%202.svg)

A free nonprofit budget template plus a CFO's step-by-step guide to filling it with defensible numbers, splitting functional expenses, and tracking spend all year.

A nonprofit budget is a financial plan that projects your revenue and expenses for one fiscal year. A good one separates restricted money from unrestricted and sets spending limits by program. It also gives your board a benchmark to measure results against as the year goes on.

A template gives you the categories and a place to put numbers. The harder work starts after the board approves it, when you spend against those numbers month after month.

I ran the budget at Compassion International before starting a fractional CFO practice for nonprofits, and I serve as treasurer at my church. The template below is the one I use with the organizations I advise. The steps after it show how to fill it with numbers you can defend.

Click here to download a free budget template.

An operating budget answers two questions: where the money comes from, and where it goes.

Your revenue side reflects how nonprofits raise money, which looks nothing like a company's sales line. You pull from individual gifts, grants, program fees, events, and sometimes investment income. Each source behaves differently, so you budget each one on its own row.

The expense side carries a wrinkle that for-profit budgets skip. You classify each cost two ways at once.

Natural classification answers what you spent money on, like salaries and rent. Functional classification answers why you spent it. The IRS sorts each dollar of expense into three functions on Form 990, Part IX: program services, management and general, and fundraising.

Build both views into your budget from the start. You save yourself a reclassification project at tax time. Your template should carry the functional split as columns next to each expense line.

Here is the structure I use with the organizations I advise. Copy it into a spreadsheet (or download this one) and adjust the line items to match your programs.

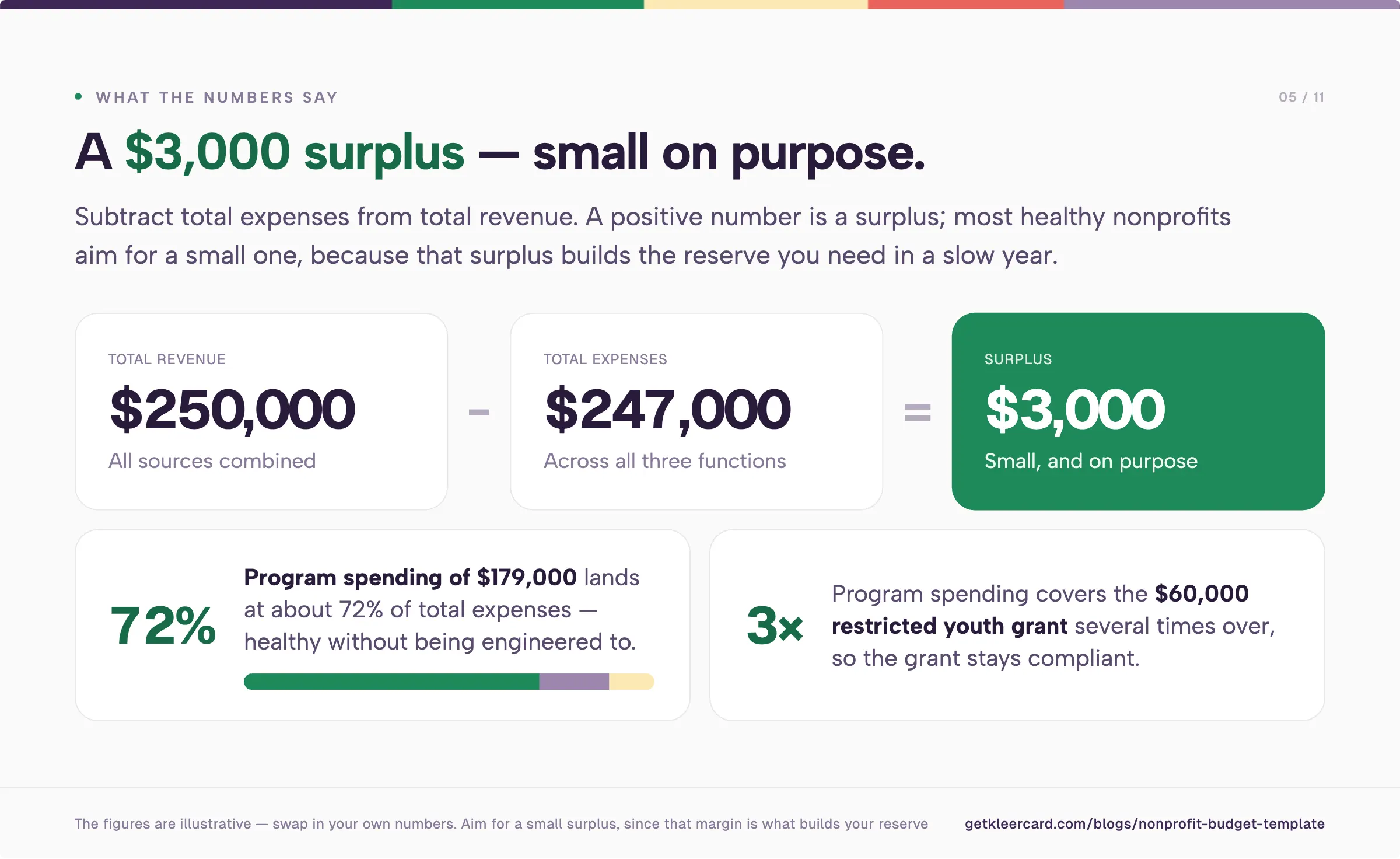

Subtract total expenses from total revenue. A positive number is a surplus, a negative one is a deficit. Most healthy nonprofits aim for a small surplus, because that surplus builds the reserve you need in a slow year.

Add one more tab to track the budget against reality. Use the same line items, twelve monthly columns, and a variance column that shows budget minus actual. That tab is where you put the budget to work all year.

The figures below are illustrative, not real. They show a small youth-services nonprofit with a $60,000 grant restricted to its youth program. Swap in your own numbers.

Revenue minus expenses leaves a $3,000 surplus, small on purpose. Program spending of $179,000 covers the $60,000 restricted grant several times over, so the grant stays compliant. Program costs land at about 72 percent of total expenses, which reads as heal›thy without being engineered to.

The template hands you a container. These steps fill it with numbers you can stand behind.

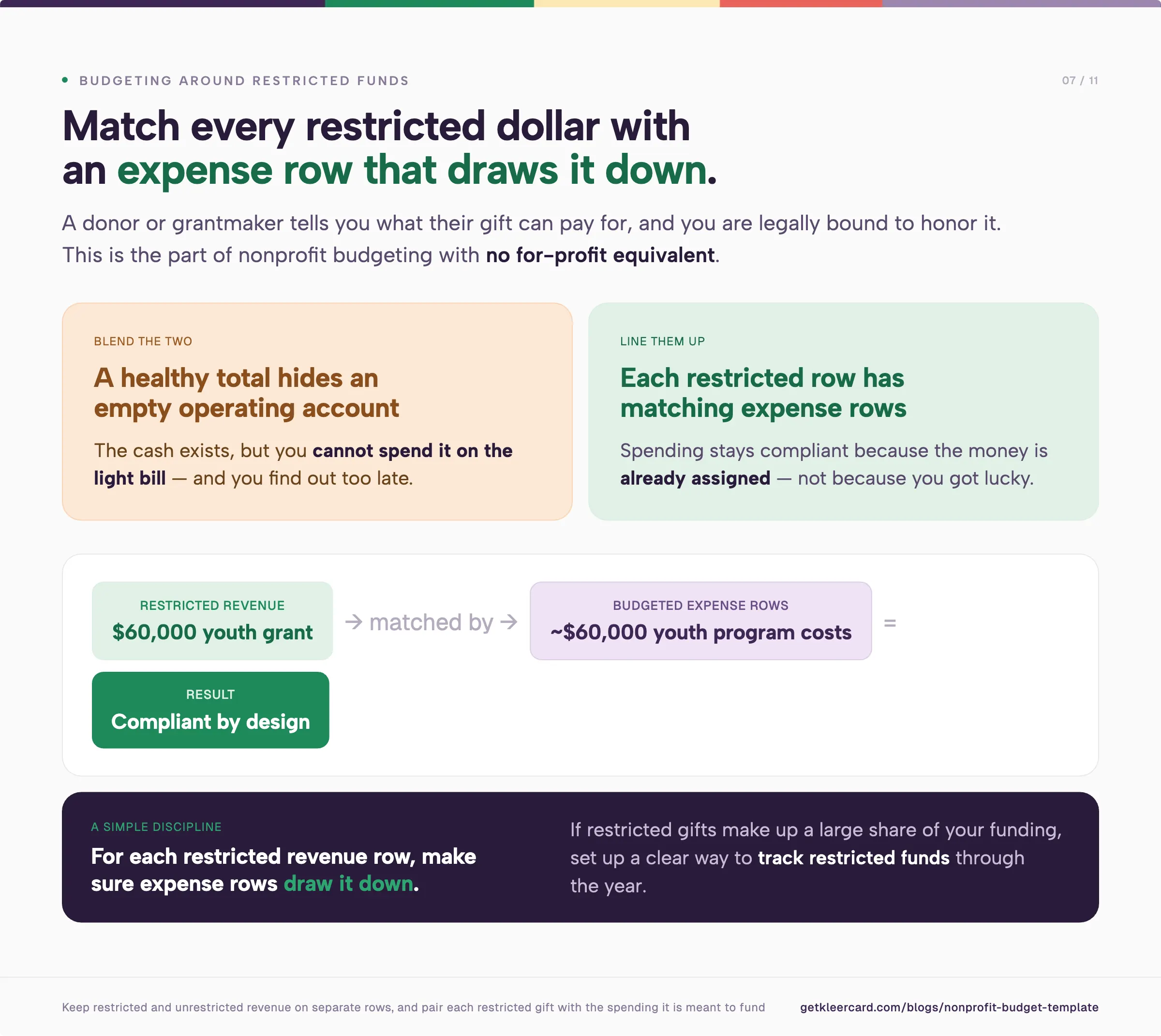

Restricted money is the part of nonprofit budgeting with no for-profit equivalent. A donor or grantmaker tells you what their gift can pay for, and you are legally bound to honor that.

Keep restricted and unrestricted revenue on separate rows. Blend them, and you can show a healthy total while your unrestricted operating funds run dry. The cash exists, but you cannot spend it on the light bill.

A simple discipline helps. For each restricted revenue row, make sure a matching set of expense rows draws it down. A $40,000 youth program grant should be matched by roughly $40,000 of budgeted youth program costs. With the two sides lined up, your spending stays compliant because the money is already assigned, not because you got lucky.

If restricted gifts make up a large share of your funding, set up a clear way to track restricted funds through the year.

The three functional categories are not optional bookkeeping. Section 501(c)(3) and 501(c)(4) organizations report expenses across all three columns on the IRS Statement of Functional Expenses. A budget that already splits costs this way makes year-end filing easier, and it lines up with how your nonprofit accounting should be structured from the start.

Program services covers the direct cost of delivering your mission. Management and general covers running the organization, including board meetings and accounting. Fundraising covers the cost of asking for money, from event expenses to donor database fees.

The split also tells your story to funders. Grantmakers read these ratios before they write a check, and your board uses them to confirm that most of your money reaches the work. Strong expense reporting habits make those ratios easy to produce on demand.

No IRS rule caps what a nonprofit spends on salaries or overhead, and the right ratio depends on what you do. A direct-service charity with caseworkers runs high on personnel, because the people are the program. A grantmaking foundation looks different.

Your real test is whether the ratio fits your mission and your funders' expectations. Many charity evaluators look for a healthy majority of total expenses landing in program services. Use that as a gut check, not a target to game. Starving your own operations to post a flattering program ratio tends to backfire within a year or two.

A reserve is unrestricted cash you set aside ahead of time, so a late grant or a slow quarter does not turn into a crisis. A common goal is three to six months of operating expenses, built up over time. The National Council of Nonprofits notes there is no single standard that fits every organization, so your board sets the target that suits your funding and your risks.

You fund a reserve by budgeting a modest surplus and protecting it. That is why healthy nonprofits keep a margin instead of spending all they raise. The surplus is what lets you keep serving people when revenue stumbles.

A budget protects you only if you can see spending against it while there is still time to react.

Most small nonprofits cannot. I watch the same pattern in organization after organization. One person enters credit card statements by hand at month's end, and the team cannot see where a department stands until that work is done. Staff buy on personal cards or a shared card, receipts arrive late, and the budget figure you check is weeks out of date.

Cindy S., a finance manager at a multi-ministry church, spent two and a half hours a month entering credit card statements into her accounting software by hand. Her staff could not see budget status in real time. They knew where they stood only after she processed each month's statement. By the time she saw a program was over budget, the money was already spent.

You can line up who can spend with what they are allowed to spend before the swipe, instead of after. Give each program or staff member a card loaded with their own budget. Set a hospitality lead up with $300 a month. Load a fall festival card with its $1,000 budget. Hand a teacher a card with their classroom allowance instead of asking them to front the cost and wait for reimbursement.

Once the budget sits on the card, staff cannot spend past it, and each charge already carries the program it belongs to. A high-limit card kept in a drawer feels safe, yet whoever holds it can spend far past what you intended. Loading each card with a right-sized budget removes that risk.

We built KleerCard for this, for nonprofits, churches, and schools that need budget-capped cards and real-time visibility without a personal guarantee. Your accounting software stays your system of record. The cards give you a live view of spending against the budget you set.

Jared, an executive pastor, watched his month-end close drop from three days to about seven minutes after the switch. If your organization spends on shared cards and reconciles after the fact, that delay is worth removing.

A few patterns cause most of the trouble I see.

None of these are hard to avoid once you know to look for them.

No fixed percentage applies, and there is no IRS limit. Personnel is usually the largest line in a nonprofit budget. For direct-service organizations it often makes up the majority of spending, because staff deliver the mission. Judge your ratio by whether it fits your work and satisfies your funders.

A nonprofit budget has two sides: revenue and expenses. Revenue categories include donations, grants, program fees, and events. Expenses are classified both by natural type, like salaries and rent, and by function: program services, management and general, and fundraising.

Restricted funds carry a donor or grantmaker condition that limits what they can pay for. Unrestricted funds can go toward any legitimate cost, including rent and salaries. Keep the two on separate budget rows, because a healthy total can hide an unrestricted shortfall if you blend them.

Start with your program plan and the cost to deliver it, since a new nonprofit has no historical actuals. Estimate startup and recurring expenses first. Then build revenue targets from named sources you can expect. Keep your first budget conservative and revisit it each quarter.

An operating budget covers your whole organization for a fiscal year. A program budget covers the revenue and costs of a single program. Program budgets roll up into the operating budget, and grantmakers often ask to see one when funding a specific initiative.

A frequent target is three to six months of operating expenses, though the National Council of Nonprofits points out that no single figure fits every organization. Your board should set a reserve policy based on how steady your funding is and what surprises you need to weather.

Review your budget against actual results at least once a month. A budget is a living document, so amend it during the year when conditions change. Boards usually receive a budget-to-actual report at each meeting.

In most nonprofits, staff prepare the annual budget and the full board adopts it at a board meeting. The National Council of Nonprofits describes this as standard practice, since the board holds fiduciary responsibility for the organization's finances.

A template gets you a clean structure in an afternoon. The numbers come from your real history and your real plan. The value comes from checking them against actual spending all year.

Copy the template above, fill it with conservative numbers, and split your expenses by function from the start. Then give yourself a way to watch the money move while you can still steer.

If real-time visibility and budget-capped cards would help, you can open a KleerCard account or see our pricing. If a spreadsheet and a disciplined monthly review are all you need right now, that works too. The budget is yours either way.

Speak to a member of our team and we can have you up and running in minutes, not weeks.