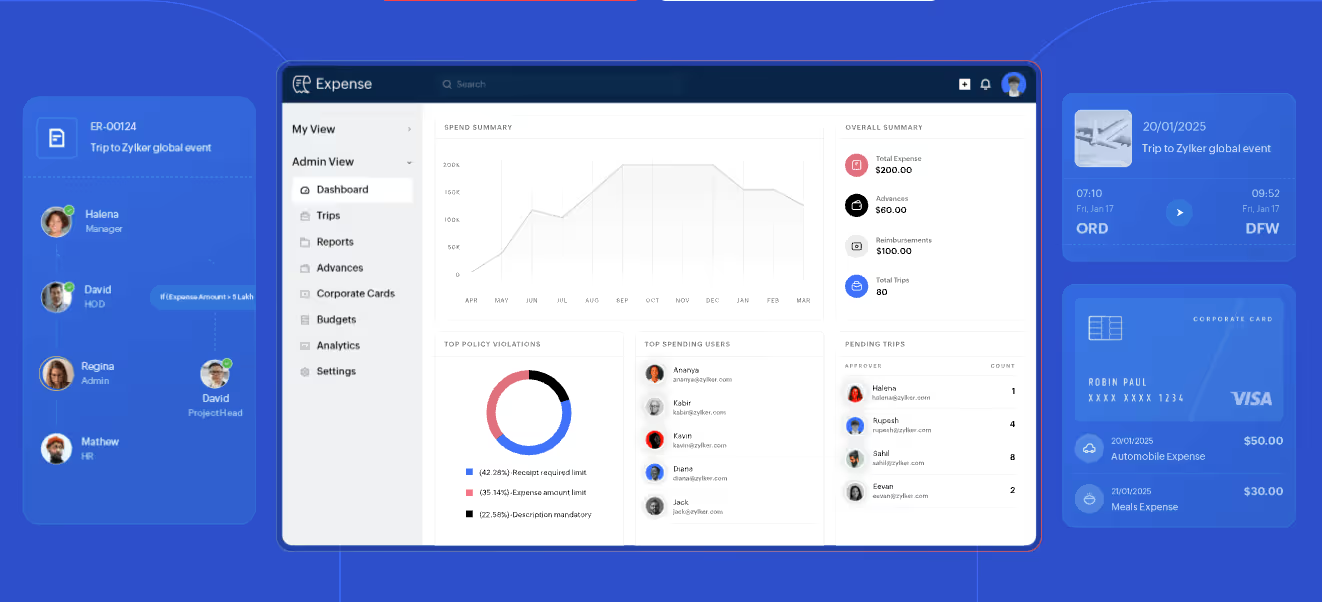

Accounting integration and reconciliation

Month-end close is where the real cost of a poor card choice shows up.

Some platforms deliver transactions directly into your accounting software with fund or class tags already applied. Others export a generic CSV that requires manual reformatting, column mapping, and line-by-line coding before import. When your accounting system is a true fund accounting platform rather than QuickBooks or NetSuite, the gap becomes expensive in staff time.

Direct integrations matter here. KleerCard connects natively with the platforms churches and nonprofits actually run: Aplos, ShelbyNext Financials, Realm Accounting, ParishSOFT, ACS Technologies, and Blackbaud Financial Edge NXT, alongside QuickBooks Online and Desktop.

Transactions flow with the coding already aligned to your chart of accounts and fund structure. One executive pastor reported that month-end close dropped from three days of work to roughly seven minutes once the card transactions and receipts were flowing cleanly. A finance director at another organization went from roughly forty hours per month spent collecting receipts and manually coding expenses down to about one hour in the first month after implementation.

If your current process involves downloading statements, hunting for receipts, and rebuilding CSV files every close, the integration question is usually the highest-leverage single change you can make. See accounting sync for details on supported platforms and how the data flows.

Rewards and cashback: an honest look

Rewards are the feature most marketing emphasizes and the one that matters least for most mission-driven buyers once you run the actual numbers.

Cashback or points only deliver value if your team spends in the bonus categories the card rewards. Many church and nonprofit purchases — curriculum, event supplies, mission trip logistics, facility maintenance — do not align neatly with typical bonus categories. The effective rate after fees and after the time spent tracking and allocating the reward often lands well below the headline percentage.

At the nonprofit level there is an additional accounting friction. Cashback cannot simply be treated as personal bonus or general slush. It has to be allocated to the correct fund or program. That allocation work often offsets much of the financial benefit.

KleerCard does not offer cashback or rewards as a standard feature. Custom pricing that includes cashback is available for organizations whose card spend regularly exceeds roughly $30,000 per month. For most churches, schools, and smaller to mid-size nonprofits, the combination of controls, integration, and predictable flat pricing delivers more operational value than chasing 1% back on spend that does not fit bonus categories anyway.

A high-volume organization that does spend heavily in rewarded categories can still come out ahead on cashback. That is a legitimate calculation to run. It simply sits lower in the decision order than eligibility, pricing predictability, controls, and accounting fit.

Support, onboarding, and the people who will use the card

The people who actually use the cards are often not full-time finance staff.

Volunteers, part-time ministry leaders, teachers, and board members rotate in and out. They need to request a card, set a budget, upload a receipt from a phone, and move on without a half-day training course or a thick policy manual. Video-only self-serve onboarding works well for technical users who already live in software.

It breaks down for the exact people who end up holding most of the cards in a church or school setting. Ask any provider three concrete questions:

- How do you handle a volunteer or seasonal staff member who only needs a card for six weeks or two months?

- What happens when the person who originally set up the account and trained everyone rotates off the board or leaves the organization?

- Can I reach a real person who understands how fund accounting and ministry budgeting actually work when something does not line up?

KleerCard runs guided setup calls as the standard path because that is who our customers are. The implementation team walks through card issuance, budget loading, receipt workflows, and accounting sync in short, focused sessions rather than expecting every user to self-teach from videos.

Provider fit and stability

Features are only useful if the provider's overall model fits how your organization actually operates over multiple years.

Unlike many guides written primarily for funded startups that emphasize rewards and rapid scaling, the needs of churches, nonprofits, and schools are different. Some cards were built for venture-backed startups and later opened a nonprofit vertical. They may approve your organization but still treat fund tagging, seasonal ministry cycles, and volunteer cardholders as edge cases.

Others were built for large enterprises and carry approval processes and fee structures that assume dedicated procurement and finance teams. Cash-flow terms matter. Some programs operate on short payment cycles that require the organization to fund the card spend quickly. Others offer longer float that aligns better with grant drawdowns or pledge collection timing.

Pricing stability is a multi-year bet. Providers that subsidized growth with low headline prices and later introduced platform fees at renewal create exactly the budgeting uncertainty a mission-driven organization cannot easily absorb.

KleerCard is built specifically for nonprofits, churches, and schools. For most for-profit small businesses or organizations that need long receivable cycles and complex enterprise approval chains, other options fit better. I will say that directly when it is true.

How to run the comparison

Once you have worked through the seven questions, run a short, structured comparison.

Read the cardholder agreement for the specific language on personal guarantees, fee triggers at renewal or termination, and what happens to virtual cards and budgets when a user is removed.

Talk to two or three peer organizations that use the card in a setting similar to yours. Ask about the real month-end close process and what surprised them after go-live.

Check independent reviews and comparison data on sites like NerdWallet, Nav, and Bankrate for the eligibility and fee details that marketing pages sometimes bury.

Run the pricing math at your actual user count and your actual monthly spend, including seasonal peaks. Do not use optimistic averages.

Confirm that the integration works with your exact accounting platform by name. "Supports fund accounting" is not the same as a native sync that preserves your fund and class structure without manual rework.

Frequently asked questions

Do corporate cards require a personal guarantee?

Many corporate cards do not require a personal guarantee when the card is issued to the organization and underwritten on its financials and history. KleerCard approves based on the organization's information without asking any individual to pledge personal credit. This removes the reassignment problem that appears when a treasurer, pastor, or finance lead rotates out.

Can I get a corporate card with an EIN only?

Most corporate card programs require an EIN, a business bank account, and some operating history for the entity. Brand-new organizations with no track record may need to establish basic banking history or start with a secured card before qualifying for an unsecured corporate line.

What is the difference between a corporate card and a business credit card?

A corporate card is issued to the legal entity. Approval and liability rest on the organization's financials. A business credit card is tied to an individual whose personal credit is checked and who typically provides a personal guarantee. The card lives on that person's credit report and creates friction when they leave the organization.

How do corporate cards work?

The organization applies and receives a credit line based on its own information. Cards, physical or virtual, are issued to specific people or for specific events with per-card budgets and controls. Transactions post in real time to a dashboard where users upload receipts from a phone. The platform applies coding and syncs cleanly into the organization's accounting software.

Controls such as limits, merchant restrictions, and auto-lock for missing receipts operate at the individual card level.

Can a nonprofit or church get a corporate card?

Yes. Nonprofits and churches with an EIN and established banking history routinely qualify for corporate cards. The key variables are whether the program requires a personal guarantee, whether it integrates with fund accounting platforms, and whether pricing remains predictable when volunteer and seasonal users are added.

What credit score do you need for a corporate card?

Corporate cards are underwritten on the organization's financials and history rather than any individual's personal credit score. Some programs still request personal credit information or a guarantee from a signer, but others, including KleerCard, do not. The organization's operating history and banking relationship carry the weight.

Conclusion

Eligibility without personal risk, pricing that does not surprise you at renewal or when you add seasonal help, controls that prevent problems at the point of spend, and accounting integration that actually closes the month — those four criteria cut through most of the noise in the corporate card market.

If you run a nonprofit, church, or school and fund accounting fit, volunteer card access, or flat predictable pricing are priorities, KleerCard is built for exactly that setting. If another provider aligns better with your specific constraints, the best credit cards for nonprofits comparison can help narrow the field further.

Start with the questions that matter most for your team. The right card becomes obvious quickly once you stop leading with rewards.

Ready to evaluate options against your actual workflow? You can sign up and begin testing in minutes, or schedule time with our team to walk through your specific setup. For churches and nonprofits exploring spend management more broadly, see our solutions for churches and solutions for non-profits.

.png)

.avif)

.svg)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)